Australia Plant-based Seafood Market Size, Share, Report 2026‑2034

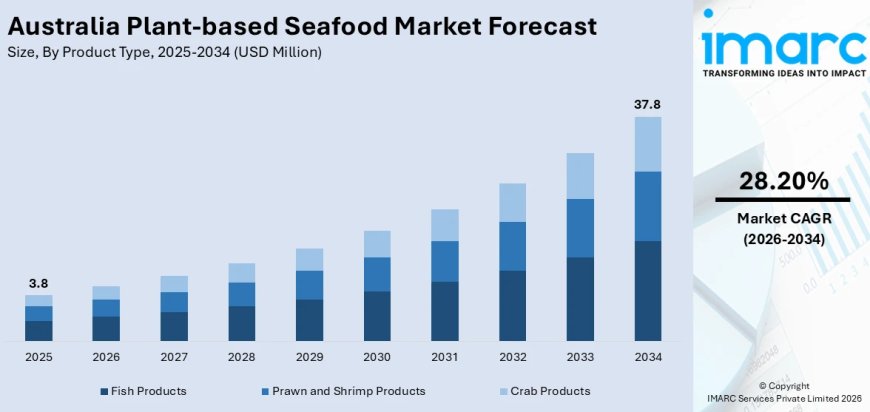

Australia plant-based seafood market size reached USD 3.8 Million in 2025 and is projected to reach USD 37.8 Million by 2034, exhibiting a compound annual growth rate (CAGR) of 28.20% from 2026‑2034

Market Overview

The Australia plant-based seafood market is witnessing explosive growth driven by rising environmental consciousness regarding ocean biodiversity and marine conservation, growing consumer interest in health and nutrition, and increasing innovation and product development by food tech companies. The market size reached USD 3.8 Million in 2025 and is projected to reach USD 37.8 Million by 2034, exhibiting a compound annual growth rate (CAGR) of 28.20% from 2026‑2034. Australia's unique geographical position, being surrounded by marine ecosystems like the Great Barrier Reef, is making the public more environmentally conscious, further accelerating plant-based seafood adoption.

This market is strategically important to Australia's food innovation and sustainability economy, supporting a dynamic food tech ecosystem funded by government subsidies and research partnerships. The combination of health awareness, environmental concerns, and product innovation continues to reinforce the Australia plant-based seafood market share across retail and food service channels.

The Australia plant-based seafood market is poised for sustained expansion, driven by environmental sustainability concerns, health consciousness, and food tech innovation. With a projected CAGR of 28.20% through 2034, the market presents significant opportunities for manufacturers focusing on realistic plant-based seafood alternatives and sustainable frozen food products.

AUSTRALIA PLANT-BASED SEAFOOD MARKET SUMMARY

- The Australia plant-based seafood market encompasses a range of seafood alternatives made from plant-based ingredients, including fish products, prawn and shrimp products, and crab products, designed to replicate the taste, texture, appearance, and nutritional content of traditional seafood.

- The ecosystem spans food tech startups, traditional food companies, research institutions, universities, distribution channels, and government funding bodies, supported by R&D tax credits and partnerships between food scientists and private companies.

- Major segments identified in the plant-based seafood industry include product type (fish products, prawn and shrimp products, crab products), distribution channel (supermarkets and hypermarkets, convenience stores, online, others), and region (Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia).

- Key innovations rely on ingredients such as soy, legumes, algae, seaweed, jackfruit, and mycoprotein to mimic seafood types including fish fillets, prawns, tuna, squid, and crab.

- The market is characterised by a dynamic food innovation ecosystem funded by government subsidies, R&D tax credits, and partnerships between food scientists, universities, and private companies, resulting in seafood products that appeal not only to vegetarians and vegans but also to mainstream consumers seeking culinary diversity.

PORTER'S FIVE FORCES ANALYSIS – AUSTRALIA PLANT-BASED SEAFOOD MARKET

The competitive dynamics of the Australia plant-based seafood market can be analysed using Porter's Five Forces framework.

Bargaining Power of Suppliers – Moderate

- Manufacturers rely on suppliers of plant-based ingredients including soy, legumes, algae, seaweed, jackfruit, and mycoprotein. Australia's established agricultural sector provides multiple sourcing options. However, the specialised nature of certain ingredients for realistic seafood alternatives gives niche suppliers moderate leverage.

Bargaining Power of Buyers – Moderate

- Australian consumers benefit from a growing range of plant-based seafood products across supermarkets, online platforms, and convenience stores. Health-conscious and environmentally aware buyers have increasing choice, strengthening their negotiating position. According to the Australian Burden of Disease Study 2024, approximately 8.3% of the overall disease burden was attributed to being overweight (which includes obesity), driving preventive health purchases.

Threat of New Entrants – Moderate

- Significant capital requirements for R&D, formulation development, and distribution networks create barriers for traditional entrants. However, Australia's dynamic food innovation ecosystem, funded by government subsidies and R&D tax credits, enables startups to access the market with differentiated offerings.

Threat of Substitutes – Low

- Traditional seafood represents the primary substitute category, but growing consumer concerns about mercury, microplastics, overfishing, and marine ecosystem damage are driving the shift toward plant-based alternatives. Plant-based seafood provides a powerful substitute high in protein and omega-3 fatty acids derived from algae without allergens and toxins.

Competitive Rivalry – High (Healthy)

- The market features intensifying competition among food tech startups and traditional food companies investing in realistic plant-based seafood alternatives. Competition is driven by product authenticity, nutritional profile, sustainability credentials, and distribution reach rather than purely price-based rivalry.

Request a Business Sample Report for Procurement & Investment Evaluation:

https://www.imarcgroup.com/australia-plant-based-seafood-market/requestsample

MARKET GROWTH DRIVERS

Rising Consumer Awareness of Health and Nutrition

Several key factors are propelling market growth in the Australia plant-based seafood market. The growing consumer interest in health and nutrition is offering a favourable market outlook in Australia. Consumers are increasingly becoming aware of food choices, thereby looking for foods that promote heart health, lower cholesterol levels, and reduce exposure to toxic substances present in traditional seafood, including mercury and microplastics. Vegetarian seafood provides a powerful substitute, which tends to be high in protein, omega-3 fatty acids derived from algae, and critical micronutrients without allergens and toxins inherent in fish and shellfish. Increasing incidences of lifestyle disorders like obesity, cardiovascular diseases, and diabetes is increasing the consumption of functional foods aligned with preventive health practices, supported by government and non-government health campaigns advocating plant-based diets.

Environmental and Sustainability Concerns

Environmental sustainability is one of the key drivers for the consumption of plant-based seafood in Australia. Consumers and businesses alike are being stimulated to adopt more sustainable alternatives due to concerns regarding overfishing, damage to marine ecosystems, bycatch, and the greenhouse gas emissions associated with seafood production. Australia's location, surrounded by marine ecosystems like the Great Barrier Reef, is making the public more environmentally conscious, particularly regarding ocean biodiversity and marine conservation. Seafood alternatives made from plants offer low-impact nutrition compared to conventionally produced seafood, using substantially fewer natural resources like water and land and releasing fewer greenhouse gases in production, aligning with larger sustainability goals shared by Australian consumers, policymakers, and food providers. Sustainable frozen food requirement, especially vegan seafood, is rising across the country.

Innovation and Product Development by Food Tech Companies

Food technology innovation is contributing significantly to market growth. Startups and traditional food businesses are investing in creating realistic plant-based seafood alternatives that mimic the taste, texture, appearance, and nutritional content of traditional seafood. These innovations rely on ingredients such as soy, legumes, algae, seaweed, jackfruit, and mycoprotein to mimic seafood types including fish fillets, prawns, tuna, squid, and crab. Australia's dynamic food innovation ecosystem, funded by government subsidies, R&D tax credits, and partnerships between food scientists, universities, and private companies, is resulting in the development of seafood products that find appeal not only among vegetarians and vegans but also among mainstream consumers seeking culinary diversity.

AUSTRALIA PLANT-BASED SEAFOOD MARKET SEGMENTATION

Segmentation analysis provides a detailed view of the Australia plant-based seafood market by category:

- Product Type Insights: Fish Products, Prawn and Shrimp Products, Crab Products.

- Distribution Channel Insights: Supermarkets and Hypermarkets, Convenience Stores, Online, Others.

- Regional Insights: Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia.

COMPETITIVE LANDSCAPE

The competitive landscape of the Australia plant-based seafood market is dynamic, featuring a mix of food tech startups and traditional food businesses investing in realistic plant-based seafood alternatives. The market research report has provided a comprehensive analysis of the competitive landscape, including market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant, with detailed profiles of all major companies provided in the full report. The market is shaped by continuous investment in R&D, ingredient innovation, and distribution network expansion. Investment opportunities exist in product development for realistic seafood alternatives, sustainable frozen food solutions, and partnerships with research institutions.

REGIONAL ANALYSIS

- Australia Capital Territory & New South Wales represents a critical demand centre, anchored by Sydney's large population, high concentration of health-conscious consumers, and well-developed retail infrastructure supporting plant-based seafood availability across supermarkets and online platforms.

- Victoria & Tasmania benefits from Melbourne's vibrant food innovation ecosystem, with strong demand for plant-based alternatives and access to research institutions supporting food tech development.

- Queensland sees rising plant-based seafood demand driven by the state's proximity to the Great Barrier Reef and heightened environmental consciousness regarding marine conservation.

- Western Australia experiences steady growth supported by Perth's health-conscious demographic and increasing availability of sustainable frozen food products.

- Northern Territory & Southern Australia, though smaller in market share, are benefiting from improved retail accessibility and growing consumer awareness of plant-based seafood alternatives.

RECENT INDUSTRY DEVELOPMENTS

- 2025 Activity: The Australia plant-based seafood market continued its rapid growth trajectory, driven by environmental sustainability concerns, health awareness, and food tech innovation.

- 2025 Activity: Startups and traditional food businesses continued investing in realistic plant-based seafood alternatives mimicking the taste, texture, appearance, and nutritional content of traditional seafood, relying on ingredients such as soy, legumes, algae, seaweed, jackfruit, and mycoprotein.

- 2024 Activity: The Australian Burden of Disease Study 2024 reported that approximately 8.3% of the overall disease burden was attributed to being overweight (which includes obesity), highlighting the growing importance of preventive health practices and plant-based nutrition.

Note: If you need any specific information that is not covered currently within the scope of the report, we will provide the same as a part of customization.

https://www.imarcgroup.com/request?type=report&id=32484&flag=E

ABOUT US

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

CONTACT US

IMARC Group

134 N 4th St., Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 433 0800

United States: +1 201 971 6302

What's Your Reaction?