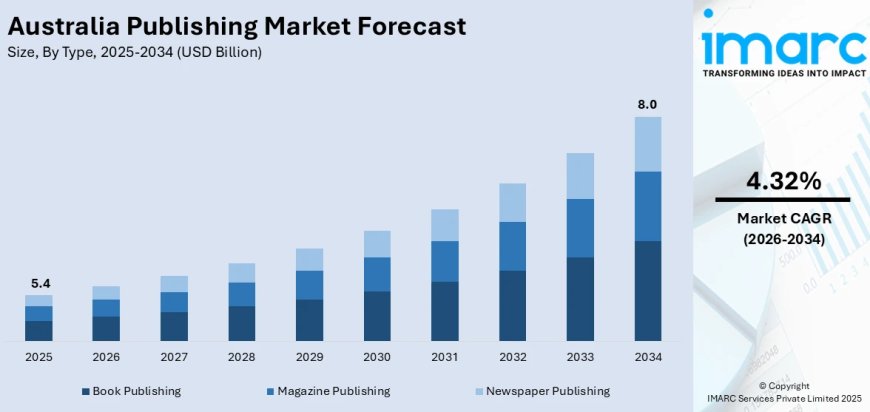

Australia Publishing Market 2026 | Worth USD 8.0 Billion by 2034

Australia publishing market size reached USD 5.4 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 8.0 Billion by 2034, exhibiting a growth rate (CAGR) of 4.32% during 2026-2034.

Australia Publishing Market Overview

The Australia publishing market size reached USD 5.4 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 8.0 Billion by 2034, exhibiting a growth rate (CAGR) of 4.32% during 2026-2034. Australia's publishing sector is experiencing a dynamic transformation driven by the rapid expansion of digital content platforms, the explosive growth of audiobooks, increasing government investment in literary programs, and the rising prominence of self-publishing models that are democratizing content creation. The Australian Government, through Writing Australia (launched July 2025), is investing more than AUD 26 million over three years to support the nation's literature sector, including the Australian Publishing and Promotion Fund offering AUD 2 million for independent publishers.

The market is being further propelled by the audiobook segment, which is projected to grow at 26.4% annually and is generating significant revenue through AI-powered narration technologies that are making production more accessible and affordable for independent authors. Educational publishing is undergoing a parallel transformation as schools and universities increasingly adopt interactive digital textbooks for hybrid learning models, while subscription-based reading platforms are introducing AI-driven personalized recommendation features that are reshaping consumer engagement and content discovery across the publishing ecosystem.

Request a Business Sample Report for Procurement & Investment Evaluation:

https://www.imarcgroup.com/australia-publishing-market/requestsample

Porter's Five Forces Analysis – Australia Publishing Market

Bargaining Power of Suppliers – Moderate

• Authors and content creators represent the primary suppliers, with established bestselling authors commanding significant negotiating power over royalty terms and publishing contracts, while emerging writers face more limited leverage in traditional publishing arrangements.

• The rise of self-publishing platforms is positively rebalancing supplier dynamics, empowering independent authors to bypass traditional gatekeepers and reach audiences directly, with the self-publishing segment valued at approximately USD 1.25 billion annually and growing steadily.

Bargaining Power of Buyers – Moderate to High

• Digital platforms including Amazon Kindle, Audible, and subscription-based reading services provide consumers with extensive choice and price comparison capabilities, increasing buyer influence over content pricing and distribution models.

• Educational institutions represent significant bulk buyers with strong procurement leverage, particularly as schools and universities increasingly adopt interactive digital textbooks for hybrid learning models, driving competitive pricing among educational publishers.

Threat of New Entrants – Moderate to High

• Digital publishing and self-publishing platforms have significantly lowered barriers to entry, enabling independent authors and small publishers to access global distribution channels with minimal capital investment, fostering a vibrant ecosystem of new content creators.

• Established publishers such as Penguin Random House, HarperCollins Australia, and Hachette Australia maintain competitive advantages through extensive distribution networks, strong brand recognition, and backlist catalogues, while Writing Australia's AUD 2 million Publishing and Promotion Fund is actively supporting independent publishers to compete and innovate.

Threat of Substitutes – Moderate

• Streaming video platforms, podcasts, social media content, and interactive gaming represent alternative entertainment options, but published content—particularly books, audiobooks, and educational materials—retains a distinct value proposition rooted in depth, expertise, and long-form engagement.

• The publishing industry is positively integrating substitute formats rather than being displaced, with audiobooks projected to grow at 26.4% annually and AI-powered narration technologies expanding the market by making audio content production more accessible and cost-effective for publishers of all sizes.

Competitive Rivalry – Moderate to High (Healthy)

• The market features healthy competition among global publishers (Penguin Random House, HarperCollins, Hachette), independent Australian publishers (Allen & Unwin, Scribe Publications, Text Publishing), self-publishing platforms, and digital content distributors—driving innovation in content delivery and reader engagement.

• Competition is increasingly centered on digital capabilities, with publishers investing in audiobook production, AI-driven content recommendations, and subscription models, creating a dynamic competitive landscape that is expanding market reach and improving content accessibility across diverse demographics and geographies.

Australia Publishing Market Trends

Digital Content Expansion and Audiobook Revolution

The most transformative trend in Australia's publishing market is the rapid expansion of digital content formats, particularly audiobooks and e-books. The Australian audiobook market is projected to reach USD 316.6 million in 2025, with revenue expected to grow at a CAGR of 6.12% through 2030, reaching USD 426.1 million. The non-fiction audiobook segment is leading growth with an annual rate exceeding 27%, driven by increasing demand for educational and self-improvement content. AI-powered narration technologies are making audiobook production more accessible and affordable, enabling independent authors and smaller publishers to enter the market. This digital transformation is complemented by the growing adoption of subscription-based reading platforms that use AI-driven personalized recommendations to enhance reader engagement, reshape content discovery patterns, and create recurring revenue streams for publishers across all market tiers.

Self-Publishing Growth and Independent Author Empowerment

Australia's publishing landscape is being reshaped by the democratization of content creation through self-publishing platforms. The self-publishing segment, valued at approximately USD 1.25 billion annually, is enabling independent authors to bypass traditional publishing barriers and reach global audiences directly. Digital platforms are providing new tools including AI-assisted editing, automated formatting, and global distribution features that significantly reduce the time and cost of bringing works to market. Social media platforms, particularly BookTok and Bookstagram, are playing an increasingly significant role in book discovery and promotion, with influencers and online communities shaping reading trends and consumer preferences, creating new pathways for independent authors to build audiences and achieve commercial success outside traditional publishing channels.

Australia Publishing Market Summary

The Australia publishing market is defined by digital transformation, government investment, and evolving content delivery models:

• The market was valued at USD 5.4 Billion in 2025 and is projected to reach USD 8.0 Billion by 2034, growing at a CAGR of 4.32% during 2026-2034.

• The audiobook segment is projected to reach USD 316.6 million in 2025 and grow at 6.12% CAGR through 2030, with AI-powered narration technologies expanding production accessibility for independent publishers and authors.

• Writing Australia, launched in July 2025, is investing more than AUD 26 million over three years to support the literature sector, including the AUD 2 million Australian Publishing and Promotion Fund for independent publishers.

• Self-publishing platforms are democratizing content creation, with the segment valued at approximately USD 1.25 billion annually and digital tools including AI-assisted editing enabling independent authors to reach global audiences directly.

• Educational publishing is transforming as institutions adopt interactive digital textbooks for hybrid learning, while subscription-based reading platforms leverage AI-driven recommendations to reshape consumer engagement and content discovery.

Australia Publishing Market Growth Drivers

Digital Transformation and Multi-Format Content Delivery

The accelerating shift toward digital content consumption is a primary structural driver of Australia's publishing market growth. Consumers are increasingly adopting e-books, audiobooks, and digital subscription platforms, with the audiobook market alone projected to grow at 26.4% annually over the next seven years. The integration of AI technologies into content production—including AI-assisted editing, automated translation, and AI-powered narration—is reducing production costs and enabling publishers to offer content across multiple formats simultaneously. Educational institutions are driving additional demand through the adoption of interactive digital textbooks and online learning resources for hybrid education models, while corporate and professional publishing is expanding as businesses invest in digital knowledge management and training content delivery systems.

Government Investment and Cultural Policy Support

The Australian Government's sustained investment in the literary and publishing sector is providing a structural growth foundation with long-term funding visibility. Writing Australia, established in July 2025 under Creative Australia, is receiving more than AUD 26 million over three years for new investment, in addition to the AUD 7.8 million that Creative Australia invests annually for literature projects. The Australian Publishing and Promotion Fund is offering AUD 2 million in grants ranging from AUD 50,000 to AUD 200,000 to support independent publishers in becoming more competitive and innovative. Additional programs including the Literary Journals Capacity Building Fund, the Writers' Festival Author Travel Fund, and the inaugural National Poet Laureate appointment are strengthening the broader publishing ecosystem, while the Copyright Agency distributed AUD 650,000 in grants supporting writers, artists, and cultural organizations in 2025.

Australia Publishing Market Segmentation

The Australia publishing market report offers a comprehensive analysis across the following segments, providing detailed insights into market dynamics and growth trajectories:

Breakup by Content Type: Trade Books (Fiction and Non-Fiction), Educational and Academic Publishing, Professional and Business Publishing, Digital Content and E-Books, Audiobooks, Others

Trade books represent the largest content segment, encompassing fiction and non-fiction titles distributed through retail and online channels. Educational and academic publishing is experiencing significant transformation through the adoption of interactive digital textbooks and online learning platforms. Audiobooks constitute the fastest-growing segment, with revenue projected to reach USD 316.6 million in 2025 and non-fiction audiobooks growing at over 27% annually. Digital content and e-books continue to gain market share as consumer preferences shift toward multi-format reading experiences.

Breakup by Distribution Channel: Online Retail, Physical Bookstores, Libraries, Institutional (Schools and Universities), Subscription Platforms, Others

Online retail represents the dominant distribution channel, driven by e-commerce platforms and digital content delivery. Physical bookstores maintain a meaningful market presence through curated experiences, author events, and community engagement. Subscription platforms are emerging as the fastest-growing channel, with AI-driven personalized recommendations reshaping content discovery and consumer engagement patterns. Institutional distribution through schools and universities remains a critical channel for educational publishing.

Breakup by Publishing Model: Traditional Publishing, Self-Publishing, Hybrid Publishing, Others

Traditional publishing remains the largest segment, dominated by multinational publishers with established distribution networks and backlist catalogues. Self-publishing is the fastest-growing model, valued at approximately USD 1.25 billion annually, empowered by digital platforms offering AI-assisted editing, automated formatting, and global distribution capabilities. Hybrid publishing models are gaining traction as authors seek to combine the editorial quality of traditional publishing with the creative control and revenue share of self-publishing.

Breakup by Region: New South Wales, Victoria, Queensland, Western Australia, South Australia, Others (including ACT, Tasmania, Northern Territory)

New South Wales leads the regional market, driven by Sydney's position as Australia's publishing capital with the highest concentration of publishers, literary agencies, and distribution infrastructure. Victoria follows closely, with Melbourne's strong literary culture, independent bookstore network, and the presence of major publishing houses. Queensland represents the third-largest market, with growing demand for digital content and the expansion of regional literary festivals and author programs supported by government funding.

Australia Publishing Market Competitive Landscape

The Australia publishing market features a diverse competitive landscape comprising multinational publishing conglomerates, independent Australian publishers, self-publishing platforms, and digital content distributors. Key players operating in the market include Penguin Random House Australia, HarperCollins Australia, Hachette Australia, Allen & Unwin, Pan Macmillan Australia, Simon & Schuster Australia, Scribe Publications, Text Publishing, Wiley Australia, and Oxford University Press Australia. These organizations compete across trade, educational, and digital publishing segments. The competitive landscape is evolving as independent publishers receive expanded government funding through Writing Australia, self-publishing platforms gain market share through technology-enabled author empowerment, and major publishers invest in audiobook production, AI-driven content solutions, and subscription-based distribution models.

Australia Publishing Market: Latest News and Developments

Recent developments shaping the Australia publishing market include:

• February 2026: Writing Australia opened applications for the Australian Publishing and Promotion Fund 2026–27, offering AUD 2 million in investments ranging from AUD 50,000 to AUD 200,000 to support independent publishers in becoming more competitive, innovative, and sustainable.

• 2026: Writing Australia announced the inaugural National Poet Laureate nominations, establishing a new national role to serve as an ambassador for language, imagination, and poetry in public life, marking a significant milestone in Australia's literary cultural infrastructure.

• 2025: Writing Australia was launched on July 1 under Creative Australia, receiving more than AUD 26 million over three years for new investment in the literature sector, in addition to Creative Australia's existing AUD 7.8 million annual literature investment.

• 2025: The Australian audiobook market reached USD 316.6 million in revenue, with non-fiction audiobooks growing at over 27% annually, as AI-powered narration technologies expanded production capabilities for independent authors and publishers.

• 2025: The Copyright Agency distributed AUD 650,000 in grants supporting Australian writers, artists, and cultural organizations, reinforcing the financial support ecosystem for the publishing industry's creative workforce.

Note: If you require any specific information not currently covered within the scope of the report, IMARC Group will provide it as part of customization.

Speak to an analyst:

What's Your Reaction?