Australia Meat Market 2026 | Worth USD 34.39 Billion by 2034

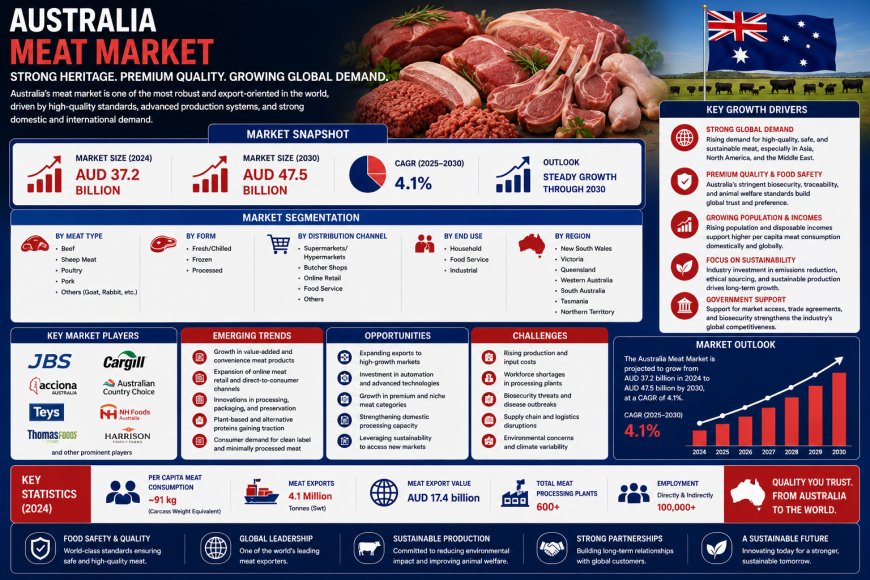

Australia meat market size was valued at USD 29.15 Billion in 2025 and is projected to reach USD 34.39 Billion by 2034, growing at a compound annual growth rate of 1.85% from 2026-2034.

Market Overview

The Australia meat market is underpinned by robust domestic consumption patterns, a well-established livestock production infrastructure, and expanding export opportunities across global markets. The market size was valued at USD 29.15 Billion in 2025 and is projected to reach USD 34.39 Billion by 2034, growing at a compound annual growth rate (CAGR) of 1.85% from 2026‑2034. The sector benefits from favourable climatic conditions that support pastoral agriculture, advanced meat processing technologies that ensure quality and traceability, and strategic free trade agreements that facilitate international market access.

This market is strategically important to Australia's agricultural economy, generating substantial rural employment and foreign exchange earnings through diversified export channels. The sector encompasses beef, lamb, pork, poultry, and goat production, supported by extensive grazing lands, modern feedlot facilities, and world-class processing infrastructure. Growing consumer preference for premium and ethically sourced protein products continues to shape Australia meat market share.

The Australia meat market is poised for sustained expansion, driven by growing demand for premium, grass‑fed products and rising exports to discerning international markets. With a projected CAGR of 1.85% through 2034, the market presents significant opportunities for processors focusing on quality assurance, sustainability, and value‑added product development.

AUSTRALIA MEAT MARKET SUMMARY

-

The Australia meat market encompasses a wide range of protein products including beef, lamb, pork, poultry, and goat, supported by extensive grazing lands, modern feedlot facilities, and world‑class processing infrastructure.

-

The ecosystem spans established multinational processing groups, regional family‑owned enterprises, independent butchers, artisanal producers, and a robust cold chain logistics network.

-

Raw dominates the type segment with a share of 64% in 2025, driven by strong household preference for fresh, unprocessed meat cuts suitable for traditional cooking methods and barbecue culture.

-

Beef leads the product segment with a share of 40% in 2025, supported by Australia's status as a leading global beef supplier, robust local demand, and production systems strongly aligned with export markets.

-

Supermarkets and hypermarkets dominate the distribution channel with a share of 60% in 2025, benefiting from extensive retail networks, competitive pricing strategies, and convenient one-stop shopping experiences.

-

Australia Capital Territory & New South Wales represent the largest regional segment with 31% market share in 2025, supported by the highest population concentration and well-developed retail and processing infrastructure.

PORTER'S FIVE FORCES ANALYSIS – AUSTRALIA MEAT MARKET

The competitive dynamics of the Australia meat market can be analysed using Porter's Five Forces framework.

Bargaining Power of Suppliers – Moderate

-

Livestock producers supply the essential raw materials for meat processing. Australia's extensive cattle industry, spanning diverse production systems from northern pastoral operations to southern grain‑finishing regions, provides multiple sourcing options that balance supplier influence. However, climate variability, including recurring droughts and extreme weather events, periodically disrupts livestock production systems, which can temporarily shift leverage toward suppliers.

Bargaining Power of Buyers – Moderate to High

-

Major retail chains command substantial purchasing power and sophisticated supply chain capabilities to negotiate volume‑based pricing and quality specifications. End consumers benefit from extensive choice across supermarket meat counters, independent butchers, specialty retailers, and online platforms, strengthening buyer negotiating power.

Threat of New Entrants – Moderate

-

Significant capital requirements for processing facilities, feedlot operations, export‑certified infrastructure, and regulatory compliance create barriers for new entrants. Major processors maintain extensive supply chain networks capturing significant production volumes. However, independent butchers and artisanal producers continue to serve premium retail and food service segments.

Threat of Substitutes – Low to Moderate

-

Plant‑based and hybrid meat alternatives are gradually expanding, catering to flexitarian consumers seeking reduced conventional meat consumption. However, Australia's high per capita meat consumption patterns, with beef consumption averaging over twenty kilograms per person annually—significantly exceeding global averages—provide strong market resilience.

Competitive Rivalry – High (Healthy)

-

The Australia meat market exhibits a moderately concentrated competitive structure characterised by established multinational processors operating alongside regional and family‑owned enterprises. Major processing groups maintain extensive supply chain networks, feedlot operations, and export‑certified facilities capturing significant production volumes, while independent butchers and specialty retailers capture niche premium segments.

Request for Sample Report: https://www.imarcgroup.com/australia-meat-market/requestsample

MARKET GROWTH DRIVERS

Rise of Premium and Grass‑Fed Meat Products

Australian consumers increasingly prioritise health, sustainability, and ethical sourcing when selecting meat products, driving substantial growth in grass-fed and premium offerings. Grass-fed beef and lamb command premium pricing due to perceived nutritional benefits, including reduced fat profiles and elevated omega-3 content. Enhanced product labelling emphasising natural feeding practices and ethical production processes strengthens consumer confidence. In 2024, Stone Axe Pastoral Company's Margaret River Wagyu achieved the Open Crossbred Steak Champion title at the Wagyu Branded Beef Competition with a marbling score exceeding nine, demonstrating Australia's premium production capabilities.

Strong Export Market Performance and International Demand

Australia's meat industry benefits from robust export demand across global markets. In February 2025, Jack's Creek introduced its premium Wagyu X range of beef into the United Kingdom via Ocado, reflecting the growing international appetite for Australian premium meat products and the sector's capacity to capture value in discerning overseas markets. The beef segment continues to attract investment across feedlot capacity, processing efficiency, and brand building, with a strong emphasis on quality positioning for both domestic consumers and premium international markets.

Technological Advancements in Processing and Quality Assessment

Ongoing investments in automation, artificial intelligence, and labour‑saving technologies are reshaping processing efficiency and addressing workforce constraints. The sector benefits from rigorous quality assurance programmes, including the Meat Standards Australia grading system, ensuring consistent eating experiences and reinforcing Australia's reputation as a reliable global supplier of premium meat products.

AUSTRALIA MEAT MARKET SEGMENTATION

Segmentation analysis provides a detailed view of the Australia meat market by category:

-

Type Insights: Raw (64% share in 2025), Processed.

-

Product Insights: Chicken, Beef (40% share), Pork, Mutton, Others.

-

Distribution Channel Insights: Supermarkets and Hypermarkets (60% share), Departmental Stores, Specialty Stores, Online Stores, Others.

-

Regional Insights: Australia Capital Territory & New South Wales (31% share), Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia.

COMPETITIVE LANDSCAPE

The competitive landscape of the Australia meat market exhibits a moderately concentrated structure with established processing conglomerates competing alongside regional operators. Major processors maintain extensive supply chain networks, feedlot operations, and export-certified facilities, while independent butchers and specialty retailers capture niche premium segments. The market research report provides a comprehensive analysis of the competitive landscape, including market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant, with detailed profiles of all major companies provided in the full report. Investment opportunities exist in value-added processing, sustainability certifications, and export market expansion.

REGIONAL ANALYSIS

-

Australia Capital Territory & New South Wales represent the largest segment with 31% market share in 2025, supported by the highest population concentration and well-developed retail and processing infrastructure.

-

Victoria benefits from Melbourne's position as a major food processing hub, with strong demand for premium and ethically sourced meat products.

-

Queensland experiences strong meat demand driven by the state's extensive cattle industry and growing population centres including Brisbane and the Gold Coast.

-

Western Australia sees demand from Perth's expanding population and the state's agricultural sector.

-

Northern Territory & Southern Australia, though smaller in market share, contribute to the national meat market through cattle production and growing retail infrastructure.

RECENT INDUSTRY DEVELOPMENTS

-

2025 Activity: The Australia meat market continued its steady growth trajectory, underpinned by robust domestic consumption patterns and expanding export opportunities across global markets.

-

November 2025: JBS Australia achieved an industry first by securing AUS‑MEAT's Facility Objective Carcase Measurement (OCM) Device Approval for MEQ Solutions' cold carcase grading camera, representing a significant advancement in carcase assessment technology.

-

November 2025: Cargill completed its full acquisition of Teys Australia, increasing ownership to one hundred percent following regulatory approvals.

-

February 2025: Jack's Creek introduced its premium Wagyu X range of beef into the United Kingdom via Ocado, reflecting the growing international appetite for Australian premium meat products.

-

February 2025: Meat and Livestock Australia, through its Aussie Beef and Lamb brand, made a prominent return to Gulfood in Dubai, marking fifty years of Australian red meat presence in the Middle East.

-

2024 Activity: Record production volumes reached over 2.57 million tonnes, representing the highest annual output in industry history.

-

2024 Activity: Stone Axe Pastoral Company's Margaret River Wagyu achieved the Open Crossbred Steak Champion title at the Wagyu Branded Beef Competition with a marbling score exceeding nine.

Note: If you need any specific information that is not covered currently within the scope of the report, we will provide the same as a part of customization.

https://www.imarcgroup.com/request?type=report&id=31741&flag=C

ABOUT US

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

CONTACT US

IMARC Group

134 N 4th St., Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 433 0800

United States: +1 201 971 6302

What's Your Reaction?