Australia Sodium Cyanide Market: Size, Share, Trends, Analysis, Growth & Forecast to 2026-2034

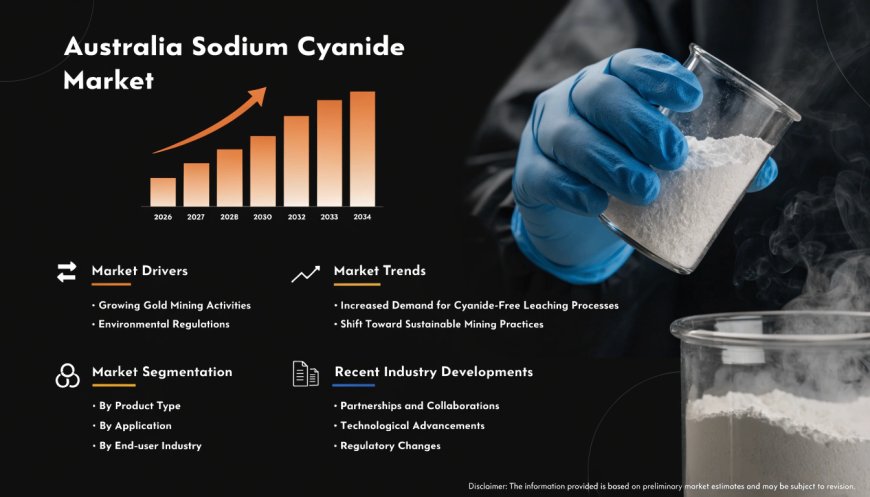

The Australia sodium cyanide market size was valued at USD 61.06 Million in 2025 and is projected to reach USD 115.64 Million by 2034, growing at a compound annual growth rate of 7.35% from 2026-2034.

Market Overview

The Australia sodium cyanide market is witnessing robust growth driven by the nation's position as the world's second‑largest gold producer, record‑high precious metal prices fueling extraction activity, and sustained investment in domestic manufacturing capacity. According to IMARC Group, the market size was valued at USD 61.06 Million in 2025 and is projected to reach USD 115.64 Million by 2034, exhibiting a compound annual growth rate (CAGR) of 7.35% during 2026‑2034. Gold miners in Western Australia (WA) are aggressively ramping up operational activity as bullion prices climb to new heights. Australia is the second‑largest gold producer globally, with about 4.7 million ounces of gold produced in 2025. This market is strategically important to Australia's economy as it directly supports the nation's gold mining sector, which generates substantial export earnings, creates high‑value employment, and contributes to economic resilience and resource sovereignty.

The Australia sodium cyanide market is poised for sustained expansion, driven by a projected CAGR of 7.35% through 2034, record‑high gold prices, and major production capacity expansions. With leading manufacturers scaling up output to serve both domestic mines and export markets, the market presents significant opportunities for stakeholders focused on efficient, safe, and environmentally responsible supply chains, as well as for downstream customers seeking reliable procurement channels.

Australia Sodium Cyanide Market Summary

The Australia sodium cyanide market encompasses the production, distribution, and consumption of sodium cyanide, a highly effective lixiviant used predominantly in gold extraction via cyanidation, as well as in chemical synthesis, electroplating, and certain pharmaceutical applications.

- By product type, solid sodium cyanide dominates the market with a share of 58.7% in 2025, owing to its superior stability during transportation, ease of storage in remote mining regions, and consistent dissolution properties that enable precise dosage control in gold extraction processes.

- By industry, mining leads the market with a share of 72.4% in 2025, driven by Australia's position as the second‑largest gold producer globally, extensive mining operations in Western Australia, and continued reliance on cyanidation as the primary gold extraction methodology.

- By sales channel, direct sales hold the largest segment with a market share of 61.2% in 2025, reflecting the preference of large‑scale mining operators for direct procurement arrangements that ensure supply security, competitive pricing, and tailored logistics for sodium cyanide delivery.

- By region, Western Australia represents the leading market with a share of 41.8% in 2025, driven by the concentration of major gold mining operations including Boddington, Super Pit, and Jundee mines, combined with proximity to key sodium cyanide manufacturing facilities in Kwinana.

The ecosystem includes domestic producers, raw material importers, logistics and supply chain partners, regulatory bodies, and end‑users comprising large‑scale gold mining operators, industrial chemical consumers, and export partners.

PORTER'S FIVE FORCES ANALYSIS – AUSTRALIA SODIUM CYANIDE MARKET

The competitive dynamics of the Australia sodium cyanide market can be analyzed using Porter's Five Forces framework.

Bargaining Power of Suppliers – Moderate

The market relies on a mix of domestic production and limited imports of sodium cyanide and its precursors. Major blenders maintain multi‑source procurement across Asia-Pacific refineries to manage supply risk. Australia is a net importer of base oils and additive packages, with domestic production limited to blending and formulation of imported intermediates.

Bargaining Power of Buyers – Moderate

Stringent OEM specifications—including API SP, ILSAC GF-6, and equipment-specific approvals from Caterpillar, Komatsu, and Siemens—limit switching to lower-cost alternatives, creating product loyalty. Fleet operators and mining companies increasingly prioritize total cost of ownership, recognizing that premium synthetic lubricants with extended drain intervals deliver measurable savings in equipment downtime and maintenance costs.

Threat of New Entrants – Low to Moderate

Significant capital requirements for blending plants, OEM approval certifications, and nationwide distribution networks across Australia's vast geography create high barriers; established players like Castrol, Shell, and Fuchs Australasia hold decades of brand equity. However, innovation-led entrants like GMG (graphene technology) and LIQUI MOLY demonstrate the market remains accessible to genuinely differentiated technology and branding propositions.

Threat of Substitutes – Low

Electric vehicles are gradually reducing traditional engine oil requirements, but Australia's vast installed base of combustion vehicles—particularly in mining, agriculture, and regional transport—ensures baseline lubricant demand for years ahead. The EV transition is creating entirely new product categories in thermal management fluids and driveline lubricants, turning substitution into market expansion for diversified suppliers.

Competitive Rivalry – High (Healthy)

Multi‑tier competition spans multinational leaders (Castrol Holdings, Viva Energy/Shell, Ampol/Chevron), specialized players (Penrite Oil, FUCHS, LIQUI MOLY), and technology disruptors—driving differentiation through product innovation, sustainability credentials, and digital service offerings rather than destructive price competition.

Request for Sample Report: https://www.imarcgroup.com/australia-sodium-cyanide-market/requestsample

MARKET GROWTH DRIVERS

Record‑High Gold Prices and Expanding Mining Activity

A primary factor propelling the Australia sodium cyanide market is the unprecedented rise in global gold prices, which has motivated miners to increase output and invest in efficient extraction processes. Australia's gold export earnings rose 42% to AUD 47 Billion in 2024–25, with forecasts projecting earnings to reach AUD 69 Billion in 2025–26. Western Australia (WA) is a global leader in gold production, producing nearly two‑thirds of all gold mined in Australia. This sustained growth in mining activity creates a robust and expanding market for sodium cyanide, driving consistent consumption across established and new mine sites.

Strategic Capacity Expansions and Investment in Domestic Manufacturing

The Australia sodium cyanide market is also benefiting from significant investment in domestic production capacity. AGR is undertaking a major expansion of its Kwinana facility, increasing annual sodium cyanide solution capacity by over 30% to approximately 130,000 tonnes per annum. Orica, another major manufacturer, has an annual production capacity of 95,000 tonnes at its Yarwun facility in Queensland. These capacity enhancements ensure a reliable domestic supply chain and position Australia as a significant exporter of sodium cyanide, particularly to gold‑producing regions in Asia, Africa, the Americas, and the Middle East.

Increasing Demand for Low‑Grade Ore Processing

As higher‑grade gold deposits become depleted, mining companies are increasingly processing lower‑grade ores, which require higher volumes of sodium cyanide per unit of gold recovered. This trend is expected to drive additional demand growth. AGR forecasts that its sales to local mines will increase from 54,000 tonnes to 73,000 tonnes within a few years, and likely grow well beyond that towards 2030. This increased demand is driven by the need to process larger volumes of ore to maintain gold output, as well as the development of new gold mining projects across Australia.

Australia Sodium Cyanide Market Segmentation

Segmentation analysis provides a detailed view of the Australia sodium cyanide market by category:

- Product Type Insights: Solid Sodium Cyanide (58.7% share in 2025), Liquid/Solution Sodium Cyanide

- Industry Insights: Mining (72.4% share in 2025), Industrial (Chemical) and Others

- Sales Channel Insights: Direct Sales (61.2% share in 2025), Indirect Sales (Distributors, etc.)

- Form Insights: Solid, Liquid

- Regional Insights: Western Australia (41.8% share in 2025), New South Wales, Queensland, Northern Territory & Southern Australia, Victoria and Tasmania

Competitive Landscape

The competitive landscape of the Australia sodium cyanide market is moderately concentrated, with two major domestic producers serving both local and international mining operations. Key companies and strategic developments include:

- Australian Gold Reagents (AGR) – Owned 75% by Wesfarmers and the remainder by Coogee Chemicals. The company is undergoing a major expansion of its Kwinana facility, increasing annual sodium cyanide solution capacity by over 30% to approximately 130,000 tonnes per annum, positioning AGR as the world's third‑largest sodium cyanide producer for gold mining operations. The expansion includes a new low‑emissions incinerator, enhanced water recycling (over 70%), and exploration of waste‑heat‑to‑electricity generation.

- Orica – Among the world's leading producers of sodium cyanide, with an annual production capacity of 95,000 tonnes at its Yarwun facility in Queensland. The facility operates in full compliance with the International Cyanide Management Code. Orica is the world's leading supplier of sparged sodium cyanide, offering both solid and liquid forms.

- CSBP – AGR is a joint venture between CSBP (a subsidiary of Wesfarmers) and Coogee Chemicals, with CSBP holding a 75% interest. CSBP brings significant industrial expertise and resources to the sodium cyanide production value chain.

Regional Analysis

Regional dynamics within the Australia sodium cyanide market are shaped by the concentration of gold mining activity and proximity to manufacturing facilities.

- Western Australia is the leading region, accounting for 41.8% of the market in 2025. WA produces nearly two‑thirds of all gold mined in Australia, with major operations including Boddington, the Super Pit (Kalgoorlie), Jundee, and numerous other sites. The region also hosts the key sodium cyanide manufacturing facility in Kwinana, ensuring a tightly integrated supply chain.

- New South Wales is a growing market, supported by emerging gold projects such as Mount Hope Mining's Mt Solitary deposit in the Cobar Basin, which has demonstrated strong cyanide amenability, offering potential for low‑capital development pathways.

- Queensland is home to Orica's Yarwun sodium cyanide facility, serving both domestic and export markets. The state hosts several gold mining operations that contribute to demand.

- Northern Territory & Southern Australia and Victoria & Tasmania, while smaller in terms of overall consumption, contribute to the national market through existing mine sites and exploration projects, with potential for future growth as gold prices remain elevated.

Recent Industry Developments

- March 2026: AGR's Board made a final investment decision to proceed with the expansion of its Kwinana sodium cyanide production facility, positioning AGR as one of the world's largest sodium cyanide producers for the gold mining industry.

- March 2026: Sodium cyanide prices in Australia reached USD 2,118 per metric tonne, with sufficient production levels and stable mining demand supporting a well‑balanced market.

- November 2025: AGR's Sodium Cyanide Plant Expansion Project moved from the engineering phase into construction, achieving an early milestone. The project includes a major concrete slab pour requiring 400m³ of concrete, 63 truckloads, and 30 personnel to complete.

- September 2025: Sodium cyanide prices in Australia remained relatively stable at USD 2,163 per metric tonne in Q2 2025, with demand from the Australian gold mining industry, particularly in Western Australia, continuing to drive market activity.

- May 2025: AGR lodged a further application to expand production at its Kwinana plant from 170,000 tonnes per annum to 210,000 tonnes per annum, targeting both domestic and international markets.

- October 2024: AGR received approval for the next stage of funding for its expansion, three years in the making, which will increase production capacity by around 28,000 tonnes per annum to more than 90,000 tonnes per annum, with first production expected in late 2025.

- February 2025: AGR announced a final investment decision to expand its Kwinana plant, increasing annual sodium cyanide production capacity by over 30% to approximately 130,000 tonnes per annum, including enhanced solids production capacity to facilitate increased exports.

- February 2025: The expansion included a new low‑emissions incinerator, partially funded by a USD 7.5 million Federal Government grant, which will enable AGR to significantly increase production while reducing greenhouse gas emissions intensity by approximately 28% and recycling over 70% of wastewater onsite.

Browse Full Report with TOC & List of Figures for In‑Depth Market Insights: https://www.imarcgroup.com/australia-sodium-cyanide-market

Note: If you need any specific information that is not covered currently within the scope of the report, we will provide the same as a part of customisation.

About Us

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us

IMARC Group

134 N 4th St., Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No.: (D) +91 120 433 0800

United States: +1-201-971-6302

What's Your Reaction?