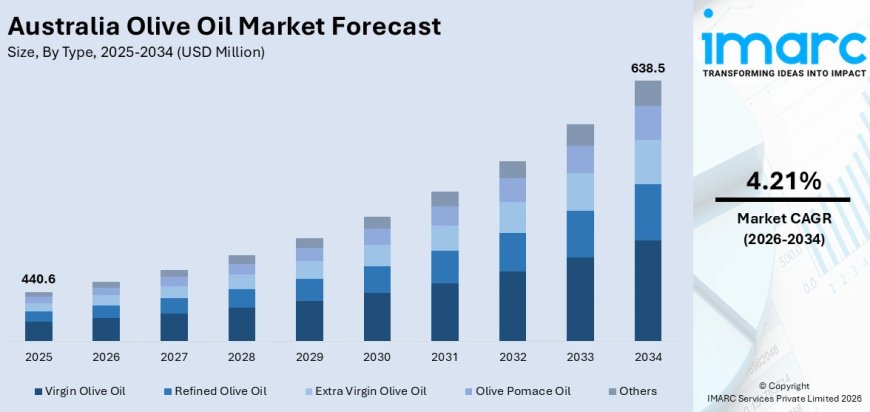

Australia Olive Oil Market Size, Share, Report 2026-2034

Australia olive oil market size reached USD 440.6 Million in 2025. Looking forward, the market is expected to reach USD 638.5 Million by 2034, exhibiting a growth rate (CAGR) of 4.21% during 2026-2034.

Australia Olive Oil Market overview

The Australia olive oil market size reached USD 440.6 Million in 2025. Looking forward, the market is expected to reach USD 638.5 Million by 2034, exhibiting a growth rate (CAGR) of 4.21% during 2026-2034. Australia's olive oil sector is experiencing sustained growth, driven by heightening health awareness among consumers, the extensive adoption of Mediterranean diets, growing demand for premium extra virgin olive oil (EVOO) products, and the strengthening domestic production base concentrated across Victoria, South Australia, and New South Wales. The market attained a consumption volume of approximately 60 million litres in 2025, with domestic production supplying roughly one-third of the nation's annual consumption of approximately 50,000 tonnes.

The market is being further propelled by the expansion of Australia's leading producer Cobram Estate Olives, which operates over 2.6 million olive trees across 7,000 hectares of freehold farmland in Victoria and reported a bumper 2024-25 harvest of 14.2 million litres—up from 10.1 million litres the prior year. Group olive oil sales revenue reached AUD 237.4 million with EBITDA surging 75% to AUD 116.6 million, while Australian branded sales grew 16.6% to AUD 141.4 million. Olive oil imports reached 42,272 tonnes in the 2024/25 crop year, representing a 46% increase compared to the previous year, reflecting strong and growing consumer demand that outpaces domestic production capacity.

Request a Business Sample Report for Procurement & Investment Evaluation:

https://www.imarcgroup.com/australia-olive-oil-market/requestsample

Porter's Five Forces Analysis – Australia Olive Oil Market

Bargaining Power of Suppliers – Moderate to High

• Australia's domestic olive oil production supplies approximately one-third of national consumption at around 20,000-21,000 tonnes annually, with the sector heavily concentrated around Cobram Estate Olives—operating 2.6 million trees across 7,000 hectares with two on-site mills processing 144 tonnes of fruit per hour—giving large-scale domestic producers significant supply-side influence.

• International suppliers, predominantly from Spain, Italy, and Greece, supply the remaining two-thirds of Australia's consumption, with imports reaching 42,272 tonnes in 2024/25 (up 46% year-on-year), providing buyers with diverse sourcing options that moderate individual supplier power while global supply volatility and harvest fluctuations can temporarily strengthen supplier leverage.

Bargaining Power of Buyers – Moderate

• Major supermarket chains Woolworths and Coles control a significant share of olive oil retail distribution, leveraging their procurement scale and private-label olive oil ranges to negotiate favorable terms with both domestic producers and importers, while the growing foodservice and hospitality sector provides alternative buyer channels that balance retail dominance.

• Consumer willingness to pay premium prices for certified Australian extra virgin olive oil, single-estate products, and provenance-verified offerings is reducing pure price-based buyer power in the premium segment, rewarding quality-focused producers like Cobram Estate whose branded sales grew 16.6% to AUD 141.4 million.

Threat of New Entrants – Low to Moderate

• Olive grove establishment requires significant upfront capital investment and a 4-7 year maturation period before trees reach commercial production yields, creating meaningful time-to-revenue barriers for new domestic producers, while established players like Cobram Estate benefit from vertically integrated operations spanning grove ownership, harvesting technology, milling, and branded retail distribution.

• Boutique and artisanal olive oil producers can enter the market at smaller scale through regional groves and direct-to-consumer channels including farmers' markets, cellar door sales, and online retail, while import-based brands can enter with lower capital requirements by sourcing from established Mediterranean producers and competing on price in mainstream retail channels.

Threat of Substitutes – Moderate

• Alternative cooking oils including canola, sunflower, avocado, coconut, and macadamia nut oils represent substitutes competing on price, smoke point, and flavor versatility, though olive oil's established position as the premium healthy cooking oil—backed by extensive cardiovascular health research and Mediterranean diet endorsements—provides strong differentiation against price-based substitution.

• The premiumization trend is positively differentiating extra virgin olive oil from commodity cooking oils, with consumers increasingly viewing EVOO as a finishing oil, salad dressing ingredient, and health food rather than a generic cooking fat, while the growing adoption of Mediterranean and plant-based diets reinforces olive oil's unique culinary and nutritional positioning.

Competitive Rivalry – High (Quality-Driven)

• Competition is intense across multiple dimensions: imported Mediterranean brands compete on heritage, authenticity, and price; domestic producers compete on freshness, provenance, and Australian-grown credentials; and private-label supermarket offerings compete on accessibility—with Cobram Estate dominating domestic production and reporting group olive oil sales revenue of AUD 237.4 million and EBITDA growth of 75%.

• Competitive rivalry is constructively driving quality improvements, with Australian producers increasingly investing in advanced milling technology, single-varietal offerings, harvest-date labeling, and international competition entries to differentiate premium EVOO products, while industry bodies promote Australian olive oil quality standards and consumer education to build domestic brand preference.

Australia Olive Oil Market Trends

Premiumization and Extra Virgin Olive Oil Dominance

The most prominent trend shaping Australia's olive oil market is the accelerating premiumization of consumer preferences toward extra virgin olive oil, single-estate products, and provenance-verified offerings. Australian consumers are increasingly choosing EVOO over refined olive oil and blended products, driven by growing understanding of the superior health benefits associated with cold-pressed, antioxidant-rich extra virgin varieties and the expanding influence of Mediterranean diet principles on Australian culinary culture. This premiumization trend is being led by Cobram Estate, whose Australian branded sales grew 16.6% to AUD 141.4 million, reflecting strong consumer demand for premium domestically produced EVOO. Single-varietal olive oils—including Picual, Hojiblanca, Coratina, and Frantoio—are gaining traction among food enthusiasts and home cooks seeking distinctive flavor profiles for specific culinary applications. Harvest-date labeling, cold-press certifications, and international quality competition medals are becoming important purchase decision factors as consumers develop more sophisticated olive oil literacy. The growing foodservice sector is further driving premiumization, with restaurants and cafés featuring high-quality Australian EVOO as a menu differentiator and ingredient highlight.

Domestic Production Expansion and Vertical Integration

The second transformative trend in Australia's olive oil market is the expansion and intensification of domestic production, led by vertically integrated producers investing across the entire value chain from grove establishment through milling, storage, and branded retail distribution. Cobram Estate Olives operates over 2.6 million olive trees across 7,000 hectares of freehold farmland in Victoria, with two on-site olive mills at Boundary Bend and Boort providing combined processing capacity of 144 tonnes of olive fruit per hour and 6.8 million litres of on-site storage. The company's bumper 2024-25 harvest of 14.2 million litres—up 41% from 10.1 million litres the prior year—demonstrates the increasing productivity of Australia's maturing olive groves. Cobram Estate's acquisition of Leda Ag, the manufacturer of olive harvesters, in 2025 further strengthened its vertically integrated model from harvesting technology through to branded retail. Domestic production currently supplies approximately one-third of Australia's annual consumption of 50,000 tonnes, with continued grove maturation, new plantings, and processing capacity investments positioned to gradually increase Australia's self-sufficiency ratio while reducing dependence on imported olive oil.

Australia Olive Oil Market Summary

The Australia olive oil market is defined by premiumization toward extra virgin varieties, expanding domestic production, and growing health-driven consumer demand:

• The market reached USD 440.6 Million in 2025 and is expected to reach USD 638.5 Million by 2034, exhibiting a CAGR of 4.21% during 2026-2034.

• Domestic production supplies approximately one-third of Australia's 50,000-tonne annual consumption, with Cobram Estate Olives operating 2.6 million trees across 7,000 hectares and reporting a bumper 2024-25 harvest of 14.2 million litres (up 41% year-on-year).

• Olive oil imports reached 42,272 tonnes in the 2024/25 crop year, representing a 46% increase compared to the previous year, reflecting strong consumer demand that continues to outpace domestic production capacity.

• Cobram Estate reported group olive oil sales revenue of AUD 237.4 million with EBITDA surging 75% to AUD 116.6 million, while Australian branded sales grew 16.6% to AUD 141.4 million, demonstrating the commercial strength of premium domestic EVOO.

• The market is driven by the growing adoption of Mediterranean diets, heightening health awareness around cardiovascular and anti-inflammatory benefits of EVOO, expanding premium product offerings, and the strengthening vertical integration of Australia's leading domestic producers.

Australia Olive Oil Market Growth Drivers

Health Awareness and Mediterranean Diet Adoption

Rising health consciousness among Australian consumers is the primary structural driver of olive oil market growth. Growing awareness of the cardiovascular, anti-inflammatory, and antioxidant benefits of olive oil—particularly extra virgin varieties rich in polyphenols, oleocanthal, and monounsaturated fatty acids—is driving a sustained shift away from saturated fats and refined cooking oils toward premium EVOO. The Mediterranean diet's recognition as one of the world's healthiest dietary patterns by leading health authorities is strongly influencing Australian culinary habits, with olive oil positioned as the foundational cooking fat in this dietary approach. Rising rates of lifestyle-related chronic conditions including cardiovascular disease, type 2 diabetes, and obesity are motivating Australian consumers to adopt healthier dietary choices, with olive oil consumption viewed as a practical and enjoyable health intervention. The growing clean-label and natural food movement is further reinforcing olive oil's position, as consumers seek minimally processed, single-ingredient products with transparent provenance and no artificial additives. This health-driven demand is particularly strong in the premium EVOO segment, where consumers are willing to pay higher prices for cold-pressed, certified, and provenance-verified products that maximize nutritional and flavor attributes.

Expanding Domestic Production and Industry Investment

The expansion and maturation of Australia's domestic olive oil production infrastructure is serving as a powerful growth driver by increasing supply availability, improving product freshness, and building consumer confidence in Australian-grown EVOO. Cobram Estate Olives, Australia's dominant producer, operates over 2.6 million olive trees across 7,000 hectares in Victoria with two on-site mills at Boundary Bend and Boort providing combined processing capacity of 144 tonnes per hour and 6.8 million litres of storage. The company's 2024-25 bumper harvest of 14.2 million litres—up 41% from 10.1 million litres the previous year—demonstrates the productivity gains from maturing groves and advanced agronomic practices. Cobram Estate's acquisition of Leda Ag (olive harvester manufacturer) in 2025 and its USD 473.5 million acquisition of California Olive Ranch in January 2026 exemplify the ambitious growth strategies of leading producers. The company raised AUD 178 million in capital to fund its expansion, including the development of 382 hectares of new groves in California, while group olive oil sales revenue reached AUD 237.4 million with EBITDA surging 75% to AUD 116.6 million. This investment cycle is strengthening Australia's position in the global olive oil industry and supporting the development of premium, internationally competitive EVOO brands.

Australia Olive Oil Market Segmentation

The Australia olive oil market report offers a comprehensive analysis across the following segments, providing detailed insights into market dynamics and growth trajectories:

Breakup by Product Type: Extra Virgin Olive Oil, Virgin Olive Oil, Refined Olive Oil, Olive Pomace Oil, Others

Extra virgin olive oil represents the largest and fastest-growing product segment, commanding dominant consumer preference driven by premiumization trends, clean-label demand, and growing awareness of EVOO's superior health benefits and flavor complexity. Refined olive oil maintains a significant share as an affordable everyday cooking option, though its growth rate lags the premium EVOO segment. Olive pomace oil serves cost-sensitive foodservice and industrial applications where high-volume cooking oil is required at lower price points.

Breakup by Packaging Type: Glass Bottles, PET Bottles, Tins and Cans, Pouches, Others

Glass bottles represent the dominant packaging format for premium EVOO products, valued for light protection, recyclability, and premium shelf presentation. PET bottles serve the mid-range and value segments with lighter weight and lower breakage risk for everyday cooking oil purchases. Tins and cans are favored for larger formats and by consumers seeking maximum light protection to preserve olive oil freshness and polyphenol content.

Breakup by Distribution Channel: Supermarkets and Hypermarkets, Specialty Food Stores, Online Retail, Foodservice, Others

Supermarkets and hypermarkets dominate olive oil distribution, with Woolworths and Coles offering extensive ranges spanning imported Mediterranean brands, domestic producers like Cobram Estate, and private-label organic and conventional olive oil products. Online retail represents the fastest-growing channel, driven by direct-to-consumer platforms, subscription models, and specialty food e-commerce. The foodservice channel is expanding as restaurants, cafés, and catering companies increasingly feature premium Australian EVOO as a menu differentiator.

Breakup by Region: New South Wales, Victoria, Queensland, Western Australia, South Australia, Others (including ACT, Tasmania, Northern Territory)

Victoria leads in domestic olive oil production, hosting Cobram Estate's 7,000-hectare operations and the majority of Australia's large-scale olive groves concentrated in the Wimmera, Mallee, and northern Victoria regions. New South Wales represents the largest consumption market, driven by Sydney's multicultural population and strong Mediterranean culinary influence. South Australia is a significant production and consumption region, with established olive groves in the Adelaide Hills, Barossa Valley, and Clare Valley regions producing premium artisanal EVOO products.

Australia Olive Oil Market Competitive Landscape

The Australia olive oil market features a competitive landscape comprising dominant domestic producers, established Mediterranean import brands, supermarket private-label offerings, and boutique artisanal producers. Key players operating in the market include Cobram Estate Olives (ASX: CBO), Moro (Accolade Foods), Red Island (Modern Olives), Alto Olives, Squeaky Gate, Woolworths (Macro), Coles (private label), Bertolli (Deoleo), Carbonell (Deoleo), and Filippo Berio (Salov Group). These organizations compete across product quality, brand heritage, provenance verification, price positioning, and retail distribution reach. Cobram Estate dominates domestic production with group olive oil sales revenue of AUD 237.4 million and a vertically integrated model spanning 2.6 million trees, proprietary harvesting technology, on-site milling, and branded retail distribution, while its January 2026 acquisition of California Olive Ranch for USD 473.5 million positions it as a global EVOO leader.

Australia Olive Oil Market: Latest News and Developments

Recent developments shaping the Australia olive oil market include:

• January 2026: Cobram Estate Olives completed the acquisition of California Olive Ranch—the leading producer and marketer of Californian extra virgin olive oil—for USD 473.5 million, significantly expanding its international production footprint and establishing a dual-hemisphere supply model spanning Australia and the United States.

• 2025: Cobram Estate reported a bumper 2024-25 Australian harvest of 14.2 million litres (up 41% from 10.1 million litres the prior year), with group olive oil sales revenue reaching AUD 237.4 million and EBITDA surging 75% to AUD 116.6 million, reflecting the commercial strength of premium domestic production.

• 2025: Cobram Estate acquired Leda Ag, the manufacturer of olive harvesters, strengthening its vertically integrated supply chain from proprietary harvesting technology through milling, storage, and branded retail distribution, and raised AUD 178 million in capital to fund US growth strategy including 382 hectares of new grove development in California.

• 2024/25: Australian olive oil imports reached 42,272 tonnes in the 2024/25 crop year, representing a 46% increase compared to the 2023/24 crop year, reflecting strong and growing consumer demand driven by health awareness, Mediterranean diet adoption, and expanding culinary applications.

• 2025: Cobram Estate's Australian branded sales grew 16.6% to AUD 141.4 million, demonstrating the strength of consumer preference for premium domestically produced extra virgin olive oil and the effectiveness of provenance-based brand positioning in the competitive retail environment.

Note: If you require any specific information not currently covered within the scope of the report, IMARC Group will provide it as part of customization.

Speak to an analyst:

https://www.imarcgroup.com/request?type=report&id=32933&flag=C

What's Your Reaction?