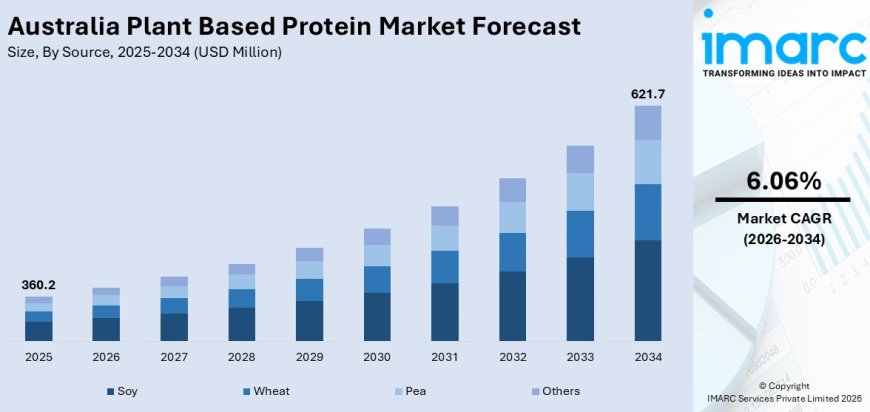

Australia Plant Based Protein Market Projected to Reach USD 621.7 Million by 2034

Australia plant based protein market size reached USD 360.2 Million in 2025. Looking forward, the market is projected to reach USD 621.7 Million by 2034, exhibiting a growth rate (CAGR) of 6.06% during 2026-2034.

Market Overview

The Australia plant based protein market is witnessing strong growth driven by rising health and wellness awareness among Australian consumers, increasing environmental concerns regarding the carbon footprint and water usage of animal agriculture, and a growing shift toward vegan, vegetarian, and flexitarian lifestyles across the nation. The market size reached USD 360.2 Million in 2025 and is projected to reach USD 621.7 Million by 2034, exhibiting a compound annual growth rate (CAGR) of 6.06% during 2026‑2034. This market is strategically important to Australia's agricultural and food technology economy, supporting innovation in alternative proteins, sustainable farming practices, and value‑added processing while strengthening the nation's position as a reliable supplier of clean, high‑quality plant‑based ingredients to both domestic and international markets.

The Australia plant based protein market is poised for sustained expansion, driven by health consciousness, environmental awareness, and growing retail accessibility. With a projected CAGR of 6.06% through 2034, the market presents significant opportunities for food manufacturers focusing on sports nutrition, export growth, and product innovation across meat and dairy alternatives.

AUSTRALIA PLANT BASED PROTEIN MARKET SUMMARY

- The Australia plant based protein market encompasses a broad range of protein products derived from plant sources, including soy, wheat, pea, and other plant materials, used across food, feed, and performance nutrition applications.

- The ecosystem spans plant protein producers, ingredient manufacturers, food processors, retailers (supermarkets and grocery stores), foodservice venues (restaurants, cafes, fast‑food chains), and export partners, supported by advancements in extraction and formulation technologies.

- Major segments identified in the plant based protein industry include source (soy, wheat, pea, others), type (concentrates, isolates, textured), nature (conventional, organic), application (food including meat alternatives, dairy alternatives, bakery alternatives, performance nutrition, convenience foods, others, and feed), and region (Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia).

- The market is fueled by the growing health awareness among consumers, with environmental issues including the need to lower carbon footprints and save water resources also encouraging consumers to shift toward plant‑based protein sources.

PORTER'S FIVE FORCES ANALYSIS – AUSTRALIA PLANT BASED PROTEIN MARKET

The competitive dynamics of the Australia plant based protein market can be analyzed using Porter's Five Forces framework.

Bargaining Power of Suppliers – Moderate

- Plant protein manufacturers rely on agricultural suppliers for raw materials including soy, wheat, peas, chickpeas, and hemp. Australia's established agricultural sector provides multiple sourcing options, balancing supplier influence.

- However, the increasing demand for organic and sustainably sourced raw materials gives certain specialty crop suppliers moderate leverage.

Bargaining Power of Buyers – Moderate

- Australian consumers benefit from extensive choice across supermarkets, specialty stores, and online platforms, with major retailers committing greater shelf space to plant‑based products and expanding their plant‑based categories.

- Food manufacturers and foodservice operators represent concentrated purchasing channels that negotiate volume‑based contracts, while the growing availability of plant‑based options in restaurants, cafes, and fast‑food chains provides buyers with alternative sourcing options.

Threat of New Entrants – Moderate

- Significant capital requirements for processing facilities, extraction technology, R&D, and regulatory compliance create barriers to entry. However, innovation‑led entrants focusing on novel protein sources (hemp, chickpea) or specialized formulations for sports nutrition are successfully accessing the market.

- Advancements in processing technology allowing for higher protein yields and improved taste and texture are reducing some traditional entry barriers.

Threat of Substitutes – Low to Moderate

- Traditional animal‑based proteins represent the primary substitute category, but the growing consumer shift toward plant‑based options driven by health, environmental, and ethical considerations continues to expand plant protein adoption.

- Hybrid developments involving plant proteins combined with conventional meats are also growing due to the rise of flexitarians, converting potential substitution into complementary market expansion.

Competitive Rivalry – High (Healthy)

- The market features intensifying competition among established plant protein producers, innovative startups, and mainstream food companies expanding into plant‑based product lines.

- Competition is driven by product taste and texture authenticity, nutritional profile, sustainability credentials, brand recognition, and distribution reach rather than purely price‑based rivalry.

Request a Business Sample Report for Procurement & Investment Evaluation:

https://www.imarcgroup.com/australia-plant-based-protein-market/requestsample

MARKET GROWTH DRIVERS

Rising Health and Wellness Awareness Among Australian Consumers

Several key factors are propelling market growth in the Australia plant based protein market. The increasing focus on health and wellness among Australian consumers is significantly driving Australia plant based protein market demand. There is a growing interest in diets that are high in protein while low in saturated fats and cholesterol, which corresponds with the health benefits of plant‑based protein. This trend is further supported by the need to combat lifestyle‑related illnesses such as obesity, diabetes, and heart disease. Additionally, consumers are attracted to plant‑based options due to their high fiber content, essential amino acids, and potential for weight management. As awareness about the health risks associated with excessive animal protein intake grows, the transition to plant‑based diets is becoming more mainstream, thereby enhancing market growth across retail, foodservice, and packaged product sectors.

Increasing Vegan and Flexitarian Population

Australia has experienced a consistent increase in both the vegan and flexitarian populations, which substantially boosts the consumption of plant‑based protein. The vegan movement has shifted from a niche market to a broader appeal, with many consumers choosing a fully plant‑based diet for health, ethical, or environmental reasons. Meanwhile, flexitarianism—where individuals cut back on but do not entirely remove animal products—has gained popularity, expanding the potential consumer base for plant‑based protein products. This change is driven by heightened public discussions on climate change, animal rights, and sustainable living. As awareness continues to grow, food manufacturers and restaurants are increasing their plant‑based offerings, adapting to changing dietary preferences and diversifying their product lines to cater to both dedicated vegans and health‑minded flexitarians.

Sustainability and Ethical Considerations

Sustainability and ethics are major forces behind the Australian plant‑based protein market. Consumers today are cognizant of the environmental consequences of animal agriculture, such as greenhouse gas emissions, land use, and water use. Therefore, there is a shift toward the consumption of plant‑based diets as a way to minimize ecological footprints. In addition, issues regarding animal well‑being and the need to promote cruelty‑free food production are shaping buying habits. As a response, businesses are focusing on the sustainable sourcing and ethical manufacturing of their plant‑based protein products, positioning their offerings in accordance with the values of environmentally and socially responsible consumers.

AUSTRALIA PLANT BASED PROTEIN MARKET SEGMENTATION

Segmentation analysis provides a detailed view of the Australia plant based protein market by category:

- Source Insights: Soy, Wheat, Pea, Others.

- Type Insights: Concentrates, Isolates, Textured.

- Nature Insights: Conventional, Organic.

- Application Insights: Food (Meat Alternatives, Dairy Alternatives, Bakery Alternatives, Performance Nutrition, Convenience Foods, Others), Feed.

- Regional Insights: Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia.

COMPETITIVE LANDSCAPE

The competitive landscape of the Australia plant based protein market is dynamic, featuring a growing number of plant protein producers, innovative startups, and mainstream food companies expanding into plant‑based product lines. The market research report has provided a comprehensive analysis of the competitive landscape, including market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant, with detailed profiles of all major companies provided in the full report. Key participants in the plant based protein industry include established Australian plant protein producers and emerging innovation‑focused firms.

Strategic developments are shaping the competitive arena. In March 2025, My Co, the investment arm of the Paule Family Office concentrating on FABtech (Food, Agri & Bio) start‑ups, purchased plant‑based protein production firm Australian Plant Proteins (APP). APP was the initial company in Australia to create and market a plant protein isolate powder. It leads in cutting‑edge plant‑based protein innovations and is crucial in establishing Australia's status—and reputation—internationally in this expanding sector. Investment opportunities exist in sports nutrition product development, export expansion into Asia‑Pacific markets, and novel protein source innovation.

REGIONAL ANALYSIS

- Australia Capital Territory & New South Wales represents a critical demand centre, anchored by Sydney's large consumer base, high density of health‑conscious shoppers, and strong retail infrastructure supporting plant‑based product availability across supermarkets, specialty stores, and foodservice venues.

- Victoria & Tasmania benefits from Melbourne's reputation as a hub for food innovation and plant‑based dining, with strong demand for meat and dairy alternatives across both retail and hospitality sectors.

- Queensland experiences rising plant‑based protein demand driven by Brisbane's growing population and increasing health awareness, alongside expanding retail presence of plant‑based products.

- Western Australia sees growth from health‑conscious consumers in Perth and the state's agricultural sector, which supports local sourcing of plant protein raw materials.

- Northern Territory & Southern Australia, though smaller in market share, contribute to the national plant‑based protein market through emerging health food retail and growing consumer interest in sustainable dietary options.

RECENT INDUSTRY DEVELOPMENTS

- March 2025: My Co, the investment arm of the Paule Family Office concentrating on FABtech (Food, Agri & Bio) start‑ups, purchased plant‑based protein production firm Australian Plant Proteins (APP). APP was the initial company in Australia to create and market a plant protein isolate powder, leading in cutting‑edge plant‑based protein innovations and playing a crucial role in establishing Australia's international reputation in this expanding sector.

- 2025 Activity: The Australia plant‑based food market, which includes plant‑based protein products, reached USD 330.4 Million in 2024, with projections to reach USD 981.3 Million by 2033 at a CAGR of 11.50%, reflecting strong momentum across the broader plant‑based category.

- 2024 Activity: Major retailers continued to commit greater shelf space to plant‑based protein products, with supermarkets and grocery stores growing their plant‑based categories and foodservice venues including restaurants, cafes, and fast‑food chains incorporating more plant‑based menu items to accommodate changing consumer preferences.

Note: If you need any specific information that is not covered currently within the scope of the report, we will provide the same as a part of customization.

Request For Sample Report:

https://www.imarcgroup.com/request?type=report&id=33895&flag=E

ABOUT US

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

CONTACT US

IMARC Group

134 N 4th St., Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 433 0800

United States: +1 201 971 6302

What's Your Reaction?