Australia Bioreactors Market: Size, Share, Trends, Analysis, Growth & Forecast to 2026-2034

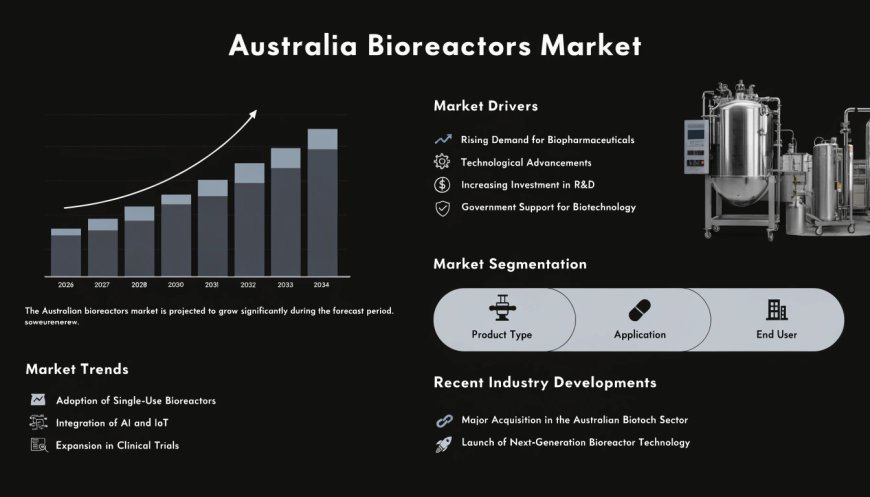

The Australia bioreactors market size reached USD 175.93 Million in 2025. The market is projected to reach USD 413.31 Million by 2034, growing at a CAGR of 9.96% during 2026-2034

Market Overview

The Australia bioreactors market is positioned for robust growth, driven by the rapid adoption of single-use systems, significant government investment in sovereign biopharmaceutical manufacturing capabilities, and the expansion of cell and gene therapy production infrastructure across the country. According to IMARC Group, the market size reached USD 175.93 Million in 2025 and is projected to reach USD 413.31 Million by 2034, exhibiting a compound annual growth rate (CAGR) of 9.96% during 2026‑2034.

The Australian Government's historic, multi‑year commitment to building domestic manufacturing capacity represents the most powerful growth driver for the market. Through policy initiatives such as the Medical Research Future Fund, the Biomedical Translation Fund, and the National Reconstruction Fund, substantial funding is being directed toward industrial infrastructure, clinical trial capabilities, and commercialisation pathways for novel medications. These initiatives directly address the supply chain vulnerabilities exposed during the COVID‑19 pandemic and the dangers associated with over‑reliance on overseas manufacturing. This market is strategically important to Australia's economy as it underpins the nation's ambition to become a regional biomanufacturing hub, reduces dependence on imported biologics and vaccines, and creates high‑value employment in the life sciences sector.

The Australia bioreactors market is poised for sustained expansion, driven by a projected CAGR of 9.96% through 2034, unprecedented government investment in sovereign manufacturing, and the explosive adoption of single‑use bioreactor systems. With the Medical Research Future Fund allocating AUD 35.7 million for clinical trial and industrial infrastructure, and single‑use systems capturing approximately 80 percent of the stirred tank bioreactor segment, the market presents significant opportunities for manufacturers, technology partners, and investors focused on flexible, scalable, and contamination‑free bioprocessing solutions.

Australia Bioreactors Market Summary

The Australia bioreactors market encompasses a range of cultivation systems used for the production of biologics, vaccines, cell and gene therapies, and precision fermentation products. The ecosystem includes bioreactor manufacturers, contract development and manufacturing organisations (CDMOs), biopharmaceutical companies, research institutions, and government agencies.

Segmentation Insights:

-

By Type: Single‑use and multi‑use bioreactor systems. Single‑use bioreactors are experiencing rapid adoption due to their operational and economic advantages.

-

By Usage: Lab‑scale production, pilot‑scale production, and full‑scale production.

-

By Region: Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia.

The market is driven by the growing adoption of single‑use bioreactor systems for enhanced operational efficiency, government investment in biopharmaceutical manufacturing infrastructure and sovereign capability building, and the expansion of cell and gene therapy manufacturing capabilities driving specialised bioreactor demand.

Porter's Five Forces Analysis – Australia Bioreactors Market

The competitive dynamics of the Australia bioreactors market can be analysed using Porter's Five Forces framework.

Bargaining Power of Suppliers – Moderate

The market relies on a mix of international bioreactor manufacturers and specialised component suppliers. Global leaders such as Thermo Fisher Scientific, Sartorius, and Merck hold influence due to their advanced technology platforms and established distribution networks. However, the growing domestic biomanufacturing sector and the presence of multiple international suppliers provide Australian buyers with alternative sourcing options, balancing supplier power.

Bargaining Power of Buyers – Moderate

Buyers include biopharmaceutical companies, CDMOs, research institutions, and government agencies. The Australian Government's substantial investment in sovereign manufacturing capability gives institutional buyers significant negotiating leverage. However, the specialised nature of bioreactor systems and the need for validated, GMP‑compliant equipment provides established suppliers with some protection against pure price‑based competition.

Threat of New Entrants – Moderate

Capital requirements for developing bioreactor manufacturing capabilities are substantial, and achieving GMP certification and TGA compliance creates barriers. However, the growing market and government support for local manufacturing are attracting new entrants focused on innovative single‑use and automated bioreactor technologies. Niche opportunities exist for manufacturers specialising in cell therapy and precision fermentation applications.

Threat of Substitutes – Low

There is a low threat of substitutes. While alternative bioprocessing methods exist, bioreactors remain essential for large‑scale production of biologics, vaccines, and cell therapies. The unique combination of scalability, process control, and contamination prevention makes bioreactors indispensable for modern biopharmaceutical manufacturing.

Competitive Rivalry – Moderate

The market is moderately competitive, featuring a mix of global bioreactor manufacturers and specialised suppliers serving the Australian market. Key players compete on product innovation, automation capabilities, scalability, and the ability to provide integrated bioprocessing solutions. The market is also seeing increased collaboration between bioreactor manufacturers, CDMOs, and research institutions to develop advanced cultivation systems for emerging therapeutic modalities.

Request for Sample Report: https://www.imarcgroup.com/australia-bioreactors-market/requestsample

Market Growth Drivers

Growing Adoption of Single‑Use Bioreactor Systems for Enhanced Operational Efficiency

Single‑use bioreactor systems are experiencing rapid adoption across Australia's biopharmaceutical manufacturing sector due to their compelling operational and economic advantages. By eliminating the need for lengthy cleaning and sterilising processes between manufacturing batches, these disposable solutions dramatically shorten turnaround times and reduce the risk of cross‑contamination. The capital investment requirements for single‑use systems are approximately 40 percent lower compared to traditional stainless‑steel bioreactors, making them particularly attractive for contract manufacturing organisations and emerging biotechnology companies with limited infrastructure budgets.

Energy and water consumption are reduced by 45‑50 percent, aligning with sustainability objectives while delivering measurable cost savings. Single‑use bioreactors captured approximately 80 percent of the stirred tank bioreactor segment in 2024, driven by their advantages in reducing contamination risks, lowering capital investment, and decreasing resource consumption. These systems are particularly favoured by CDMOs due to operational flexibility and reduced turnaround times between batches, enabling rapid switching between different cell lines and production processes.

Government Investment in Sovereign Biopharmaceutical Manufacturing Capability

The most powerful growth driver is the Australian Government's historic, multi‑year commitment to building domestic manufacturing capacity. Through policy initiatives such as the Medical Research Future Fund, the Biomedical Translation Fund, and the National Reconstruction Fund, substantial funding is being directed toward industrial infrastructure, clinical trial capabilities, and commercialisation pathways for novel medications. In January 2025, the Medical Research Future Fund allocated AUD 35.7 million specifically to improve clinical trial and industrial infrastructure nationwide, targeting early‑stage development capacity and aiming to attract global pharmaceutical interest while supporting the growth of Australia's CDMO capabilities.

State governments are complementing federal initiatives with targeted programs supporting regional biomanufacturing hubs, skills development, and technology adoption, creating an enabling environment for bioreactor manufacturers and end‑users. The coordinated approach across government levels is stimulating demand for advanced cultivation systems capable of supporting diverse therapeutic modalities including monoclonal antibodies, vaccines, cell therapies, and gene therapies.

Expansion of Cell and Gene Therapy Manufacturing Capabilities

The rapid growth of cell and gene therapy (CGT) manufacturing capabilities in Australia is driving specialised bioreactor demand. The CGT and vaccine segments are almost exclusively served by single‑use bioreactors due to their flexibility and reduced cross‑contamination risk. As the nation works to close its first‑of‑a‑kind manufacturing gap, bioreactors have become the physical heart of Australia's ambition to become a regional biomanufacturing hub.

Market Growth Drivers

Integration of Artificial Intelligence and Automation Technologies

Advancements in automation and artificial intelligence integration are enhancing process efficiency and attracting international partnerships. Through predictive modelling, real‑time process optimisation, and digital twin simulations that allow exact control of crucial factors like temperature, pH, oxygen levels, and nutrient distribution, AI and machine learning are revolutionising bioprocess development. Manufacturers may use sophisticated process control techniques, lower batch variability, reduce contamination concerns, and expedite the transition from laboratory to commercial production with AI‑driven solutions. Leading biopharmaceutical companies are deploying AI platforms for continuous monitoring of mammalian cell culture bioreactors to boost yields and enhance operational efficiency across global manufacturing sites.

Rising Demand for Biologics, Biosimilars, and Precision Fermentation

The accelerating adoption of single‑use technologies by CDMOs, combined with rising demand for biologics and biosimilars, will create sustained momentum. The expansion of precision fermentation initiatives is further driving demand for specialised bioreactor systems. Precision fermentation products are set to transform Australia's agricultural and industrial base, creating new applications for bioreactor technology beyond traditional pharmaceutical manufacturing.

Strategic Bifurcation in Demand Across Segments

The market is defined by a strategic bifurcation in demand: large‑scale commercial biomanufacturing for established modalities leans toward stainless steel or hybrid systems for long‑term cost control, while the rapidly growing cell and gene therapy and vaccine segments are almost exclusively served by single‑use bioreactors due to their flexibility and reduced cross‑contamination risk. This dual‑track demand creates opportunities for suppliers across both segments, with each addressing distinct customer requirements and production scales.

Australia Bioreactors Market Segmentation

Segmentation analysis provides a detailed view of the Australia bioreactors market by category:

-

Usage Insights: Lab‑scale Production, Pilot‑scale Production, Full‑scale Production

-

Regional Insights: Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia

Competitive Landscape

The competitive landscape of the Australia bioreactors market features a mix of global bioreactor manufacturers and specialised suppliers serving the Australian biopharmaceutical sector. Key players drive the market by expanding product portfolios, investing in single‑use and automation technologies, and strengthening partnerships with CDMOs and research institutions. Their investments in innovation, regulatory compliance, and process optimisation are accelerating biopharmaceutical manufacturing capability and ensuring consistent bioreactor availability across diverse therapeutic applications.

The market is also benefiting from strategic collaborations between bioreactor manufacturers, CDMOs, and research institutions to develop advanced cultivation systems capable of supporting diverse therapeutic modalities. The market research report has provided a comprehensive analysis of the competitive landscape, including market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant. Detailed profiles of all major companies have also been provided.

Regional Analysis

Regional dynamics within the Australia bioreactors market are shaped by the concentration of biopharmaceutical manufacturing facilities, research institutions, and government investment across states and territories.

-

Victoria & Tasmania is a leading region, driven by Melbourne's strong biotech ecosystem, concentration of CDMOs, and significant government investment in biopharmaceutical infrastructure. The state benefits from the presence of major research institutions and a skilled life sciences workforce.

-

Australia Capital Territory & New South Wales represents a significant market, with Sydney's growing biotech sector, research institutions, and government agencies supporting biopharmaceutical innovation.

-

Queensland is an emerging market, supported by the state's commitment to biomanufacturing and the presence of key research institutions and CDMOs.

-

Western Australia sees steady demand, with Perth's growing life sciences sector and research institutions driving adoption of bioreactor systems.

-

Northern Territory & Southern Australia, while smaller in market size, are experiencing growth driven by increasing research activity and government initiatives to expand regional biomanufacturing capabilities.

Recent Industry Developments

-

January 2025: The Medical Research Future Fund allocated AUD 35.7 million specifically to improve clinical trial and industrial infrastructure nationwide, targeting early‑stage development capacity and aiming to attract global pharmaceutical interest while supporting the growth of Australia's CDMO capabilities.

-

2024: Single‑use bioreactors captured approximately 80 percent of the stirred tank bioreactor segment, driven by their advantages in reducing contamination risks, lowering capital investment, and decreasing resource consumption.

-

2025‑2026 (Throughout): The Australia bioreactors market continued its robust growth trajectory, supported by the expansion of cell and gene therapy manufacturing capabilities, increasing government investment in sovereign biopharmaceutical manufacturing, and the accelerating adoption of single‑use technologies by CDMOs.

-

2025‑2026 (Throughout): Leading biopharmaceutical companies deployed AI platforms for continuous monitoring of mammalian cell culture bioreactors to boost yields and enhance operational efficiency across global manufacturing sites.

Browse Full Report with TOC & List of Figures for In‑Depth Market Insights: https://www.imarcgroup.com/australia-bioreactors-market

Note: If you need any specific information that is not covered currently within the scope of the report, we will provide the same as a part of customisation.

About Us

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us

IMARC Group

134 N 4th St., Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No.: (D) +91 120 433 0800

United States: +1-201-971-6302

What's Your Reaction?