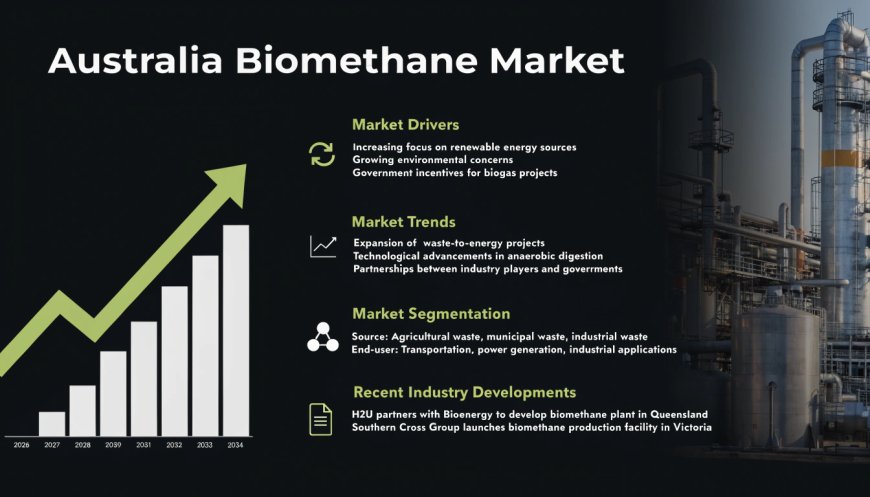

Australia Biomethane Market Size, Share, Report 2026-2034

The Australia biomethane market size was valued at USD 180.59 Million in 2025 and is projected to reach USD 539.95 Million by 2034, growing at a compound annual growth rate of 12.94% from 2026-2034.

Market Overview

The Australia biomethane market is gaining significant momentum as the nation accelerates its transition toward renewable gas solutions and sustainable energy pathways. According to IMARC Group, the market size was valued at USD 180.59 Million in 2025 and is projected to reach USD 539.95 Million by 2034, exhibiting a compound annual growth rate (CAGR) of 12.94% during 2026‑2034. Increasing government commitment to decarbonising hard‑to‑abate industrial sectors, expanding waste‑to‑energy infrastructure, and growing circular economy practices are strengthening adoption. Advancements in anaerobic digestion technologies, rising demand for carbon‑neutral gas alternatives, and strategic investments in biogas upgrading systems are reshaping the energy landscape, positioning Australia as an emerging hub for renewable gas production. This market is strategically important to Australia’s economy as it supports the nation’s net‑zero by 2050 target, diversifies the energy mix, strengthens waste management systems, and creates new economic opportunities across regional communities.

The Australia biomethane market is poised for sustained expansion, driven by a projected CAGR of 12.94% through 2034, abundant domestic feedstocks, and strengthening state and federal policy frameworks. With leading energy infrastructure operators and renewable gas developers advancing biomethane injection projects, the market presents significant opportunities for investors, technology providers, and industrial energy users seeking a drop‑in renewable gas solution that leverages existing natural gas infrastructure.

Australia Biomethane Market Summary

- The Australia biomethane market encompasses the production, upgrading, and utilisation of renewable natural gas derived from organic waste feedstocks through anaerobic digestion and other conversion technologies.

- The ecosystem includes feedstock suppliers (agricultural waste, municipal solid waste, sewage sludge, food processing residues), biomethane producers, gas network operators, energy retailers, industrial end‑users, government agencies, and technology providers.

- Major segments identified in the market include feedstock (organic residue and wastes dominate with 72.4% share in 2025), application (power generation leads with 54.6% share), production method (anaerobic digestion exhibits a clear dominance with 81.9% share), and region (Australia Capital Territory & New South Wales represents the largest region with 34.7% share).

- Organic residue and waste‑based feedstocks form the backbone of Australia’s biomethane production ecosystem, driven by the consistent year‑round availability of municipal solid waste, sewage sludge, and food processing residues.

- Power generation leads the market due to growing integration of biogas‑derived electricity into the national grid and increasing demand for dispatchable renewable energy sources to complement intermittent solar and wind generation.

- Anaerobic digestion remains the dominant production method, reflecting its proven reliability, technological maturity, and suitability for processing diverse organic waste feedstocks.

- Australia Capital Territory & New South Wales leads the market, driven by historic biomethane infrastructure projects, significant urban waste production, and strong government support for renewable gas projects, particularly throughout the Sydney metropolitan area.

PORTER’S FIVE FORCES ANALYSIS – AUSTRALIA BIOMETHANE MARKET

The competitive dynamics of the Australia biomethane market can be analysed using Porter’s Five Forces framework.

Bargaining Power of Suppliers – Moderate

The market relies on a mix of feedstock suppliers, biogas upgrading technology providers, and gas network operators. Abundant domestic feedstock availability — with approximately 400 petajoules of biomethane recoverable annually from existing feedstocks — gives Australian producers access to diverse input sources, moderating supplier power. However, specialised technology suppliers of anaerobic digestion and gas upgrading equipment hold some influence due to their technical expertise.

Bargaining Power of Buyers – Moderate to High

Buyers include industrial gas users, energy retailers, and gas network operators. Industrial end‑users seeking to reduce Scope 1 emissions under the Safeguard Mechanism have strong incentives to secure renewable gas supplies. Major energy retailers such as Origin Energy are entering long‑term offtake agreements, providing producers with revenue certainty while giving buyers negotiating leverage over price and volume terms.

Threat of New Entrants – Moderate

Capital requirements for biomethane production facilities are substantial, with projects typically requiring significant investment in anaerobic digestion units, biogas upgrading equipment, and grid injection infrastructure. However, government grant programs (including ARENA’s National Industrial Transformation Program and state‑level initiatives) and long‑term offtake agreements are lowering entry barriers. The emerging status of the Australian market creates opportunities for new entrants with proven international expertise.

Threat of Substitutes – Low

Biomethane offers unique advantages as a direct, carbon‑neutral substitute for fossil natural gas that can be seamlessly integrated into existing pipeline networks without requiring appliance modifications. While electrification, green hydrogen, and synthetic methane represent alternative decarbonisation pathways, biomethane remains the most readily deployable solution for hard‑to‑abate industrial sectors reliant on high‑temperature gas applications. The ability to use existing gas infrastructure limits substitution pressure.

Competitive Rivalry – Moderate

The market is currently in an emerging growth phase, with a limited number of operational biomethane injection facilities. Key players such as Delorean Corporation, Jemena, Optimal Renewable Gas, AGIG, Origin Energy, and LMS Energy are competing to establish first‑mover advantages through project development, strategic partnerships, and long‑term offtake agreements. As additional projects reach commercial operation, competitive rivalry is expected to intensify.

Request for Sample Report: https://www.imarcgroup.com/australia-biomethane-market/requestsample

MARKET GROWTH DRIVERS

Abundant Feedstock Availability and Waste‑to‑Energy Circular Economy Expansion

A primary factor propelling the Australia biomethane market is the country’s abundance of organic waste feedstocks suitable for biomethane production. A study commissioned for Energy Networks Australia estimates that approximately 400 petajoules of biomethane per year could be recoverable today from existing feedstocks such as food and garden waste, agricultural residues, livestock by‑products, and municipal solid waste. Urban areas generate substantial volumes of organic waste through established collection systems, creating a reliable and cost‑effective feedstock supply for anaerobic digestion facilities. Australia is rapidly developing circular economy systems that convert organic waste into renewable energy and useful by‑products, diverting municipal, commercial, and agricultural waste from landfills while producing biomethane, biogenic carbon dioxide, and organic fertilisers. This dual benefit of waste diversion and renewable energy generation is strengthening the commercial case for biomethane facilities across the country, positioning the market for substantial expansion as both state and federal governments implement waste diversion mandates and circular economy policies.

Strengthening Federal and State Policy Frameworks

The Australia biomethane market is benefiting from a strengthening policy environment at both federal and state levels. The Australian Government’s 2024 Future Made in Australia initiative allocated AUD 22.7 billion over the next decade to the Australian Renewable Energy Agency to support the commercialisation of low‑carbon fuels including biomethane, reinforcing the nation’s commitment to renewable gas development. In 2025, the government commenced consultation on expanding the Guarantee of Origin scheme to include biogas and biomethane, which will enable producers to make verifiable environmental claims and access low‑emissions markets. The Electricity and Energy Sector Plan 2025 envisages that renewable gases will increasingly support decarbonisation in hard‑to‑abate sectors between 2030 and 2035, with renewable gases and fuel‑switching forming an important part of the energy mix by 2050. At the state level, NSW has introduced a $40 million Renewable Gas Production Program to boost biomethane production, co‑funding up to 50% of project costs with eligible projects required to inject at least 0.1 petajoules annually into the network by June 2030. Victoria’s Gas Substitution Roadmap sets out a path for transitioning away from fossil gas use, while NSW is developing a Renewable Fuel Strategy that includes establishing a biomethane and green hydrogen target increasing to 8 million gigajoules by 2038.

Growing Industrial Demand for Carbon‑Neutral Gas Alternatives

The Australia biomethane market is being shaped by rising demand from industrial sectors seeking to decarbonise their operations. Policy encouragement through emission reduction frameworks such as the Safeguard Mechanism, expanding waste diversion mandates, and rising demand from hard‑to‑abate manufacturing sectors reliant on high‑temperature gas applications are contributing to a favourable investment environment. Biomethane can be used as a drop‑in replacement for natural gas, which is widely used by industry, commercial businesses, and households in Australia. Australia’s gas infrastructure can be readily adapted for biomethane injection, and pipeline operators are already facilitating injection into the grid, limiting downstream transition costs for domestic and industrial customers. Major energy retailers and industrial gas users are entering long‑term biomethane offtake agreements, providing revenue certainty that enhances project bankability and supports facility construction.

MARKET GROWTH DRIVERS

Pioneering Biomethane Grid Injection Infrastructure

The Australia biomethane market is advancing through pioneering grid injection demonstration projects and evolving technical standards. The Malabar Biomethane Injection Plant, developed by Jemena in partnership with Sydney Water, became Australia’s first facility to inject biomethane into a gas distribution network in 2023, initially producing around 95 terajoules of renewable gas annually for approximately 6,300 homes. This milestone has catalysed broader industry interest in scaling biogas‑to‑grid infrastructure across multiple states. In South Australia, the Australian Gas Infrastructure Group has signed a formal agreement to connect Delorean Corporation’s SA1 bioenergy facility, with up to 210 terajoules of biomethane generated from commercial and industrial organic waste to be injected into the existing gas network each year. These demonstration projects demonstrate the technical, operational, and commercial foundations required to support biomethane upgrading and injection within Australian gas networks, providing templates for replication across the country.

Advancements in Anaerobic Digestion and Biogas Upgrading Technologies

Technological advancements are enhancing the efficiency and reducing the costs of biomethane production. Anaerobic digestion exhibits a clear dominance in the market, reflecting its proven reliability, technological maturity, and suitability for processing diverse organic waste feedstocks including municipal waste, sewage sludge, and agricultural residues. Biomethane grid injection is emerging as a commercially viable pathway in Australia, supported by pioneering demonstration projects and evolving technical standards. The Energy Networks Australia report indicates that the first 50 petajoules of biomethane could be delivered at $10–27 per gigajoule, with costs expected to fall further through supportive policy and improved recovery practices. As facilities scale up and operators gain operational experience, production costs are projected to decline, improving the commercial competitiveness of biomethane relative to fossil natural gas.

Strategic Partnerships and Long‑Term Offtake Agreements

Strategic partnerships between energy infrastructure companies, waste processors, and industrial end‑users are accelerating market development. In September 2025, Delorean Corporation secured a binding gas sales agreement with Origin Energy for the long‑term supply of renewable natural gas, with Origin purchasing up to 200 terajoules of biomethane per annum on a take‑or‑pay basis for eight years. In March 2025, Delorean signed a $6.08 million grant funding agreement with ARENA to enhance its SA1 bioenergy facility, enabling the production of mains‑grade biomethane injected into AGIG’s gas network. Optimal Renewable Gas has set a target of ten large‑scale biohubs in development by 2030, with combined annual production of up to ten petajoules, partnering with Jemena Gas Networks, Baiada Poultry, and Osaka Gas Australia. These collaborations are providing the commercial certainty needed to attract investment, secure financing, and scale production across the Australian market.

Australia Biomethane Market Segmentation

Segmentation analysis provides a detailed view of the Australia biomethane market by category:

- Feedstock Insights: Organic Residue and Wastes (including Biowaste, Municipal Waste, Sewage Waste, Agricultural Waste, Others), Energy Crops.

- Application Insights: Power Generation, Heating, Transportation Fuel, Industrial Feedstock, Others.

- Production Method Insights: Anaerobic Digestion, Gasification, Pyrolysis, Others.

- Regional Insights: Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia.

Competitive Landscape

The competitive landscape of the Australia biomethane market features a mix of energy infrastructure operators, renewable gas developers, waste management companies, and energy retailers. Key players are expanding production capacities, investing in advanced biogas upgrading technologies, and forging strategic partnerships with gas network operators. Their investments in circular economy infrastructure, waste processing capabilities, and renewable gas certification are boosting awareness, accelerating commercial deployment, and ensuring consistent biomethane availability across diverse industrial and residential segments. Key companies and strategic developments include:

- Delorean Corporation (ASX: DEL) – The only ASX‑listed company leading with bioenergy and commercial production of renewable gas in the form of biomethane. Owns the SA1 bioenergy facility in South Australia (processing up to 70,000 tonnes of organic waste annually, producing up to 210 terajoules of biomethane). Secured a $6.08 million ARENA grant and an eight‑year gas sales agreement with Origin Energy for up to 200 terajoules per annum. Developing NSW1 Brickworks Bioenergy Plant (120,000 tonnes per annum capacity, 253,000 gigajoules of biomethane annually) and VIC1 Stanhope Bioenergy Plant.

- Jemena – Operates Australia’s first biomethane injection plant in Malabar, Sydney, producing enough renewable gas annually to power the equivalent of 6,300 homes. The Malabar Biomethane Injection Plant became Australia’s first facility to inject biomethane into a gas distribution network in 2023.

- Optimal Renewable Gas (ORG) – Awarded a 20 million NSW government grant for the Griffith Biohub, a 58 million project processing up to 100,000 tonnes of agricultural waste annually, producing around 460 terajoules of biomethane. Has set a target of ten large‑scale biohubs in development by 2030, with combined annual production of up to ten petajoules.

- Australian Gas Infrastructure Group (AGIG) – Has a goal to deliver 100% renewable and carbon‑neutral gas in its distribution networks by 2050. Signed a formal agreement to connect Delorean’s SA1 biomethane project into its South Australian gas networks.

- Origin Energy (ASX: ORG) – Entered an eight‑year binding gas sales agreement with Delorean Corporation for the long‑term supply of biomethane, supporting emissions reduction in hard‑to‑abate sectors.

- LMS Energy – One of Australia’s largest methane abatement and bioenergy companies, partnering with more than 40 local councils and landfill owners to deliver methane abatement and renewable energy solutions.

- Solstice Energy – Partnered with Optimal Renewable Gas on the Westbury BioHub in Tasmania, designed to process 86,000–150,000 tonnes of organic waste annually and produce approximately 320 terajoules of biomethane.

Regional Analysis

Regional dynamics within the Australia biomethane market are shaped by feedstock availability, policy support, gas network infrastructure, and industrial energy demand.

- Australia Capital Territory & New South Wales is the largest region with a 34.7% share in 2025, driven by historic biomethane infrastructure projects, significant urban waste production, and strong government support for renewable gas projects throughout the Sydney metropolitan area. The Malabar Biomethane Injection Plant serves as a pioneering demonstration facility, while the NSW government’s $40 million Renewable Gas Production Program is accelerating biomethane project development across the state.

- Victoria is an emerging market, with the Gas Substitution Roadmap setting out a pathway for transitioning away from fossil gas use. The state is exploring policy options to incentivise biomethane and has recently proposed a renewable gas obligation. Victoria’s strong agricultural and food processing sectors provide abundant feedstock resources, and Delorean’s VIC1 Stanhope Bioenergy Plant is under development.

- Queensland is advancing biomethane capabilities, with vegetable grower Kalfresh securing an 80 million investment to build a bioenergy facility turning food waste and crop residues into biomethane as part of a larger 291 million Scenic Rim Agricultural Industrial Precinct.

- South Australia is a growing market, hosting Delorean’s SA1 bioenergy facility in Edinburgh Parks, which will inject mains‑grade biomethane into AGIG’s gas network. The project benefits from strong state‑level support for renewable energy and circular economy initiatives.

- Western Australia, Tasmania, and the Northern Territory represent emerging markets. Tasmania’s Westbury BioHub is under development, while the Northern Territory and Western Australia are beginning to assess biomethane potential from agricultural and municipal waste streams as policy frameworks evolve.

Recent Industry Developments

- March 2026: Optimal Renewable Gas was awarded a 20 million government grant under the NSW Low Carbon Product Manufacturing Grant programme to accelerate construction of the Griffith Biohub, a 58 million project converting agricultural waste into renewable biomethane.

- December 2025: The Westbury BioHub in Tasmania, a partnership between Optimal Renewable Gas and Solstice Energy, was announced with an election commitment of up to $12.5 million, designed to process 86,000–150,000 tonnes of organic waste annually and produce approximately 320 terajoules of biomethane.

- December 2025: Delorean Corporation announced its VIC1 Stanhope Bioenergy Plant, one of the first projects in Australia to produce mains‑grade biomethane from processed commercial and industrial organic waste, with Stage 1 processing up to 54,000 tonnes per annum for generation of 160 terajoules of biomethane.

- September 2025: Delorean Corporation secured a binding gas sales agreement with Origin Energy for the long‑term supply of renewable natural gas, with Origin purchasing up to 200 terajoules of biomethane per annum on a take‑or‑pay basis for eight years from expected first gas in April 2026.

- September 2025: Delorean Corporation’s NSW1 Brickworks Bioenergy Plant was announced as Australia’s first industrial‑scale bioenergy project to create Renewable Gas Behind the Meter for industrial manufacturing, with 120,000 tonnes per annum processing capacity producing approximately 253,000 gigajoules of biomethane annually.

- July 31, 2025: A new report released by Blunomy and Energy Networks Australia revealed that biomethane could meet up to 96% of current East Coast gas demand by tapping into existing waste streams, with approximately 400 petajoules of biomethane recoverable annually from existing feedstocks.

- July 31, 2025: Bioenergy Australia released its report “Unlocking Renewable Natural Gas to Enhance Energy Security and Maintain Australia’s Manufacturing Sector,” building the business case for biomethane to help decarbonise Australian industry.

- March 2025: Delorean Corporation signed a $6.08 million grant funding agreement with ARENA to enhance its SA1 bioenergy facility, enabling production of mains‑grade biomethane injected into AGIG’s gas network, with renewable gas supplied to industrial users through the Adelaide gas network.

- 2025: The Australian Government commenced consultation on expanding the Guarantee of Origin scheme to include biogas and biomethane, with a consultation period open until 27 April 2026, enabling producers to access domestic and international low‑emissions markets.

- 2025: The NSW Government announced the $40 million Renewable Gas Production Program to boost biomethane production, co‑funding up to 50% of project costs with eligible projects required to inject at least 0.1 petajoules of biomethane into the network each year by June 2030.

- 2024: The Australian Government’s Future Made in Australia initiative allocated $22.7 billion over the next decade to ARENA to support the commercialisation of low‑carbon fuels including biomethane, reinforcing the nation’s commitment to renewable gas development.

Browse Full Report with TOC & List of Figures for In‑Depth Market Insights: https://www.imarcgroup.com/australia-biomethane-market

Note: If you need any specific information that is not covered currently within the scope of the report, we will provide the same as a part of customisation.

About Us

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us

IMARC Group

134 N 4th St., Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No.: (D) +91 120 433 0800

United States: +1-201-971-6302

What's Your Reaction?