Australia Self Storage Market Size, Share, Report 2026–2034

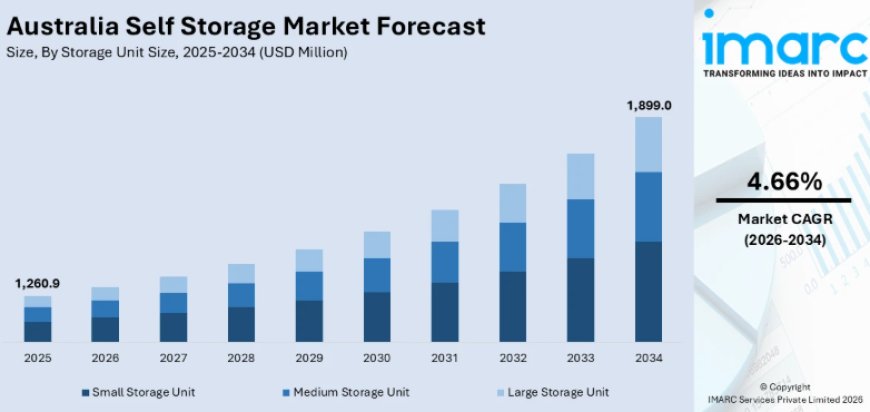

The Australia Self Storage Market reached a size of USD 1,260.9 Million in 2025 and is projected to reach USD 1,899.0 Million by 2034, growing at a CAGR of 4.66% during the forecast period of 2026–2034.

Market Overview

The Australia Self Storage Market reached a size of USD 1,260.9 Million in 2025 and is projected to reach USD 1,899.0 Million by 2034, growing at a CAGR of 4.66% during the forecast period of 2026–2034. The market is driven by rising urban density, shrinking home sizes, frequent housing transitions, e-commerce expansion, changing apartment living trends, regional migration, and downsizing among older adults. With over 2,500 self-storage facilities already operating across the country — and more than 200 new facilities in the pipeline led by New South Wales and Victoria — the Australian self-storage sector has matured into a standalone institutional asset class attracting global private equity, sovereign wealth funds, and listed REITs at unprecedented investment volumes. Australia's supply sits at 0.23 sqm per capita — positioned between the more saturated US market at 0.72 sqm per capita and the UK at 0.14 sqm per capita — indicating substantial structural room for continued supply growth before market saturation. The three dominant operators are ASX-listed National Storage REIT with over 250 centres, ASX-listed Abacus Storage King with approximately 150 centres, and family-owned Kennards Self Storage with over 100 centres — together accounting for approximately 30% market share alongside mid-sized operators at 16%, with 54% of facilities still operated by single-site operators that represent the ongoing consolidation opportunity. Average monthly storage rates have held steady at AUD 266–269 per square metre through 2024–2025 — with medium operators leading at 7.6% rate growth, large operators posting modest gains, and REITs seeing a 4.4% rate decline as they compete for occupancy to justify their massive acquisition investment. New South Wales and Victoria are the leading and fastest-growing regional markets through the highest concentration of urban population, housing density pressure, and e-commerce activity of any Australian states.

How AI is Reshaping the Future of the Australia Self Storage Market:

- AI-powered dynamic pricing platforms — deployed by National Storage REIT, Abacus Storage King, and StorHub — are using machine learning models that analyze local occupancy rates, competitor pricing, search traffic patterns, and seasonal demand signals in real time to dynamically set storage unit prices at the unit-type and facility level, enabling operators to maximize revenue per available square metre during high-demand periods while using targeted promotional pricing to maintain occupancy during softer periods — with the growing gap between street and online promotional rates (expanding from under 1% in 2022 to nearly 3% in 2023 before settling at approximately 2% in 2024) reflecting the increasing sophistication of digital-first acquisition strategies.

- StorHub Australia — backed by USD 300 Million of Warburg Pincus equity committed at launch in March 2024 — is deploying a state-of-the-art technology platform across its 11 Australian sites including AI-powered inventory management, digital self-service kiosks, automated unit access systems, and real-time facility security monitoring that is establishing a new operational technology benchmark for the Australian self-storage sector that traditional single-site operators cannot replicate.

- AI-driven customer acquisition and conversion optimization platforms — used by major Australian self-storage operators across Google Ads, Meta, and SEO — are applying machine learning to search intent signals, competitor availability data, and historical conversion patterns to dynamically allocate digital marketing spend toward the highest-converting facility-level keyword and audience combinations, with Citi's Self-Storage Website Tracker finding website visits up 17% in September 2024 versus the prior year led by National Storage — demonstrating the commercial impact of data-driven digital acquisition investment.

- Smart access technology — including app-controlled digital locks, QR code entry systems, automated kiosks for after-hours unit access, and AI-powered surveillance cameras with motion detection and anomaly alerts — is becoming a baseline operational requirement for competitive self-storage facilities in Australia, enabling 24/7 unmanned operations that reduce staffing costs while simultaneously improving security outcomes and customer convenience satisfaction scores that drive referral and retention.

- The AUD 270 Million GIC-NSR joint venture fund — launched in June 2024 — is applying institutional-grade financial modelling and AI-supported site selection analytics to identify optimal locations for ten new self-storage construction projects across Australia, using machine learning models that integrate population growth projections, housing density mapping, competitor proximity analysis, and demographic demand indicators to optimize facility placement decisions at a level of analytical sophistication that is reshaping what development underwriting looks like in Australian self-storage.

Request Industry-Focused Sample with Insights & Forecasts: https://www.imarcgroup.com/australia-self-storage-market/requestsample

Market Trends and Insights

- Institutional Capital Reshaping the Competitive Landscape: 2025 has delivered over AUD 1 Billion in self-storage transactions — a single-year record that exceeds the cumulative deal volume of many prior years combined — with BlackRock's entry through the acquisition of a controlling interest in StoreLocal for over AUD 450 Million (including 24 StoreLocal facilities and 13 third-party managed sites) joining GIC's AUD 270 Million NSR joint venture, StorHub's AUD 460 Million equity commitment, and SIA's AUD 40 Million development fund as transformative capital events that are consolidating ownership, driving yield compression, and elevating facility quality standards across the market.

- E-Commerce Driving Commercial Storage Demand: Australia's e-commerce market was valued at approximately USD 536 Billion in 2024 — growing at a CAGR of 12.7% through 2033 — with online retailers, home-based businesses, sole traders, and small e-commerce operators collectively representing a fast-growing commercial self-storage demand segment that values the flexibility, scalability, and lower overhead of climate-controlled self-storage units as an alternative to expensive commercial warehouse leases, with value-added services including parcel acceptance, delivery coordination, shelving, co-working space, and free Wi-Fi increasingly available at premium self-storage facilities.

- Housing Market Volatility Sustaining Transitional Demand: Elevated mortgage rates, record property prices, and volatile settlement timelines are compelling increasing numbers of Australian households to use self-storage as a transitional buffer — storing belongings between property purchases, during rental periods, throughout renovation delays, and across the frequent interstate relocations driven by remote-work-enabled lifestyle migration patterns — with facility operators responding through flexible month-to-month lease terms, 24/7 access, and digital facility management tools that accommodate the mobile and unpredictable nature of transitional storage demand.

- Regional Expansion Extending Market Penetration: The geographic diversification of self-storage facility development beyond inner-city Melbourne, Sydney, and Brisbane into outer suburban growth corridors — including Western Sydney, South East Queensland, and Melbourne's northern growth areas — and regional centres is addressing storage shortages in previously underserved communities, with highway-adjacent and industrial zone-proximate facility locations capturing both residential and commercial demand from populations who have migrated regionally for affordability and lifestyle reasons but have brought the storage habits of their prior metropolitan lives.

- Ageing Population Creating Stable Long-Term Demand: Australia's growing population of over-65s — projected to reach 22% of the total population by 2066 — is generating a reliable and growing self-storage demand segment as older adults downsize from family homes to retirement villages, aged care facilities, or low-maintenance apartments, storing furniture, family heirlooms, and sentimental belongings that they are unwilling to discard but cannot accommodate in their new compact living arrangements — with user-friendly access, flat-rate pricing transparency, ground-level unit availability, and proximity to residential aged care precincts emerging as the primary facility attributes for this growing demographic.

Small storage units dominate by volume — serving the dominant residential downsizing, decluttering, and student/young adult transitional use cases that characterize Australia's personal self-storage demand base — while medium storage units serve the core household relocation and small business inventory storage needs that generate the longest average tenure and highest revenue per unit. Large storage units serve commercial clients including e-commerce businesses, tradespeople, and event equipment operators and command premium rental rates that drive disproportionate revenue contributions. By end use, personal is the dominant segment by unit count while business is growing as the fastest-expanding segment by revenue contribution — driven by e-commerce expansion, the proliferation of home-based businesses, and the growing awareness of self-storage as a cost-effective commercial storage solution. Regionally, New South Wales leads through Sydney's acute housing density pressure and the highest concentration of e-commerce and small business activity, followed by Victoria through Melbourne's comparable urban dynamics, and Queensland as the fastest-growing regional market through its sustained interstate migration inflow.

Market Growth Drivers

Urban Density and Residential Downsizing

The structural shift toward high-density urban living is the primary foundational driver of Australian self-storage demand — with approximately 86.6% of Australia's 27 million population residing in urban areas and new residential developments overwhelmingly targeting high-rise apartment and compact townhouse formats that offer substantially less in-unit storage space than the detached houses they are replacing. As Sydney, Melbourne, and Brisbane continue their upward development trajectories — driven by planning reforms, housing affordability imperatives, and transit-oriented development policies — the average new apartment is delivering 15–30% less storage space than comparable dwellings built 20 years ago, structurally requiring residents to seek off-site storage solutions for seasonal items, recreational equipment, archived documents, and possessions that do not fit comfortably within their living space. Developers are actively marketing compact apartments with the explicit assumption that residents will supplement their storage externally — further normalizing self-storage as a standard complement to urban apartment living — and operators are responding by targeting high-density residential precincts for new facility development with convenient, easily accessible, well-secured units tailored to apartment dwellers' needs.

E-Commerce Growth and Small Business Storage Needs

The sustained expansion of Australia's e-commerce sector — valued at approximately USD 536 Billion in 2024 with a projected CAGR of 12.7% through 2033 — is generating consistent and growing demand for self-storage from online retailers and small-scale entrepreneurs who need affordable, scalable, and flexible inventory storage solutions. Self-storage units serve as the most cost-effective and operationally flexible alternative to commercial warehouse leasing for the growing cohort of Australians operating home-based businesses, solo e-commerce operations, and side-hustle retail activities that collectively represent a material portion of Australia's small business formation and growth. StorHub Australia has directly responded to this demand by offering tailored business storage solutions including co-working spaces, free Wi-Fi, and printing services at its facilities — demonstrating that premium self-storage operators recognize the commercial opportunity in serving the full small-business operating environment rather than purely providing secure square meterage. Value-added services including parcel acceptance, delivery coordination, professional shelving installations, and oversized item handling are progressively differentiating business-friendly self-storage facilities from residential-focused competitors.

Regional Expansion and Infrastructure Investment

Australia's self-storage market is extending its geographic footprint beyond saturated major urban centres into fast-growing regional hubs and outer suburban growth corridors — driven by the interstate and intrastate population migrations that accelerated post-COVID as Australians leveraged remote work flexibility to pursue regional lifestyle and affordability options. NSR's dual strategy of acquisitions and developments — with 52 projects underway by early 2025 after completing 20 acquisitions and 7 new developments — alongside SIA's AUD 40 Million development fund targeting high-demand urban and regional markets and StorHub's stated intent to expand to Brisbane and additional gateway cities reflects the industry's confidence in regional demand durability. Infrastructure upgrades including improved highway access, regional town centre expansion, and industrial zone development are enhancing site feasibility for new regional facilities — with highway-adjacent locations particularly valuable for both residential and commercial self-storage customers who prioritize vehicle accessibility and operational convenience when selecting storage solutions.

Market Segmentation

Storage Unit Size Insights:

- Small Storage Unit

- Medium Storage Unit

- Large Storage Unit

End Use Insights:

- Personal

- Business

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Recent News and Developments

- May 2025: BlackRock — the world's largest asset manager — announced its entry into the Australian self-storage market through acquisition of a controlling interest in StoreLocal for over AUD 450 Million, including 24 self-storage facilities under the StoreLocal brand and 13 third-party managed sites across Australia, establishing BlackRock's direct position in Australian self-storage real estate and signaling the sector's ascent to global institutional asset class status.

- 2025: Abacus Storage King received and then saw withdrawn a takeover offer — with a second bid lodged at AUD 1.65 per security in July before being retracted in August 2025 — confirming both the high institutional appeal of Australia's listed self-storage REITs to global operators and the complexity of executing large-scale consolidation transactions in a sector where publicly listed operator valuations reflect premium asset quality expectations.

- June 2024: GIC — Singapore's sovereign wealth fund — partnered with National Storage REIT in a AUD 270 Million joint venture to fund 10 new self-storage construction projects across Australia over 12–18 months, with GIC holding 75% and NSR managing the fund and retaining 25%, representing the most significant sovereign capital commitment to Australian self-storage development in the sector's history.

- Q4 2024: StorHub acquired three Sydney self-storage facilities in Homebush, Forestville, and Revesby for approximately AUD 110 Million — adding over 18,000 sqm of net lettable area and nearly 2,000 units — expanding its Australian portfolio to 11 sites with over 110,000 sqm of gross floor area valued at more than AUD 420 Million and positioning itself as Australia's fastest-growing institutional self-storage operator.

- 2024: National Storage REIT acquired a self-storage portfolio from MAAS Group Holdings for USD 32 Million — continuing its dual roll-up and development strategy that had reached 20 acquisitions and 7 developments by early 2025 with 52 projects underway — while Storage Investment Australia raised AUD 40 Million to fund a development pipeline targeting a long-term AUD 1 Billion portfolio.

- March 2024: StorHub launched its Australian operations backed by a USD 300 Million equity commitment from Warburg Pincus — seeded with five quality assets in Sydney, Melbourne, and Canberra totalling 56,210 sqm gross floor area — announcing its intent to become one of Australia's leading self-storage platforms through a buy-and-build strategy targeting gateway cities including Sydney, Melbourne, and Brisbane.

Note: If you need specific information that is not currently within the scope of the report, we can provide it to you as a part of the customization.

Ask analyst for your customized sample:

https://www.imarcgroup.com/request?type=report&id=33038&flag=F

About Us

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC's offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 433 0800

United States: +1-201-971-6302

What's Your Reaction?