India Diesel Generator Market 2026-2034: Overall Valuation Reaching USD 2.15 Billion With 5.25% CAGR

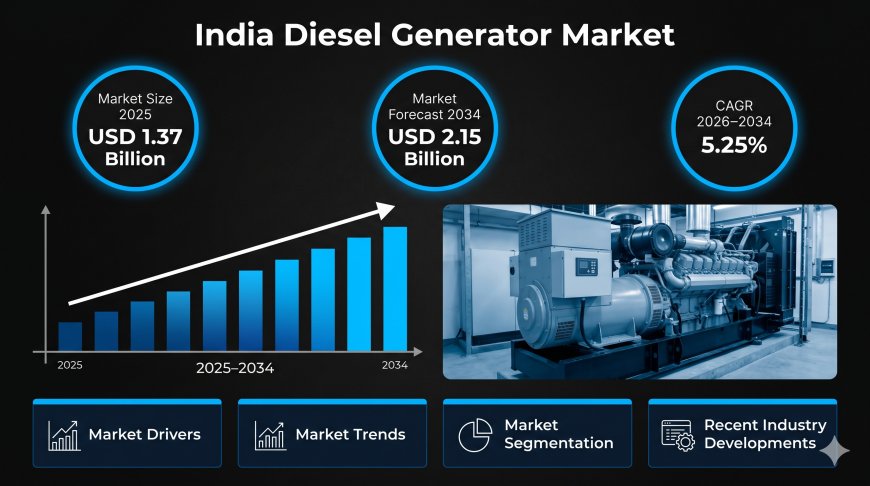

The India diesel generator market size was valued at USD 1.37 Billion in 2025, and is projected to reach USD 2.15 Billion by 2034, growing at a CAGR of 5.25% during 2026-2034.

According to IMARC Group’s report titled “India Diesel Generator Market Size, Share, Trends and Forecast by Capacity, Application, Mobility, End User, and Region, 2026-2034“, The report offers a comprehensive analysis of the industry, including India diesel generator market forecast, growth and regional insights.

The India diesel generator market size was valued at USD 1.37 Billion in 2025, and is projected to reach USD 2.15 Billion by 2034, growing at a CAGR of 5.25% during 2026-2034.

The India diesel generator market is fundamentally realigning to support the nation’s accelerated industrialization and the critical uptime requirements of a burgeoning digital economy. As the manufacturing sector targets a contribution to GDP by 2034, the demand for resilient, high-capacity power backup solutions has become a structural necessity for institutional stakeholders.

- Segment Leadership: The medium and high-kVA segments (above 750 kVA) are capturing significant volume, particularly within the data center and heavy industrial sectors.

- Infrastructure Catalyst: Under the National Infrastructure Pipeline (NIP), projects worth USD 1.4 trillion are currently under execution, directly scaling the requirement for on-site power generation.

- Data Center Expansion: India's data center capacity is exceed 1.3 GW by 2025, necessitating a high-velocity deployment of Tier-IV compliant backup power grids.

The Strategic Market Challenge: Navigating the Diesel Generator Market in India

The critical structural challenge within the Energy & Mining sector is the capital-intensive transition to the CPCB IV+ emission norms, which mandate a 90% reduction in particulate matter and nitrogen oxides. Leaders often overlook the operational complexity of integrating advanced after-treatment systems into legacy power architectures. This transition significantly inflates the initial capital expenditure and alters the total cost of ownership (TCO), requiring a sophisticated recalibration of procurement strategies to balance environmental compliance with bottom-line profitability.

➤ Access Key Market Statistics and Actionable Insights - Request Sample Report: https://www.imarcgroup.com/india-diesel-generator-market/requestsample

India's Strategic Vision for the Diesel Generator Market

- Atmanirbhar Bharat in Power Systems: The strategic vision focuses on achieving 100% domestic value addition in high-speed engine manufacturing to reduce reliance on imported components and optimize the supply chain.

- Hybridization and Grid Stability: According to the Ministry of Power, the long-term goal involves the seamless integration of diesel generators with renewable energy microgrids, utilizing DG sets as the primary balancing mechanism for intermittent solar and wind power.

- Smart Energy Management: Government policy shifts are prioritizing the deployment of IoT-integrated power units to facilitate real-time monitoring of fuel efficiency and emission levels, aligning with the National Clean Air Programme (NCAP).

Why Invest in the India Diesel Generator Market: Key Growth Drivers & ROI

- Data Center and IT-BPM Proliferation: With the expansion of 5G and hyper-scale data centers, the demand for "zero-downtime" power is non-discretionary. Investors achieve superior ROI by targeting the high-kVA segment, which offers higher margins and long-term maintenance contracts driven by essential service-level agreements (SLAs).

- Real Estate and Commercial Revitalization: The resurgence of Grade-A office spaces and the construction of over 100 smart cities provide a steady volume play. According to Invest India, the construction sector's expansion ensures a consistent demand for medium-capacity DG sets, offering a resilient hedge against cyclical industrial fluctuations.

- Technological Shift to CPCB IV+ Compliance: The mandatory shift to cleaner emission standards acts as a catalyst for replacement demand. Stakeholders can capitalize on the massive upgrade cycle of the existing national fleet, where organizations are replacing legacy assets with high-efficiency, compliant units to avoid regulatory penalties.

India Diesel Generator Market Market Trends & Future Outlook

- Adoption of Dual-Fuel Systems: A definitive shift toward systems that utilize a mix of diesel and natural gas is occurring to optimize fuel costs and reduce carbon footprints in industrial corridors.

- Growth in Rental Power Markets: Small and medium enterprises (SMEs) are increasingly pivoting toward Power-as-a-Service (PaaS) models, reducing upfront CAPEX while maintaining operational agility.

- Digital Remote Monitoring: The integration of AI-driven predictive maintenance and cloud-based telematics is becoming standard for high-capacity units to prevent unplanned outages and optimize fuel consumption.

- Focus on Noise Reduction: Urban development norms are driving R&D into acoustic enclosures and low-decibel engine designs, making DG sets more compatible with residential and hospital zones.

- Expansion in Tier-2 and Tier-3 Cities: The decentralization of the IT sector is triggering fresh demand for standby power in emerging urban hubs across the country.

Regulatory Landscape & Policy Catalysts in India

- CPCB IV+ Emission Standards: According to the Central Pollution Control Board, these stringent norms came into full effect in 2024, legally requiring all new DG sets to meet the world’s most rigorous particulate and NOx standards.

- GRAP (Graded Response Action Plan) Implementation: In regions like the NCR, the Commission for Air Quality Management (CAQM) restricts the use of non-compliant DG sets during peak pollution months, forcing a structural shift toward clean-fuel or retrofitted systems.

- Production Linked Incentive (PLI) Scheme: While primarily focused on heavy components, the scheme indirectly benefits the sector by incentivizing the domestic assembly of electronic controllers and fuel injection systems.

- Energy Conservation Building Code (ECBC): As mandated by the Bureau of Energy Efficiency (BEE), new commercial developments must integrate high-efficiency backup systems to comply with national energy rating standards.

- Duty Drawback and Export Incentives: According to the Ministry of Commerce, the government provides duty-neutralization schemes to boost the export of domestically manufactured DG sets to Southeast Asian and African markets.

➤ Explore the Exact Chapters and Data Scope - Get Full Brochure: https://www.imarcgroup.com/request?type=report&id=29681&flag=A

By the IMARC Group, the Top Competitive Landscape & their Positioning:

- Cummins India Ltd.

- Kirloskar Oil Engines Limited

- Mahindra Powerol Ltd.

India Diesel Generator Market Segmentation:

The market report offers a comprehensive analysis of the segments, highlighting those with the largest India diesel generator market share. It includes forecasts for the period 2026-2034 and historical data from 2020-2025 for the following segments.

Capacity Insights

- 100–350 kVA (37.0%)

- 0–100 kVA

- 350–1000 kVA

- Above 1000 kVA

Application Insights

- Standby Backup Power (70.0%)

- Prime Power

- Peak Shaving Power

Mobility Insights

- Stationary (71.0%)

- Portable

End User Insights

- Industrial (42.0%)

- Residential

- Commercial

Regional Insights

- West India (31.0%)

- North India

- South India

- East India

Note: If you need specific information that is not currently within the scope of the report, we can provide it to you as a part of the customization.

➤ Shape the Data to Answer Your Specific Questions - Request Customization: https://www.imarcgroup.com/request?type=report&id=29681&flag=E

Frequently Asked Questions (FAQs)

Q1: What is the current value and projected growth of the India Diesel Generator Market?

According to IMARC Group, the India diesel generator market reached a significant valuationUSD 1.37 Billion in 2025, and is projected to reach USD 2.15 Billion by 2034, growing at a CAGR of 5.25% during 2026-2034.

Q2: Which kVA range is currently witnessing the highest demand in India?

The medium-kVA (75 kVA to 375 kVA) range leads in terms of volume, while the high-kVA (above 750 kVA) range is the fastest-growing in terms of value due to data center demand.

Q3: How is the rise of renewable energy impacting the diesel generator market?

Renewable integration is driving the demand for hybrid DG sets, which serve as a critical backup during periods of low solar or wind generation, ensuring overall grid stability.

Q4: What are the primary end-user segments driving market volume?

The industrial manufacturing, commercial real estate, and healthcare sectors remain the primary users, with the IT and telecom segment providing the highest growth velocity.

Q5: What impact do the CPCB IV+ norms have on the cost of generators?

The adoption of CPCB IV+ technology typically results in an initial price increase of 20% to 30% due to the addition of SCR (Selective Catalytic Reduction) and DPF (Diesel Particulate Filter) systems.

Strategic Insight & Verdict:

The India diesel generator market is no longer a commodity-driven segment; it has evolved into a high-tech utility essential for the nation's 5G and industrial ambitions. we at IMARC Group have observed that that the winners in this sector will be those who master the transition to CPCB IV+ compliant, smart-integrated systems. For investors, the strategic path lies in high-capacity units and hybrid solutions that cater to the "zero-downtime" requirements of the digital infrastructure boom.

Gaurav, Digital Market Research Strategist at IMARC Group: https://www.linkedin.com/in/gourav-shah-005425345

Verified Data Source: IMARC Group

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1-202071-6302

What's Your Reaction?