Australia Data Center Market Size, Share, Report 2026 2034

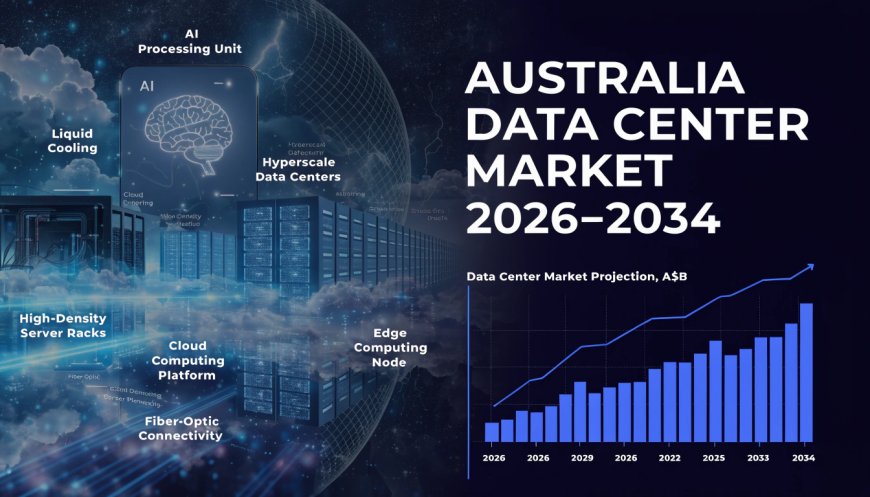

Australia data center market size was valued at USD 4.8 Billion in 2025 and is projected to reach USD 8.2 Billion by 2034, exhibiting a CAGR of 5.47% during the forecast period 2026-2034.

Market Overview

The Australia data center market size was valued at USD 4.8 Billion in 2025 and is projected to reach USD 8.2 Billion by 2034, exhibiting a CAGR of 5.47% during the forecast period 2026‑2034. Surging cloud adoption, AI and high‑performance computing workloads, 5G network rollout, and government digital sovereignty mandates are key growth enablers. AirTrunk's AUD 24 Billion acquisition by Blackstone in 2024 underscored the scale of investor appetite for Australian hyperscale capacity.

This market is strategically important to Australia's digital economy, providing the foundational infrastructure for cloud computing, artificial intelligence, and data sovereignty. Australia's total data center occupancy has grown from 37MW in 2005 to 1,315MW in 2025, with 67% of that growth occurring in the past five years.

The Australia data center market is poised for sustained expansion, driven by AI workload demand, hyperscale capacity build-out, and digital sovereignty mandates. With a projected CAGR of 5.47% through 2034, the market presents significant opportunities for operators focusing on AI‑ready facilities, edge computing, and renewable energy integration.

AUSTRALIA DATA CENTER MARKET SUMMARY

- The Australia data center market encompasses the full spectrum of physical infrastructure facilities, including servers, storage systems, networking equipment, power and cooling systems, and security infrastructure that house and process digital data for cloud, enterprise, and government applications.

- The ecosystem spans data center developers, colocation providers, hyperscale operators (AWS, Microsoft Azure, Google Cloud), managed service providers, enterprise IT departments, and government digital agencies.

- Solution commands the dominant component share at 63.8% in 2025, supported by demand for server, storage, and network hardware across hyperscale and colocation deployments. Services follow at 36.2%, lifted by managed hosting, consulting, and integration revenues.

- Hyperscale dominates the type segment at 41.6% in 2025, reflecting AWS, Microsoft Azure, and Google Cloud regional expansion.

- Australian Capital Territory and New South Wales dominate regionally at 36.5% in 2025, anchored by Sydney's position as the country's largest cloud availability zone.

- Queensland is the fastest‑growing region at a CAGR of ~6.8%, reflecting emerging edge computing deployments supporting regional digital services.

PORTER'S FIVE FORCES ANALYSIS – AUSTRALIA DATA CENTER MARKET

The competitive dynamics of the Australia data center market can be analysed using Porter's Five Forces framework.

Bargaining Power of Suppliers – Moderate to High

- Data center operators rely on specialised suppliers for power infrastructure, cooling systems, networking hardware, and real estate. Rising demand for high‑density AI workloads has increased leverage for suppliers of liquid cooling and advanced chip infrastructure.

Bargaining Power of Buyers – Moderate

- Hyperscale cloud providers (AWS, Microsoft Azure, Google Cloud) represent concentrated buyer segments with significant purchasing volumes, negotiating long‑term, high‑capacity colocation contracts. Enterprise and government clients increasingly prioritise sovereign data requirements and sustainability credentials alongside pricing.

Threat of New Entrants – Moderate

- Significant capital requirements for land acquisition, power infrastructure, grid connection, and regulatory approvals create high barriers. Australia's grid connection lead times (12–18 months) and renewable energy co‑investment requirements add to entry challenges.

Threat of Substitutes – Low

- Edge computing and on‑premise server rooms represent partial substitutes, but the scale, efficiency, and connectivity advantages of large data centers make them irreplaceable for core cloud and AI workloads.

Competitive Rivalry – High (Healthy)

- The market is fragmented, with the top five companies occupying 24.29% of industry revenue. Major players include NEXTDC Ltd., AirTrunk Operating Pty Ltd, Equinix Inc., Digital Realty Trust Inc., CDC Data Centres Pty Ltd, Macquarie Technology Group, DigiCo Infrastructure REIT, Vocus Group, and DCI Data.

Request for Sample Report: https://www.imarcgroup.com/australia-data-center-market/requestsample

MARKET GROWTH DRIVERS

Hyperscale Expansion and AI Workloads Fueling Data Center Demand

Hyperscale dominates the type segment at 41.6% in 2025, reflecting AWS, Microsoft Azure, and Google Cloud regional expansion. AirTrunk's AUD 24 billion acquisition by Blackstone in 2024 underscored the scale of investor appetite for Australian hyperscale capacity. The AI data center sector is forecast to reach significant revenues as Australia's total data center occupancy grows.

Infrastructure Investment and Digital Sovereignty Supporting Market Expansion

The Australian Government's recently released national framework prioritises new data centers that align with "national interest," including data sovereignty, environmental sustainability, and local economic benefits. Sydney leads the upcoming data center market, accounting for nearly 65% of total power capacity, with facilities operating at 85–90% utilisation.

Rising Demand for AI‑Optimised and Edge Computing Facilities

The growing adoption of AI and high‑performance computing workloads is driving demand for specialised, AI‑ready data center facilities. Australian Capital Territory and New South Wales dominate with a 36.5% share in 2025, led by Sydney's position as the country's largest cloud availability zone.

AUSTRALIA DATA CENTER MARKET SEGMENTATION

Segmentation analysis provides a detailed view of the Australia data center market by category:

- Component Insights: Solution (63.8% share in 2025), Services (36.2% share).

- Type Insights: Hyperscale (41.6% share), Colocation, Edge, Others.

- Enterprise Size Insights: Large Enterprises, Small and Medium Enterprises (SMEs).

- End User Insights: Cloud Providers, BFSI, IT and Telecom, Government, Healthcare, Retail, Others.

- Regional Insights: Australia Capital Territory & New South Wales (36.5% share), Victoria & Tasmania (24.8% share), Queensland (16.3% share, fastest‑growing at ~6.8% CAGR), Northern Territory & Southern Australia, Western Australia.

COMPETITIVE LANDSCAPE

The competitive landscape of the Australia data center market is fragmented, with the top five companies occupying 24.29% of industry revenue. Major players in the market include NEXTDC Ltd., AirTrunk Operating Pty Ltd, Equinix Inc., Digital Realty Trust Inc., CDC Data Centres Pty Ltd, Macquarie Technology Group, DigiCo Infrastructure REIT, Vocus Group, and DCI Data. Strategic developments are shaping the competitive landscape, notably Blackstone's AUD 24 billion acquisition of AirTrunk (2024), representing the largest leveraged buyout of 2024 in the Asia‑Pacific region. Investment opportunities exist in specialised AI‑ready facilities, edge computing nodes, and renewable energy‑integrated data centers.

REGIONAL ANALYSIS

- Australia Capital Territory & New South Wales leads the market with a 36.5% revenue share (2025), anchored by Sydney's position as the country's largest cloud availability zone.

- Victoria & Tasmania holds a 24.8% revenue share, driven by Melbourne's growing digital infrastructure and strong enterprise cloud migration.

- Queensland, with a 16.3% share, is the fastest‑growing region at a CAGR of ~6.8%, reflecting emerging edge computing deployments supporting regional digital services.

- Western Australia sees demand from the resources sector and growing data center infrastructure investment.

- Northern Territory & Southern Australia, though smaller in market share, are seeing growth from digital connectivity and logistics infrastructure developments.

RECENT INDUSTRY DEVELOPMENTS

- 2025 Activity: The Australia data center market continued its strong growth trajectory from USD 4.8 Billion in 2025 to USD 8.2 Billion by 2034.

- 2024 Activity: AirTrunk's AUD 24 Billion acquisition by Blackstone underscored the scale of investor appetite for Australian hyperscale capacity.

- 2025 Activity: Hyperscale expansion and AI workloads continued to fuel data center demand, with Queensland emerging as the fastest‑growing region at a CAGR of ~6.8%.

Note: If you need any specific information that is not covered currently within the scope of the report, we will provide the same as a part of customization.

https://www.imarcgroup.com/request?type=report&id=24647&flag=C

Report Format, Delivery, and Customization Details

Report Format Mode: PPT, PDF, and Excel

Report Delivery Mode: Online Delivery, Physical Delivery

Report Delivery Time: Report Delivered Over Email within 24 to 48 hours. If requested by the client, a physical copy will be delivered within three to ten days.

Report Confirmation Mode: Yes via Email

Report Customization Mode: Yes via Email / Call

Report Table of Content: Yes

Report List of Figures: Yes

Report Methodology Mode: Yes

Request For Sample Report: Yes

What's Your Reaction?