Australia Aluminum Alloys Market 2026-2034 | Trends, Growth and Forecast - IMARC Group

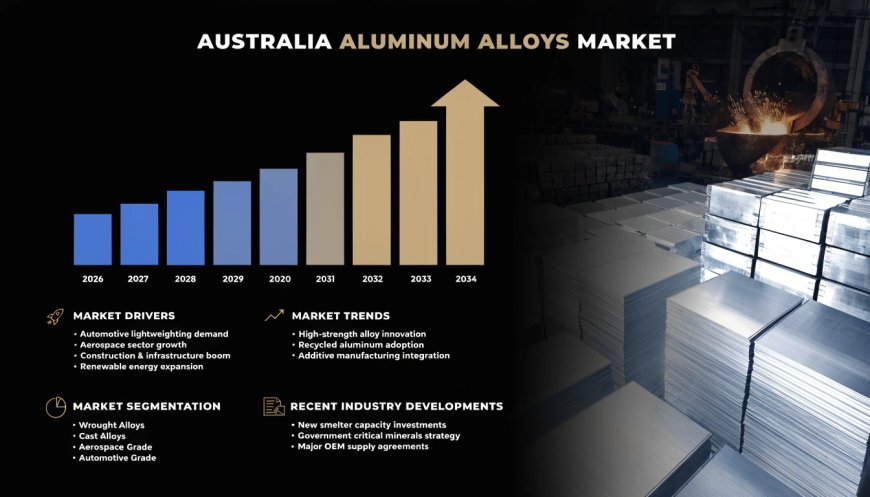

The Australia aluminum alloys market size reached USD 4.3 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 8.5 Billion by 2034, exhibiting a growth rate (CAGR) of 7.72% during 2026-2034.

Market Overview

The Australia aluminum alloys market is advancing at a steady pace, fuelled by surging demand across the automotive, aerospace, and construction industries, together with a definitive move towards lightweight materials and environmentally sustainable manufacturing. According to IMARC Group, the market size reached USD 4.3 Billion in 2025 and is projected to reach USD 8.5 Billion by 2034, exhibiting a robust compound annual growth rate (CAGR) of 7.72% during 2026‑2034. The sector's expansion is strengthened by a considerable increase in aluminum exports, with shipments to the US surging by 103%, and a landmark AUD 2 Billion government initiative to transition domestic smelters to renewable energy, securing up to 75,000 jobs. The Australia aluminum alloys market remains strategically vital to the country’s economy, supporting thousands of jobs, underpinning key export industries, and aligning with national ambitions to become a leader in sustainable, low‑carbon metal production.

The Australia aluminum alloys market is poised for sustained expansion, driven by a projected CAGR of 7.72% through 2034, the surge in export demand, and the strategic government‑led shift to renewable energy. With the world’s sixth‑largest aluminum producer status, the market presents significant opportunities for producers, fabricators, and technology partners focused on sustainable, high‑performance alloy solutions for automotive lightweighting, aerospace innovations, and green building practices.

Australia Aluminum Alloys Market Summary

The Australia aluminum alloys market encompasses a comprehensive range of products, including rolled, extruded, and cast forms, essential for applications requiring lightweight strength, corrosion resistance, and infinite recyclability. The ecosystem includes global mining and smelting giants, such as Rio Tinto and Alcoa, alongside downstream fabricators and extruders like Capral Aluminium, serving end‑users across the automotive and transportation, construction, packaging, electrical, consumer durables, and machinery and equipment sectors.

- Application Insights: The market is segmented by application into: Automotive and Transportation, Construction, Packaging, Electrical, Consumer Durables, Machinery and Equipment, and Others.

- Regional Insights: Geographically, the market covers: Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia.

- The market is driven by a strong appetite for lightweight materials to improve fuel efficiency and reduce emissions, along with massive government investment in renewable energy for smelters and growing global demand for sustainable aluminum.

PORTER’S FIVE FORCES ANALYSIS – AUSTRALIA ALUMINUM ALLOYS MARKET

The competitive dynamics of the Australia aluminum alloys market can be analyzed using Porter’s Five Forces framework.

Bargaining Power of Suppliers – Moderate

The market relies on a concentrated group of global mining and energy companies for raw materials, particularly bauxite and electricity. Australia has abundant bauxite reserves, but the bargaining power of suppliers is significantly influenced by energy costs. The transition to renewable energy, supported by the AUD 2 Billion government plan, is helping stabilize power costs and reduce supplier leverage over smelters.

Bargaining Power of Buyers – Moderate

Buyers in the Australia aluminum alloys market include large‑scale manufacturers in the automotive, aerospace, and construction industries. While these buyers often negotiate long‑term contracts for high‑volume purchases, the specialized properties required for specific alloys (e.g., high‑strength grades for aerospace) can create switching costs. The rise of sustainable aluminum as a premium product is providing producers with enhanced pricing power for certified low‑carbon aluminum.

Threat of New Entrants – Moderate

Establishing a new primary aluminum smelting facility requires immense capital investment and access to stable, affordable energy. However, the government’s focus on developing a green aluminum industry is creating openings for partnerships and specialized entrants, particularly in the recycling and downstream processing sectors.

Threat of Substitutes – Low

While materials like high‑strength steel, carbon fiber composites, and magnesium compete in some applications, aluminum offers a unique combination of light weight, high strength‑to‑weight ratio, corrosion resistance, and infinite recyclability. In key end‑use sectors like packaging (beverage cans) and transportation (automotive bodies), no other material can match aluminum’s performance and cost‑effectiveness.

Competitive Rivalry – Moderate

The market features a mix of global vertically integrated mining and smelting companies, such as Rio Tinto and Alcoa, alongside specialized downstream processors like Capral Aluminium. The recent surge in global aluminum prices has led major smelters to restart idle capacity, intensifying competition for production output and export market share. Competition is centered on energy efficiency, sustainability credentials, and the ability to supply advanced alloy specifications for emerging applications like electric vehicles and renewable energy infrastructure.

Request for Sample Report: https://www.imarcgroup.com/australia-aluminum-alloys-market/requestsample

MARKET GROWTH DRIVERS

Strategic Shift to Renewable Energy and Green Aluminum Production

A primary factor propelling the Australia aluminum alloys market is the landmark AUD 2 Billion government plan to transition the nation’s smelters from coal‑fired power to renewable energy. This initiative is designed to secure up to 75,000 jobs while strengthening Australia’s position as a major global aluminum producer. The shift to green energy is promoting environmental aims while increasing the industry's resilience and competitiveness. As the world’s sixth‑largest aluminum producer, this forward‑thinking strategy puts the country in a strong position to meet rising global demand for cleaner, more sustainable manufacturing practices, driving long‑term growth in the domestic market.

Expanding Demand for Lightweighting in Automotive and Aerospace Sectors

The global push for lightweight materials is directly benefiting the Australia aluminum alloys market. Rising demand for improved fuel efficiency, reduced emissions, and enhanced electric vehicle range is boosting aluminum consumption. Automotive manufacturers are increasingly using aluminum alloys for body panels, structural components, and battery enclosures to meet stringent fuel efficiency and emissions standards. Similarly, the aerospace sector is adopting high‑strength aluminum alloys for aircraft manufacturing to enhance fuel efficiency and reduce emissions, driven by increasing investments in defense modernization and commercial aviation.

Infrastructure Development and Construction Megaprojects

The construction sector is a major consumer of aluminum alloys, driven by ongoing infrastructure development and large‑scale megaprojects. The lightweight, corrosion‑resistant, and design‑flexible properties of aluminum make it ideal for a wide range of architectural applications, from window frames and curtain walls to structural components. The use of domestically produced, low‑carbon aluminum is gaining significant traction, and the impending Brisbane 2032 Olympic and Paralympic Games is unlocking extensive opportunities across construction, transport, and energy sectors, all of which will rely heavily on aluminum materials and systems.

Australia Aluminum Alloys Market Segmentation

Segmentation analysis provides a detailed view of the Australia aluminum alloys market by category:

- Application Insights: Automotive and Transportation, Construction, Packaging, Electrical, Consumer Durables, Machinery and Equipment, Others.

- Regional Insights: Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia.

Competitive Landscape

The competitive landscape of the Australia aluminum alloys market is shaped by a mix of global vertically integrated mining and smelting giants and specialized downstream manufacturers. Key players drive the market by expanding production capacities, investing in renewable energy transitions, and strengthening export partnerships. Their investments in advanced alloy technologies, energy efficiency, and sustainability are boosting awareness, accelerating the adoption of green aluminum, and ensuring reliable alloy availability across diverse industrial and consumer segments. Key companies operating in the market include Rio Tinto, Alcoa, Capral Aluminium, and South32. Rio Tinto and Alcoa are at the centre of a major upswing, moving to bring production back online and reassess expansion options in the wake of a surge in global aluminum prices. As part of a major government support package, Rio Tinto will invest in energy and transmission assets at the Boyne smelter in Queensland. Capral Aluminium, a leading local extruder, is positioned to supply materials for the Brisbane 2032 Olympic and Paralympic Games. The market is also seeing new entrants, such as Alpha HPA, which secured a $75 million investment from the National Reconstruction Fund Corporation to build a manufacturing facility for ultra‑high purity aluminum materials in Gladstone, Queensland.

Regional Analysis

Regional dynamics within the Australia aluminum alloys market are shaped by the location of major smelters, downstream manufacturing hubs, and high‑profile infrastructure projects.

- Australia Capital Territory & New South Wales is a large market, driven by Sydney's significant construction activity and the landmark Western Sydney International Airport project, which is a major consumer of locally extruded low‑carbon aluminum.

- Queensland is emerging as a powerhouse for the industry, home to the Boyne aluminum smelter, which is at the center of a $2 billion federal‑state government deal to transition to renewable energy, securing thousands of jobs. The state is also a major hub for bauxite mining.

- Victoria & Tasmania is significant due to the presence of the Portland aluminum smelter. Alcoa has resumed production from previously idle potlines at the Portland smelter to capitalize on a surge in global aluminum prices.

- Western Australia is a key region for raw material extraction and power generation, home to significant bauxite mining operations and an area where major producers like Alcoa are focused on expanding capacity.

Recent Industry Developments

- March 2026: The federal and Queensland state governments struck a $2 billion deal with Rio Tinto to help transition the Boyne aluminum smelter to renewable energy, securing the operational future and thousands of jobs at the plant through at least 2040.

- May 2026: Major producers Rio Tinto and Alcoa moved to restart idle production capacity at smelters in Queensland and Victoria, respectively, to capitalize on a sharp price increase in global aluminum markets.

- January 2026: Alpha HPA secured a $75 million investment from the National Reconstruction Fund Corporation to support its HPA First Project in Gladstone, Queensland, which is expected to become the world’s largest single manufacturing facility for ultra‑high purity aluminum materials.

- 2025 (Throughout): Australia’s aluminum exports to the US surged 103%, with the Australian government unveiling its AUD 2 Billion plan to help smelters transition to renewable energy, reinforcing Australia's position as the world’s sixth‑largest aluminum producer.

- 2024-2025 (Throughout): Capral Aluminium supplied its largest order of custom‑designed low‑carbon aluminum for the Western Sydney International Airport terminal, highlighting the growing domestic demand for sustainable, Australian‑made aluminum products.

Browse Full Report with TOC & List of Figures for In‑Depth Market Insights: https://www.imarcgroup.com/australia-aluminum-alloys-market

Note: If you need any specific information that is not covered currently within the scope of the report, we will provide the same as a part of customisation.

About Us

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us

IMARC Group

134 N 4th St., Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No.: (D) +91 120 433 0800

United States: +1-201-971-6302

What's Your Reaction?