Australia MedTech Market Projected to Reach USD 14.0 Billion by 2034

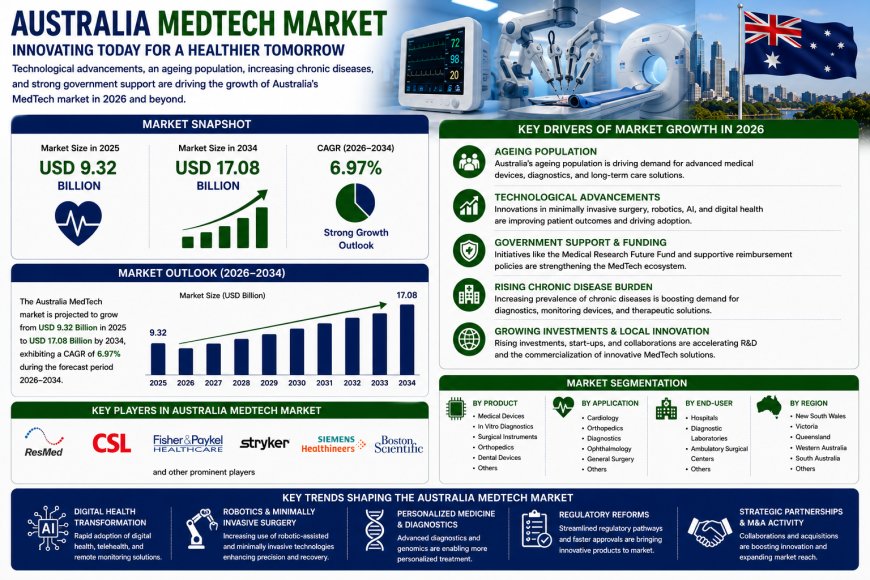

Australia MedTech market size was valued at USD 8.9 Billion in 2025. Looking forward, the market is projected to reach USD 14.0 Billion by 2034, exhibiting a CAGR of 5.00% from 2026‑2034.

The Australia MedTech market size was valued at USD 8.9 Billion in 2025. Looking forward, the market is projected to reach USD 14.0 Billion by 2034, exhibiting a CAGR of 5.00% from 2026‑2034. New South Wales leads the market, driven by robust healthcare infrastructure, extensive research capabilities, government funding, and a thriving innovation ecosystem, fostering advancements in digital health, diagnostics, and medical devices.

The Australia MedTech market growth is fueled by increasing demand for advanced healthcare technologies, driven by an aging population and rising chronic diseases. In addition, increasing government initiatives are funding support innovation, and promoting growth in digital health and telemedicine, which is aiding the market growth. The presence of top-tier research institutions and universities promotes collaboration and the advancement of innovative devices, driving market demand. Strong private sector investment in health technology boosts advancements and increases the shift toward personalized and minimally invasive treatments.

The Australia MedTech market is poised for sustained expansion, driven by digital health transformation, AI integration, and strong government investment. With a projected CAGR of 5.00% through 2034, the market presents significant opportunities for companies focused on remote monitoring, precision diagnostics, and AI‑powered medical solutions.

AUSTRALIA MEDTECH MARKET SUMMARY

- The Australia MedTech market encompasses the full spectrum of medical technologies, including diagnostic devices, therapeutic devices, monitoring devices, supportive devices, imaging systems, surgical instruments, wearable health tech, and prosthetics.

- New South Wales leads the market, driven by robust healthcare infrastructure, extensive research capabilities, government funding, and a thriving innovation ecosystem.

- The 2024 ResMed Global Sleep Survey examined 17 markets worldwide and found that 46% of participants received a diagnosis of obstructive sleep apnea (OSA) in their past, highlighting the growing awareness of sleep health and driving demand for diagnostic and therapeutic MedTech solutions.

- Monash University partnered with Apollo Hospitals to advance digital health research, fostering innovation in healthcare technology and strengthening international collaborations.

- Key digital health trends include telemedicine, remote patient monitoring, wearable devices, and AI‑driven health solutions.

- Australia’s position as a hub for MedTech startups fosters innovation and market entry, with enhanced funding for clinical trials supporting new product development.

PORTER'S FIVE FORCES ANALYSIS – AUSTRALIA MEDTECH MARKET

The competitive dynamics of the Australia MedTech market can be analysed using Porter's Five Forces framework.

Bargaining Power of Suppliers – Moderate

- MedTech companies rely on specialised suppliers for components, raw materials, and software platforms. The global nature of supply chains provides multiple sourcing options, but high‑precision components for imaging systems and surgical instruments have limited suppliers, giving them moderate leverage. Australia's strong research institutions and university collaborations provide access to cutting‑edge innovation and talent, balancing supplier influence.

Bargaining Power of Buyers – Moderate to High

- Australia's healthcare system, including public hospitals, private hospital networks, and diagnostic imaging providers, represents concentrated purchasing channels that negotiate volume‑based contracts for medical devices and technologies. Individual patients and healthcare professionals increasingly influence purchasing decisions through demand for personalised and minimally invasive treatment solutions.

Threat of New Entrants – Moderate

- Significant capital requirements for R&D, clinical trials, regulatory approval (TGA), and commercialization create barriers. However, Australia's position as a hub for MedTech startups fosters innovation and market entry, with startups flourishing thanks to innovation hubs and grant schemes from federal and state governments. Niche entrants focused on AI diagnostics, digital health platforms, and wearable monitoring are successfully accessing the market with differentiated propositions.

Threat of Substitutes – Low

- Traditional treatment methods may compete with some MedTech solutions, but the shift toward digital health, telemedicine, and AI‑powered diagnostics continues to expand MedTech adoption rather than face displacement. The growing demand for personalised medicine and precision healthcare solutions reinforces the essential role of advanced medical technologies.

Competitive Rivalry – High (Healthy)

- The market features intense competition among global MedTech leaders, established diagnostic providers, and innovative startups. Competition is driven by technological innovation, AI integration, regulatory efficiency, and clinical efficacy rather than purely price‑based rivalry.

Request for Sample Report: https://www.imarcgroup.com/australia-medtech-market/requestsample

MARKET GROWTH DRIVERS

Aging Population and Rising Chronic Disease Burden

The Australia MedTech market growth is fueled by increasing demand for advanced healthcare technologies, driven by an aging population and rising chronic diseases. The growing adoption of wearable medical devices and remote monitoring solutions aligns with Australia's push for better chronic disease management, contributing to market expansion. Continuous advancements in artificial intelligence (AI) and data analytics improve diagnostic accuracy and treatment outcomes, strengthening the Australia MedTech market share.

Strong Government Funding and Digital Health Transformation

Increasing government initiatives are funding support innovation and promoting growth in digital health and telemedicine. Digital health is rapidly transforming the Australia MedTech market trends, with an increased focus on telemedicine, wearable devices, and AI‑driven health solutions. The utilization of remote monitoring systems, especially in chronic disease cases, is increasing due to the growing population and demand for accessible healthcare services.

Strong Private Sector Investment and Startup Ecosystem

Strong private sector investment in health technology boosts advancements and increases the shift toward personalized and minimally invasive treatments. Australia’s position as a hub for MedTech startups fosters innovation and market entry, which is driving the market demand. Enhanced funding for clinical trials supports new product development, thereby propelling the market forward. The increased focus on mental health and wellness also boosts demand for relevant MedTech solutions.

AUSTRALIA MEDTECH MARKET SEGMENTATION

Segmentation analysis provides a detailed view of the Australia MedTech market by category:

- Product Type Insights: Diagnostic Devices, Therapeutic Devices, Monitoring Devices, Supportive Devices.

- Technology Type Insights: Imaging Systems, Surgical Instruments, Wearable Health Tech, Prosthetics.

- Application Area Insights: Hospitals, Clinics, Home Care, Rehabilitation Centers.

- End User Insights: Healthcare Providers, Medical Professionals, Patients, Elderly.

- Regional Insights: New South Wales (leading region), Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia.

COMPETITIVE LANDSCAPE

The competitive landscape of the Australia MedTech market features a dynamic mix of global leaders, established diagnostic providers, and innovative startups driving technological advancement across digital health, AI diagnostics, wearable monitoring, and precision medicine. Australian MedTech companies are increasingly engaging in cross‑border collaborations, spurring development of next‑gen diagnostic and therapeutic tools. The market research report provides comprehensive analysis including market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant. Investment opportunities exist in AI‑powered diagnostic systems, remote monitoring platforms, wearable health devices, and digital health solutions.

REGIONAL ANALYSIS

- New South Wales leads the Australia MedTech market, driven by robust healthcare infrastructure, extensive research capabilities, government funding, and a thriving innovation ecosystem fostering advancements in digital health, diagnostics, and medical devices.

- Victoria benefits from Melbourne's position as a major healthcare and research hub, with strong collaboration between universities, research institutions, and MedTech companies supporting innovation in AI diagnostics and wearable health tech.

- Queensland sees growth from digital health adoption and an expanding healthcare infrastructure serving the state's growing population.

- Western Australia contributes to the MedTech market through emerging MedTech startups and healthcare technology innovation.

- Northern Territory & Southern Australia, though smaller in market share, benefit from improved healthcare access through telemedicine and remote monitoring solutions.

RECENT INDUSTRY DEVELOPMENTS

- 2025 Activity: The Australia MedTech market continued its strong growth trajectory from USD 8.9 Billion in 2025 to USD 14.0 Billion by 2034.

- 2024 Activity: The ResMed Global Sleep Survey found that 46% of participants received a diagnosis of obstructive sleep apnea (OSA) in their past.

- 2025 Activity: Monash University partnered with Apollo Hospitals to advance digital health research, fostering innovation in healthcare technology and strengthening international collaborations.

Note: If you need any specific information that is not covered currently within the scope of the report, we will provide the same as a part of customization.

https://www.imarcgroup.com/request?type=report&id=6064&flag=C

Report Format, Delivery, and Customization Details

Report Format Mode: PPT, PDF, and Excel

Report Delivery Mode: Online Delivery, Physical Delivery

Report Delivery Time: Report Delivered Over Email within 24 to 48 hours. If requested by the client, a physical copy will be delivered within three to ten days.

Report Confirmation Mode: Yes via Email

Report Customization Mode: Yes via Email / Call

Report Table of Content: Yes

Report List of Figures: Yes

Report Methodology Mode: Yes

Request For Sample Report: Yes

What's Your Reaction?