Philippines Active Pharmaceutical Ingredients (APIs) Market | Size, Growth, Trends and Analysis 2026-2034

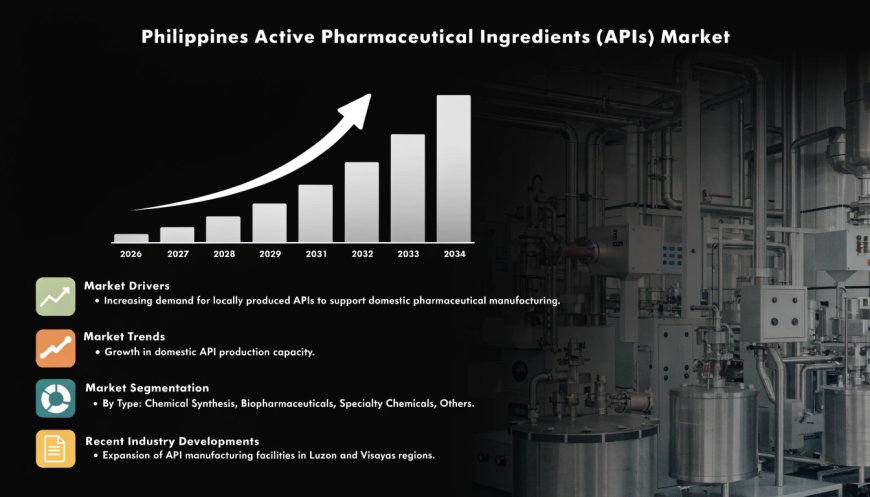

The Philippines active pharmaceutical ingredients (APIs) market size reached USD 5,115.50 Million in 2025. The market is projected to reach USD 7,374.23 Million by 2034, growing at a CAGR of 4.15% during 2026-2034.

Market Overview

The Philippines active pharmaceutical ingredients (APIs) market is advancing at a solid pace, driven by sustained government support for local drug manufacturing, a rising national burden of chronic diseases, and the country's ongoing push to reduce its heavy reliance on imported pharmaceutical inputs. According to IMARC Group, the market size was valued at USD 5,115.50 Million in 2025 and is projected to reach USD 7,374.23 Million by 2034, growing at a compound annual growth rate (CAGR) of 4.15% during 2026‑2034.

The market's momentum reflects a strategic shift toward pharmaceutical self‑sufficiency, reinforced by fiscal policies such as the expanded list of VAT‑exempt medicines, which now covers 2,263 items, directly reducing patient costs and supporting higher demand across pharmacy channels. These affordability measures are particularly impactful for the generics segment, which is expected to command 54 percent of total pharmaceutical sales by 2030, up from 51 percent in 2025. This, combined with a projected 8.8 percent annual growth for generics, is creating consistent and growing demand for domestically produced APIs.

The market is strategically important to the Philippines' economy as it underpins healthcare access, strengthens the country's manufacturing base, and reduces external supply chain vulnerabilities. With the pharmaceutical market expected to reach ₱759 billion ($12.1 billion) by 2030 and the government targeting a 40 percent expansion in local manufacturing capacity under the Philippine Development Plan 2023‑2028, the API sector is emerging as a cornerstone of the nation's industrial and health security strategy.

The Philippines active pharmaceutical ingredients (APIs) market is poised for sustained expansion, driven by a projected CAGR of 4.15% through 2034, expanding pharmaceutical ecozones, and rising generic drug consumption. With VAT exemptions boosting drug affordability and FDI commitments strengthening the value chain, the market offers significant opportunities for local producers and technology partners focused on quality, compliance, and supply chain resilience.

Philippines Active Pharmaceutical Ingredients (APIs) Market Summary

The Philippines active pharmaceutical ingredients (APIs) market encompasses the production and distribution of chemical or biological substances used as the active component in finished pharmaceutical products. APIs are essential for drug efficacy and are categorised by drug type, manufacturer type, synthesis method, and therapeutic application.

The ecosystem includes captive manufacturers producing APIs for their own finished drug products, merchant API manufacturers supplying third‑party pharmaceutical companies, and a growing number of biotech innovators leveraging synthetic and biological synthesis methods.

Segmentation Analysis

-

By Drug Type: Innovative Active Pharmaceutical Ingredients (API), Generic Active Pharmaceutical Ingredients (API)

-

By Type of Manufacturer: Captive Manufacturers, Merchant API Manufacturers

-

By Type of Synthesis: Synthetic Active Pharmaceutical Ingredients (API), Biotech Active Pharmaceutical Ingredients (API)

-

By Therapeutic Application: Oncology, Cardiovascular and Respiratory, Diabetes, Central Nervous System Disorders, Neurological Disorders, Others

-

By Region: Luzon, Visayas, Mindanao

The generic API segment is expected to see strong growth, supported by government policies promoting affordable medicines and the Universal Health Care (UHC) Act. Biotech APIs, including biosimilars, monoclonal antibodies, and vaccines, represent an emerging segment as the country builds capabilities in advanced biological synthesis.

Porter’s Five Forces Analysis – Philippines Active Pharmaceutical Ingredients (APIs) Market

Bargaining Power of Suppliers – Moderate

The Philippines relies heavily on imported APIs, particularly from China and India, which gives international suppliers significant influence over pricing and availability. However, government initiatives to attract foreign direct investment and develop local manufacturing capabilities are gradually reducing this dependency. The establishment of pharmaceutical economic zones (pharmazones) offering tax incentives and streamlined regulatory processes is encouraging both domestic and international players to set up local production, helping to balance supplier power over the medium term.

Bargaining Power of Buyers – High

Buyers include pharmaceutical manufacturers, government procurement agencies, and healthcare providers. The government's commitment to lowering medicine costs through policies such as the Drug Price Reference Index (DPRI) and expanded VAT exemptions gives institutional buyers significant negotiating leverage. The generics market, where cost‑effectiveness is paramount, further amplifies buyer power as pharmaceutical companies seek competitive pricing from API suppliers. However, the specialised nature of innovative APIs and biologics can reduce buyer influence in those segments.

Threat of New Entrants – Moderate

The threat of new entrants is moderate. Capital requirements for API manufacturing are substantial, and navigating regulatory approval processes can be complex. However, government support through pharmazones, which provide tax incentives and streamlined registration, is lowering barriers. The growing demand for generic APIs and the push for local production are attracting new players, particularly in the generic API segment. Established international manufacturers with existing technology and supply chains have an advantage, but local startups focusing on niche biotech APIs or cost‑effective synthetic processes are emerging.

Threat of Substitutes – Low

There is a low threat of substitutes. APIs are essential components of pharmaceutical products, and alternative treatment modalities (e.g., biologics, gene therapy) still require their own specific active ingredients. While some plant‑based or synthetic alternatives exist for certain molecules, they are not direct substitutes for the vast majority of APIs. The increasing complexity of modern drugs, particularly in oncology and biologics, reinforces the need for specialised APIs, limiting substitution risk.

Competitive Rivalry – Moderate

The market is moderately competitive. International API manufacturers, particularly from India and China, dominate imports, while a growing number of local producers are establishing themselves, supported by government incentives. Competition is intensifying in the generic API segment, where cost leadership and quality certification are key differentiators. In the innovative and biotech API segments, competition is based on technological capability, regulatory compliance, and R&D intensity. The push for local production and import substitution is driving both price competition and innovation among local players.

Request for Sample Report: https://www.imarcgroup.com/philippines-active-pharmaceutical-ingredients-market/requestsample

Market Growth Drivers

Establishment of Pharmaceutical Ecozones and Investment Incentives

A primary factor driving the Philippines active pharmaceutical ingredients (APIs) market is the government's aggressive push to establish dedicated pharmaceutical economic zones (pharmazones) under the Philippine Economic Zone Authority. These zones provide tax incentives, simplified regulatory processes, and improved infrastructure, attracting both domestic and international API manufacturers. In January 2026, Filipino-owned Zen LifeSciences Inc. announced a ₱1.2 billion investment to build an export-oriented pharmaceutical manufacturing facility in the Luisita Industrial Park Special Economic Zone in Tarlac, creating nearly 100 jobs and supporting both local and export markets.

The PEZA guidelines for pharmazones, approved in March 2025, outline incentives for developers, operators, and registered business enterprises, aiming to attract substantial pharma investments, advance technology, and increase local production. These zones are expected to position the Philippines as a competitive player in the global pharmaceutical market. Additionally, the Aurora Pacific Economic Zone and Freeport Authority is exploring the establishment of a pharmaceutical investment hub in Casiguran town, with potential activities including R&D, clinical trials, cold chain logistics, and warehousing. These ecozones foster research collaborations and technology transfer, improving production efficiency and product quality, while the government's industrial policies promote innovations in life sciences and support startups focusing on biopharmaceuticals and synthetic chemistry.

Rising Prevalence of Chronic Diseases and Healthcare Access Expansion

The rising prevalence of chronic diseases, including cardiovascular disorders, diabetes, and cancer, is significantly fuelling the demand for APIs in the Philippines. These conditions require long‑term medication, creating sustained and growing demand for both innovative and generic APIs. According to BMI, essential medicines for cancer and diabetes are among the most financially burdensome for patients, and expanded VAT exemptions for these drugs are expected to boost consumption.

The government's Universal Health Care (UHC) Act has increased the accessibility of medicines, particularly generics, reducing healthcare costs for patients and expanding the addressable market for API manufacturers. The Philippine pharmaceutical market is expected to grow to ₱759 billion ($12.1 billion) by 2030, with generic medicines forecast to account for 54 percent of total pharmaceutical sales by 2030, up from 51 percent in 2025. This shift is driving API demand across therapeutic areas such as oncology, cardiovascular, respiratory, and diabetes.

Market Growth Drivers

Reduction of Import Dependency and Pharmaceutical Trade Deficit

The Philippines remains heavily dependent on imported medicine and pharmaceutical ingredients, with a pharmaceutical trade deficit of $2.3 billion in 2025. Over 90 percent of pharmaceuticals in the country are imported, exposing the sector to external supply disruptions and cost fluctuations. The government is actively working to reduce this import dependency through policies that promote local manufacturing.

The government's target of a 40 percent expansion in local pharmaceutical manufacturing capacity under the Philippine Development Plan 2023‑2028 is creating a favourable environment for API investment. The Integrated Roadmap for the Philippine Pharmaceutical Industry (IRPPI), which began in 2023, envisions a local pharmaceutical sector "with a value chain capable of supporting pharmaceutical security and improving health outcomes for Filipinos." Efforts to strengthen national medicine reserves are also expected to provide steadier procurement flows, helping API manufacturers plan production and investment more effectively.

Technological Advancements and AI Integration in API Manufacturing

Artificial intelligence is progressively transforming the API manufacturing landscape in the Philippines by enabling predictive maintenance systems that reduce unplanned downtime, implementing computer vision‑driven quality inspection processes that enhance product consistency, and deploying machine learning algorithms for production optimization and process control. As pharmaceutical manufacturers are adopting Industry 4.0 technologies and digital factory platforms, AI‑powered solutions are improving operational efficiency, reducing manufacturing costs, and ensuring regulatory compliance. These technological advancements are making local API production more competitive and efficient, supporting the government's push for import substitution.

Philippines Active Pharmaceutical Ingredients (APIs) Market Segmentation

Segmentation analysis provides a detailed view of the Philippines active pharmaceutical ingredients (APIs) market by category:

-

Drug Type Insights: Innovative Active Pharmaceutical Ingredients (API), Generic Active Pharmaceutical Ingredients (API)

-

Type of Manufacturer Insights: Captive Manufacturers, Merchant API Manufacturers

-

Type of Synthesis Insights: Synthetic Active Pharmaceutical Ingredients (API), Biotech Active Pharmaceutical Ingredients (API)

-

Therapeutic Application Insights: Oncology, Cardiovascular and Respiratory, Diabetes, Central Nervous System Disorders, Neurological Disorders, Others

-

Regional Insights: Luzon, Visayas, Mindanao

Competitive Landscape

The competitive landscape of the Philippines active pharmaceutical ingredients (APIs) market is characterised by a mix of international suppliers, particularly from India and China, which dominate imports, and a growing number of local manufacturers supported by government incentives. International API suppliers leverage established supply chains and cost advantages, while local producers are focusing on generic APIs and, increasingly, biotech APIs with government support.

Key Manufacturers and Recent Developments:

-

Zen LifeSciences Inc. – Investing ₱1.2 billion to build an export‑oriented pharmaceutical manufacturing facility at the Luisita Industrial Park Special Economic Zone in Tarlac, with commercial operations expected to start in January 2027.

-

Aurora Pacific Economic Zone and Freeport Authority (APECO) – Exploring the establishment of a pharmaceutical investment hub in Casiguran town, with potential activities including R&D, clinical trials, cold chain logistics, and warehousing.

-

Philippine Economic Zone Authority (PEZA) – Issued guidelines for pharmazones to streamline regulatory processes, reduce drug prices, and attract global pharmaceutical investors, offering tax incentives to developers and registered business enterprises.

-

Other participants include a range of international API suppliers, local generic API manufacturers, and emerging biotech firms focused on biosimilars and monoclonal antibodies.

These players compete on cost, quality, regulatory compliance, and supply chain reliability. The market is seeing increasing vertical integration and partnerships between local manufacturers and international technology providers.

Regional Analysis

Regional dynamics within the Philippines active pharmaceutical ingredients (APIs) market are shaped by the concentration of industrial zones, manufacturing facilities, and research institutions.

-

Luzon is the largest market region, hosting the Luisita Industrial Park Special Economic Zone in Tarlac, where Zen LifeSciences is building its ₱1.2 billion facility. The region also has the highest concentration of pharmaceutical manufacturing plants and is the primary destination for FDI in the sector.

-

Visayas is an emerging market, with potential for pharmaceutical logistics and distribution hubs, supported by improving infrastructure and connectivity.

-

Mindanao is a growing market, with the Aurora Pacific Economic Zone in Casiguran positioning itself as a potential pharmaceutical investment hub, offering land, infrastructure, and incentives for R&D, clinical trials, and cold chain logistics.

Recent Industry Developments

-

March 2025: PEZA issued guidelines for the establishment and registration of pharmaceutical economic zones (pharmazones), outlining incentives to attract pharma, medical, and healthcare‑related investments and position the Philippines as a competitive player in the global pharmaceutical market.

-

January 2026: Filipino‑owned Zen LifeSciences Inc. signed a registration agreement with PEZA to build a ₱1.2 billion export‑oriented pharmaceutical manufacturing facility at the Luisita Industrial Park Special Economic Zone in Tarlac, with commercial operations expected in January 2027.

-

May 2026: APECO announced it is exploring the establishment of a pharmaceutical investment hub in Casiguran town, with potential activities including R&D, clinical trials, cold chain logistics, and warehousing, widening access to medicines and creating high‑value investment opportunities.

-

2025 (Throughout): The Bureau of Internal Revenue expanded the list of VAT‑exempt medicines to 2,263 items, covering treatments for cancer, diabetes, and other chronic conditions, reducing retail costs and encouraging higher demand.

-

2025 (Throughout): BMI forecast that generic medicines will account for 54 percent of Philippine pharmaceutical sales by 2030, up from 51 percent in 2025, with the segment growing at an 8.8 percent compound annual rate, reaching ₱409 billion.

Browse Full Report with TOC & List of Figures for In‑Depth Market Insights: https://www.imarcgroup.com/philippines-active-pharmaceutical-ingredients-market

Note: If you need any specific information that is not covered currently within the scope of the report, we will provide the same as a part of customisation.

About Us

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us

IMARC Group

134 N 4th St., Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No.: (D) +91 120 433 0800

United States: +1-201-971-6302

What's Your Reaction?