Australia Germanium Market Share, Trends & Forecast 2026-2034

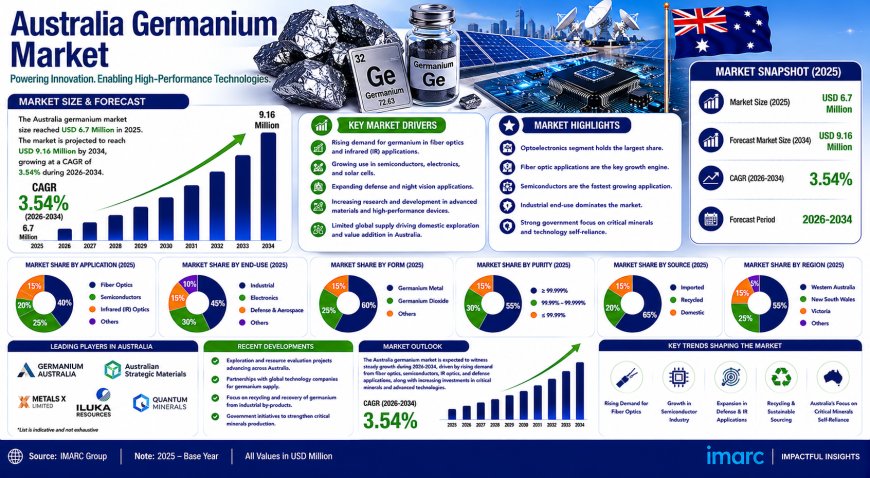

According to IMARC Group, the market size reached USD 6.7 Million in 2025 and is projected to reach USD 9.16 Million by 2034, exhibiting a compound annual growth rate (CAGR) of 3.54% during 2026 2034

Market Overview

The Australia germanium market is witnessing strong growth driven by the rapid expansion of fiber optic networks supporting 5G infrastructure deployment, strategic government initiatives to reduce dependence on foreign critical mineral supplies through domestic extraction from zinc ore by-products, and the rising need for germanium substrates in multi-junction solar cells with high efficiency for space and satellite applications. According to IMARC Group, the market size reached USD 6.7 Million in 2025 and is projected to reach USD 9.16 Million by 2034, exhibiting a compound annual growth rate (CAGR) of 3.54% during 2026‑2034. The increasing adoption of infrared optics in defense and autonomous vehicle systems is also expanding the Australia germanium market share. This market is strategically important to Australia’s economy as it supports the nation’s technological sovereignty, telecommunications infrastructure development, space industry growth, and defense modernization objectives.

Australia Germanium Market Summary

- The Australia germanium market encompasses the production, distribution, and consumption of germanium, a strategic critical mineral essential for fiber optics, infrared optics, electronics, and solar cell applications.

- The market ecosystem currently features complete import dependence, with no current domestic primary production or refining operations, but is evolving as government initiatives encourage domestic processing capability development.

- Major segments identified in the germanium industry include type (germanium ingot, germanium tetrachloride, high purity GeO₂, and others) and application (PET, electronics and solar, fiber optics, IR optics, and others).

- The market is driven by telecommunications sector investments in fiber optic infrastructure to support nationwide 5G rollouts, strategic government initiatives for domestic critical mineral extraction and processing, growing demand for high-efficiency solar cells in space and satellite applications, and increasing adoption of infrared optics in defense and autonomous vehicle systems.

- Australia generates approximately 20 percent of global zinc production from regions such as Western Australia and Queensland, providing a significant domestic resource base for potential germanium extraction as a by-product.

- Government‑backed research initiatives through Geoscience Australia and CSIRO are focusing on extracting germanium from existing zinc mining operations, establishing technical and economic frameworks for Australia to transition from complete import dependence to partial domestic production.

PORTER'S FIVE FORCES ANALYSIS – AUSTRALIA GERMANIUM MARKET

Bargaining Power of Suppliers – High

- Australia is completely dependent on imports for germanium supplies, with no current domestic primary production or refining operations. The competitive landscape is dominated by international suppliers, primarily from China, Belgium, and other established germanium‑producing regions.

- China controls approximately 60 percent of worldwide germanium output and maintains near‑monopoly positions in refining operations. Chinese authorities implemented export restrictions on germanium in August 2023, requiring detailed licensing procedures that can extend from 30 to 80 days per shipment.

- These supply chain vulnerabilities give international suppliers substantial pricing and availability leverage over Australian buyers. However, government‑backed initiatives to develop domestic processing capabilities are creating potential opportunities to rebalance supplier influence over the medium to long term.

Bargaining Power of Buyers – Moderate

- Buyers in the Australia germanium market include telecommunications infrastructure companies, semiconductor device manufacturers, defense systems suppliers, and downstream industrial consumers. These buyers source germanium materials through specialized chemical distributors and materials trading companies that maintain local inventory and provide technical support.

- The highly specialized nature of germanium and its critical role in fiber optic networks, infrared optics, and high‑efficiency solar cells limits switching to alternatives, providing suppliers with some leverage. However, the establishment of long‑term supply agreements and distribution networks helps stabilize buyer‑supplier relationships.

Threat of New Entrants – Moderate (Evolving)

- Capital requirements for germanium extraction and refining are substantial, with hydrometallurgical separation systems, solvent extraction units, and high‑purity refining facilities requiring tens of millions of dollars in investment.

- Recovery yields from zinc concentrates typically range from only 8 to 15 percent of the germanium content, with significant losses occurring during various processing stages, further undermining economic returns.

- However, government initiatives are actively working to de‑risk investment decisions through techno‑economic feasibility studies and pilot‑scale demonstration projects. Research institutions including CSIRO and Geoscience Australia are collaborating with industry partners to attract capital for commercial‑scale extraction facilities, creating an evolving environment that may lower entry barriers for well‑positioned entrants over the forecast period.

Threat of Substitutes – Low

- Germanium possesses unique material properties, including excellent lattice matching with gallium arsenide and other compound semiconductors, enabling the epitaxial growth of complex multi‑layer solar cell structures optimized for space environments.

- In fiber optic applications, germanium tetrachloride serves as a critical precursor material for high‑purity optical fibers essential for long‑distance data transmission and high‑speed internet connectivity. Alternative materials cannot fully replicate germanium's performance characteristics in these demanding applications.

- In infrared optics, germanium provides superior performance for thermal imaging and sensing systems used in defense and autonomous vehicle technologies, with no commercially viable substitutes at equivalent price‑performance levels.

Competitive Rivalry – Low (Import‑Dominated)

- The Australia germanium market currently exhibits low competitive rivalry due to complete import dependence and the absence of domestic production. International suppliers serve Australian customers through distribution networks and direct supply agreements.

- The market environment is evolving as government initiatives encourage domestic processing capability development, creating potential opportunities for mining companies with zinc operations to vertically integrate into germanium recovery.

- Research institutions are actively working with industry partners on techno‑economic feasibility studies and pilot‑scale demonstration projects that could attract capital for commercial‑scale extraction facilities over the coming years.

Request for Sample Report: [No sample request link available on the source page]

MARKET GROWTH DRIVERS

Expansion of Fiber Optic Networks Supporting 5G Infrastructure Development

Several key factors are propelling market growth in the Australia germanium market. The rapid expansion of fiber optic networks supporting 5G infrastructure deployment serves as a powerful demand driver. The Australian telecommunications sector is undergoing a major transformation with substantial investments in fiber optic infrastructure to support nationwide 5G network deployments and enhanced broadband connectivity. Germanium tetrachloride serves as a critical precursor material in the production of high‑purity optical fibers, which form the backbone of modern telecommunications systems. The material's unique properties enable the creation of low‑loss optical fibers essential for long‑distance data transmission and high‑speed internet connectivity. Major telecommunications providers are extending fiber‑to‑the‑premises networks throughout metropolitan and regional areas, accelerated by government efforts such as the Regional Connectivity Program. Global internet traffic is predicted to increase significantly, requiring a strong fiber optic infrastructure, and high‑purity germanium dioxide is essential for fiber optic communication systems and semiconductor doping procedures. This telecommunications infrastructure expansion is establishing a solid foundation for sustained Australia germanium market growth throughout the forecast period.

Strategic Government Initiatives for Domestic Critical Mineral Extraction and Processing

The Australia germanium market growth is also significantly influenced by strategic government initiatives to reduce dependence on foreign critical mineral supplies. The Australian government has identified germanium as a strategic critical mineral essential for technological sovereignty and national security, prompting significant investments in domestic extraction and processing capabilities. Geoscience Australia has launched comprehensive research programs aimed at quantifying the country's germanium resource potential within existing zinc deposits, which are abundant across Western Australia, Queensland, and New South Wales. In November 2024, researchers from CSIRO announced that Australia is exploring the possibility of extracting germanium and gallium as byproducts of zinc and bauxite mining operations. China currently produces 60 percent of global germanium supply, and CSIRO's principal investigator stated that Australia could help reduce supply chain pressures due to the country's high mining rates of minerals needed for germanium production. These government‑backed initiatives are establishing technical foundations and economic frameworks necessary for Australia to transition from complete import dependence to partial domestic production, strengthening supply chain resilience while creating new revenue streams for existing mining operations.

MARKET GROWTH DRIVERS

Growing Demand for High‑Efficiency Solar Cells in Space and Satellite Applications

The Australia germanium market is benefiting from Australia's rapidly expanding space industry, which is driving increased consumption of germanium substrates used in high‑efficiency multi‑junction solar cells that power satellites and space exploration systems. Germanium wafers serve as the foundational substrate material for advanced photovoltaic cells capable of converting sunlight into electricity with efficiency rates exceeding 30 percent, far surpassing conventional terrestrial solar panels. The material's excellent lattice matching properties with gallium arsenide and other compound semiconductors enable the epitaxial growth of complex multi‑layer solar cell structures optimized for the broad spectrum of solar radiation encountered in space environments. Australian space startups and research institutions are developing next‑generation satellite constellations for communications, Earth observation, and scientific research missions, all requiring radiation‑resistant germanium‑based solar arrays. International satellite constellation projects represent enormous demand potential, with the G60 Constellation project planning to launch over 15,000 satellites by 2030, each requiring approximately 6,000 to 15,000 germanium wafers. Australian companies are positioning themselves to supply components for both domestic space programs and international partnerships, while research collaborations with NASA and the European Space Agency are advancing germanium solar cell technologies with improved performance characteristics and reduced manufacturing costs.

Increasing Adoption of Infrared Optics in Defense and Autonomous Vehicle Systems

Increasing adoption of infrared optics in defense and autonomous vehicle systems is further expanding the Australia germanium market share. Germanium's superior performance for thermal imaging and sensing systems makes it essential for defense modernization programs, where germanium‑based infrared optics are critical for night vision equipment, surveillance systems, and missile guidance technology. Australia's defense modernization programs are expected to drive consumption of germanium‑based infrared optics and radiation‑resistant substrates throughout the forecast period. The autonomous vehicle industry's reliance on germanium optics for LiDAR and thermal imaging systems, essential for all‑weather navigation and obstacle detection, is also creating growing demand channels for germanium materials across Australia's automotive technology sector.

Australia Germanium Market Segmentation

Segmentation analysis provides a detailed view of the Australia germanium market by category:

- Type Insights: Germanium Ingot, Germanium Tetrachloride, High Purity GeO₂, Others.

- Application Insights: PET, Electronics and Solar, Fiber Optics, IR Optics, Others.

- Regional Insights: Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia.

Competitive Landscape

The competitive landscape of the Australia germanium market is characterized by complete import dependence, with no current domestic primary production or refining operations. The competitive environment is dominated by international suppliers, primarily from China, Belgium, and other established germanium‑producing regions that serve Australian customers through distribution networks and direct supply agreements. Australian companies operating in downstream sectors such as telecommunications infrastructure, semiconductor device manufacturing, and defense systems source germanium materials through specialized chemical distributors and materials trading companies that maintain local inventory and provide technical support. The market environment is evolving as government initiatives encourage domestic processing capability development, creating potential opportunities for mining companies with zinc operations to vertically integrate into germanium recovery. Research institutions including CSIRO and Geoscience Australia are actively working with industry partners to de‑risk investment decisions through techno‑economic feasibility studies and pilot‑scale demonstration projects that could attract capital for commercial‑scale extraction facilities over the coming years.

Regional Analysis

Regional dynamics within the Australia germanium market are shaped by varying levels of mining activity, research institution presence, and downstream industrial concentration.

- Western Australia emerges as a critical demand center for germanium resource potential, driven by the region's significant zinc mining operations that provide abundant source materials for potential germanium extraction as a by‑product. The region's mining infrastructure and expertise create favourable conditions for domestic processing capability development.

- Queensland represents another key region for germanium resource potential, with substantial zinc deposits and bauxite refining operations offering opportunities for by‑product recovery. The region's established mining industry and government support for critical minerals development position it as a potential hub for future germanium extraction facilities.

- New South Wales and the Australian Capital Territory benefit from the presence of major research institutions including Geoscience Australia, CSIRO, and ANSTO, which are conducting detailed studies on germanium extraction methodologies and techno‑economic assessments. These research activities are establishing the technical foundations for future domestic production capabilities.

- Victoria and Tasmania, along with the Northern Territory and Southern Australia, though smaller in mining activity, contribute to the broader research ecosystem and may see emerging opportunities as domestic processing capability develops.

Recent Industry Developments

- October 2024: Geoscience Australia announced a major research initiative to develop methodologies for quantifying Australia's resource potential for germanium and indium in Australian zinc deposits. The project involves collaboration with ANSTO, which is undertaking desktop studies and test work on the technical recovery of germanium from zinc ores, and CSIRO, which is assessing the techno‑economic opportunities for Australia to produce germanium and gallium from existing mining operations.

- November 2024: Scientists from the Commonwealth Scientific and Industrial Research Organisation (CSIRO) announced that Australia is exploring the possibility of extracting germanium and gallium as byproducts of mining operations. CSIRO's principal investigator for green mineral technologies stated that Australia could help reduce supply chain pressures due to the country's high mining rates of bauxite and zinc, the primary source minerals for germanium production.

- December 2024: The Australian Government continued to prioritise critical mineral development, with germanium remaining on Australia's Critical Minerals List, reinforcing its strategic importance for technological sovereignty and national security.

- 2025 (Throughout): The Australian telecommunications sector continued substantial investments in fiber optic infrastructure to support nationwide 5G network deployments, creating sustained demand for high‑purity germanium dioxide across metropolitan and regional areas.

- 2025 (Throughout): Australian space startups and research institutions advanced next‑generation satellite constellation development, increasing demand for germanium substrates in multi‑junction solar cells for space applications.

Browse Full Report with TOC & List of Figures for In‑Depth Market Insights: https://www.imarcgroup.com/australia-germanium-market

Note: If you need any specific information that is not covered currently within the scope of the report, we will provide the same as a part of customization.

About Us

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us

IMARC Group

134 N 4th St., Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No.: (D) +91 120 433 0800

United States: +1-201-971-6302

What's Your Reaction?