Australia Online Grocery Market Size, Share, Report 2026-2034

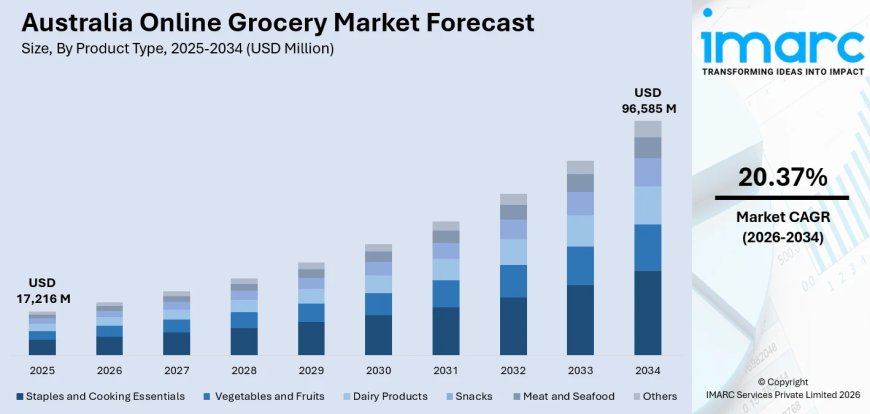

Australia online grocery market size stood at USD 17,216 Million in 2025 and is projected to hit USD 96,585 Million by 2034, advancing at a CAGR of 20.37% through 2026-2034.

Australia Online Grocery Market Overview

The Australia online grocery market is experiencing explosive growth, driven by massive fulfilment centre automation investments by major retailers, surging smartphone-based shopping adoption, expanding delivery speed and coverage, the integration of AI-powered personalisation and demand forecasting, and the permanent shift in consumer purchasing behaviour catalysed by the pandemic era. The Australia online grocery market size stood at USD 17,216 Million in 2025, reflecting the accelerating digital transformation of Australia’s grocery retail landscape. App-based platforms dominate with 62.4% of the market, driven by Australia’s smartphone penetration exceeding 95% of the population and 25.94 million internet users representing 96.7% of the population as of February 2026. Hybrid marketplace models command 47.2% of the market, led by Woolworths and Coles which anchor Australia’s omnichannel grocery ecosystems. Woolworths’ online food sales exceeded AUD 9.1 billion in FY2025, with its Everyday Rewards program boasting 10.2 million active members as of February 2025 — representing more than half of Australia’s adult population. Coles’ online sales surged 25.7% over the twelve months to March 2025, with Q1 FY26 online sales increasing 27.9% and penetration reaching 13.3%, while Woolworths’ online penetration reached 16.2%. Click-and-collect remains uniquely popular in Australia, accounting for approximately 40% of online sales at the top two retailers, reflecting consumer preference for flexibility and convenience. Australian food and beverages online spending reached AUD 13.6 billion in 2024, within a total online purchase market of AUD 69 billion.

Looking forward, the Australia online grocery market is projected to hit USD 96,585 Million by 2034, advancing at a CAGR of 20.37% through 2026-2034. This extraordinary growth trajectory is being supported by unprecedented infrastructure investment in automated customer fulfilment centres, the aggressive expansion of Amazon Fresh into the Australian market, the development of express delivery capabilities targeting sub-60-minute windows, and the deepening integration of AI across the entire online grocery value chain from demand prediction to last-mile delivery optimisation. Coles and Woolworths invested a combined AUD 200 million in automation between 2024 and 2025, enabling chilled-chain reliability within 2 hours. Coles commissioned its Witron-powered automated facility in Truganina, Victoria, in October 2024, unlocking capacity for tens of thousands of automated daily order picks, and launched a Perth express delivery pilot in February 2025 targeting 60-minute delivery. Woolworths’ Moorebank Customer Fulfilment Centre targets 60,000+ online orders per week, while the company opened a AUD 60 million fulfilment hub in Adelaide and announced the Heathwood CFC in Brisbane in May 2025 using Witron automation technology. Amazon Fresh extended to 47 additional Sydney suburbs in December 2024 and 80 more in January 2026, while Amazon announced a AUD 750 million Brisbane facility in March 2026 creating 1,000+ permanent jobs. In December 2025, Coles partnered with Uber Eats to expand 50%+ of Coles items for on-demand delivery. Amazon partnered with Harris Farm Markets to offer fresh local products through Amazon, with Harris Farm fulfilling orders from stores and Amazon Flex delivery partners handling last-mile delivery.

Request a Business Sample Report for Procurement & Investment Evaluation: https://www.imarcgroup.com/australia-online-grocery-market/requestsample

How AI is Reshaping the Future of the Australia Online Grocery Market

Artificial intelligence is fundamentally transforming Australia’s online grocery market, revolutionising demand forecasting, fulfilment automation, personalised shopping experiences, delivery route optimisation, and quality assurance. With the Australian AI in retail market generating USD 310.9 million in 2024 and projected to reach USD 1,990.6 million by 2030, and over 45% of retail SMEs already implementing AI solutions, the sector is undergoing rapid intelligent transformation. Key developments include:

• AI-Powered Demand Forecasting and Inventory Optimisation: Machine learning algorithms are transforming inventory management for online grocery operations by analysing historical purchase patterns, seasonal trends, weather data, promotional calendars, local events, and real-time demand signals to predict product demand with unprecedented accuracy at the store and fulfilment centre level. These AI systems enable Woolworths and Coles to optimise stock allocation across their customer fulfilment centres, reducing out-of-stock rates for online orders, minimising fresh food waste, and ensuring that the right products are available in the right quantities at the right fulfilment locations. The integration of AI-driven demand prediction with Witron automated picking systems at Coles’ Truganina facility and Woolworths’ expanding CFC network creates a powerful feedback loop where demand intelligence directly drives automated fulfilment efficiency.

• AI-Enabled Produce Quality Grading and Automated Fulfilment: Woolworths implemented an AI-enabled produce grading system at its Sydney fulfilment facility in March 2025, using computer vision and machine learning to automatically assess the quality, ripeness, and condition of fresh produce for home delivery orders. This technology ensures that online grocery customers receive produce that meets or exceeds the quality they would select in-store, addressing one of the primary barriers to online fresh food adoption. The system analyses visual characteristics including colour, shape, size, and surface condition to grade produce in real time as it moves through the automated fulfilment process, rejecting items that don’t meet quality thresholds and ensuring consistent customer satisfaction across thousands of daily orders.

• Hyper-Personalised Shopping Experiences and Recommendation Engines: AI-powered recommendation engines are transforming the online grocery shopping experience by analysing individual purchase history, dietary preferences, household composition, browsing behaviour, and seasonal patterns to deliver hyper-personalised product suggestions, meal planning assistance, and automated shopping list generation. Woolworths’ Everyday Rewards program — with 10.2 million active members — provides a vast dataset that AI systems leverage to personalise offers, predict repurchase timing, and recommend complementary products that increase basket size and customer satisfaction. These personalisation capabilities are particularly powerful in the subscription segment, where AI can predict when households need to replenish staple items and proactively suggest reorders at optimal intervals.

• AI-Optimised Last-Mile Delivery and Route Planning: Machine learning algorithms are optimising last-mile delivery operations — the most expensive component of online grocery fulfilment — by dynamically routing delivery vehicles based on real-time traffic conditions, delivery window preferences, vehicle capacity, temperature-sensitive product requirements, and geographic clustering of orders. Coles’ February 2025 Perth express delivery pilot targeting 60-minute delivery windows relies on AI-powered route optimisation to achieve rapid fulfilment within economically viable operating parameters. These systems continuously learn from delivery performance data to improve routing accuracy, reduce delivery times, and lower per-order delivery costs.

• AI-Driven Dynamic Pricing and Promotional Intelligence: AI-powered pricing engines are enabling Australian online grocery retailers to implement dynamic pricing strategies that optimise margins while maintaining competitive positioning across thousands of product lines. These systems analyse competitor pricing, demand elasticity, inventory levels, product shelf life, and promotional effectiveness to adjust prices in real time, maximising revenue while minimising waste on perishable items. AI-driven promotional intelligence tools identify the most effective promotional mechanics, optimal discount levels, and ideal timing for each customer segment, improving the return on promotional investment and driving incremental online order volume.

Australia Online Grocery Market Trends

Massive Automated Fulfilment Centre Investment Transforming Online Grocery Infrastructure

The unprecedented investment in automated customer fulfilment centres by Australia’s leading grocery retailers represents the most transformative infrastructure trend in the online grocery market, as Woolworths, Coles, and Amazon build the high-capacity, technology-enabled distribution networks required to serve rapidly growing online demand with improved speed, accuracy, and cost efficiency. Coles and Woolworths invested a combined AUD 200 million in automation between 2024 and 2025, enabling chilled-chain reliability within 2-hour delivery windows that match the temperature integrity requirements of fresh, chilled, and frozen grocery products. Coles commissioned its Witron-powered automated facility in Truganina, Victoria, in October 2024, unlocking capacity for tens of thousands of automated daily order picks at substantially reduced operational cost compared to manual store-based fulfilment. Woolworths’ Moorebank Customer Fulfilment Centre targets 60,000+ online orders per week, while the company opened a AUD 60 million fulfilment hub in Adelaide — joining its network of seven CFCs across all major eastern cities — and announced the Heathwood CFC in Brisbane in May 2025, also using Witron automation technology. Amazon’s announcement of a AUD 750 million Brisbane facility in March 2026 — spanning 150,000 square metres and creating 1,000+ permanent jobs — signals the intensifying infrastructure arms race between established Australian retailers and global competitors. This automated fulfilment investment is critical to achieving the unit economics necessary to sustain rapid online grocery growth, as automated picking systems deliver 3-5x the throughput of manual store-based fulfilment at lower error rates, enabling retailers to process the increasing order volumes projected in the market’s 20.37% CAGR growth trajectory.

Express Delivery, Quick Commerce, and On-Demand Grocery Partnerships Accelerating Consumer Adoption

The rapid development of express delivery capabilities, quick commerce models, and strategic partnerships between traditional grocery retailers and on-demand delivery platforms is fundamentally reshaping consumer expectations and accelerating adoption of online grocery shopping across Australia. Coles launched a Perth express delivery pilot in February 2025 targeting 60-minute delivery windows, demonstrating the shift from next-day and same-day delivery models toward sub-hour fulfilment that positions online grocery as a real-time shopping alternative rather than a planned-ahead convenience. In December 2025, Coles partnered with Uber Eats to expand availability of 50%+ of Coles items through on-demand delivery, creating a powerful distribution channel that leverages Uber’s existing delivery infrastructure and consumer app ecosystem. Amazon Fresh extended to 47 additional Sydney suburbs in December 2024 and 80 more in January 2026, progressively building the geographic coverage necessary to challenge incumbent retailers’ last-mile advantage, while Amazon’s partnership with Harris Farm Markets enables fresh local product delivery through Amazon’s platform with Harris Farm fulfilling orders from stores. One-time purchases represent 65.7% of the market, indicating significant growth potential for subscription models as express delivery capabilities reduce the need for advance planning and enable impulse and top-up online grocery shopping. Staples and cooking essentials represent 25.8% of the market by product type, with Coles pantry essentials showing the highest repeat transaction frequency — a pattern that supports the development of automated replenishment and subscription services. The convergence of rapid delivery, extensive product availability, competitive pricing, and seamless digital experiences is progressively eliminating the friction points that historically limited online grocery adoption, with Australian Capital Territory and New South Wales leading at 34.5% regional share driven by Sydney’s dense population, advanced delivery infrastructure, and the concentration of fulfilment centre investment in the greater Sydney metropolitan area.

Australia Online Grocery Market Summary

• The Australia online grocery market stood at USD 17,216 Million in 2025 and is projected to hit USD 96,585 Million by 2034 at a CAGR of 20.37%, driven by massive fulfilment centre automation, express delivery expansion, AI-powered personalisation, and permanent consumer behavioural shifts toward digital grocery shopping.

• Woolworths’ online food sales exceeded AUD 9.1 billion in FY2025 with 16.2% online penetration, while Coles’ online sales surged 27.9% in Q1 FY26 with 13.3% penetration, and click-and-collect accounts for approximately 40% of online sales at both retailers.

• Coles and Woolworths invested a combined AUD 200 million in fulfilment automation in 2024-2025, with Coles’ Witron-powered Truganina CFC (October 2024) and Woolworths’ AUD 60 million Adelaide hub and Heathwood Brisbane CFC (May 2025) expanding automated capacity.

• App-based platforms dominate at 62.4% market share with 95%+ smartphone penetration, while hybrid marketplace models command 47.2% and Woolworths’ Everyday Rewards program has 10.2 million active members — over half of Australia’s adult population.

• Amazon announced a AUD 750 million Brisbane facility (March 2026) creating 1,000+ jobs, expanded Amazon Fresh to 127+ additional Sydney suburbs, and partnered with Harris Farm Markets for fresh local product delivery, intensifying competition with incumbent retailers.

Australia Online Grocery Market Growth Drivers

Ultra-High Digital Connectivity and Smartphone Penetration Enabling Seamless Online Grocery Adoption

Australia’s exceptionally high levels of digital connectivity and smartphone penetration represent a fundamental enabler of online grocery market growth, providing the technological infrastructure and consumer digital fluency necessary for rapid adoption of app-based and web-based grocery shopping platforms. Australia has 25.94 million internet users representing 96.7% of the population as of February 2026, while smartphone penetration exceeds 95%, creating near-universal access to the mobile applications that dominate 62.4% of the online grocery market. Australian consumers spent AUD 69 billion on online purchases in 2024, with food and beverages accounting for AUD 13.6 billion, demonstrating the established digital commerce behaviour that online grocery platforms can build upon. The high smartphone penetration is particularly significant for the online grocery market because mobile apps enable features that drive adoption and repeat usage — including push notification alerts for delivery windows, real-time order tracking, barcode scanning for product reordering, digital shopping lists, and personalised promotional offers. Woolworths’ Everyday Rewards program — with 10.2 million active members as of February 2025 — exemplifies how digital loyalty ecosystems create powerful engagement loops that drive online grocery adoption, with AI-powered personalisation leveraging purchase data to deliver targeted offers and recommendations through mobile applications. The hybrid marketplace model commanding 47.2% of the market reflects how digital platforms enable retailers to extend their product range beyond traditional grocery through online marketplace partnerships, with Woolworths’ Everyday Market expanding available selection by end-2024. Australia’s advanced 4G and 5G mobile network infrastructure supports the bandwidth-intensive features of modern grocery apps — including high-resolution product imagery, video content, augmented reality, and real-time inventory availability — that enhance the online shopping experience and reduce barriers to adoption.

Intensifying Competitive Investment Creating Superior Consumer Propositions

The intensifying competitive investment among Woolworths, Coles, Amazon, and emerging players is creating a virtuous cycle of infrastructure development, service innovation, and consumer proposition improvement that is collectively accelerating online grocery market growth beyond what any single retailer could achieve independently. Woolworths and Coles’ combined AUD 200 million automation investment in 2024-2025 has enabled chilled-chain reliability within 2-hour delivery windows, addressing the quality and temperature integrity concerns that historically limited consumer willingness to purchase fresh, chilled, and frozen products online. Woolworths’ online food sales exceeding AUD 9.1 billion in FY2025 and Coles’ 27.9% online sales growth in Q1 FY26 demonstrate that this infrastructure investment is translating directly into consumer adoption and revenue growth. Amazon’s aggressive Australian expansion — extending Amazon Fresh to 127+ additional Sydney suburbs across 2024-2026, announcing a AUD 750 million Brisbane facility, and partnering with Harris Farm Markets for fresh local product delivery — is introducing competitive pressure that compels incumbent retailers to accelerate their own investment in delivery speed, product range, and pricing competitiveness. Coles’ December 2025 partnership with Uber Eats to expand 50%+ of its items for on-demand delivery, and its February 2025 Perth express delivery pilot targeting 60-minute windows, reflect the competitive imperative to match and exceed the delivery speed expectations being set by quick commerce entrants. This competitive dynamic is creating a market environment where service levels continuously improve, delivery windows shrink, product availability expands, and pricing remains competitive — all of which lower barriers to consumer adoption and drive the market’s extraordinary 20.37% CAGR growth trajectory. Woolworths achieving 100% renewable electricity by February 2026 and Amazon’s Melbourne sort centre receiving zero-carbon certification in March 2025 demonstrate that sustainability credentials are emerging as an additional competitive dimension as environmentally conscious consumers factor supply chain sustainability into their grocery purchasing decisions.

Australia Online Grocery Market Segments

The Australia online grocery market is comprehensively segmented across product type, business model, platform, purchase type, and region, providing a detailed framework for analysing growth opportunities and competitive dynamics across the digital grocery value chain.

• Breakup by Product Type: The market encompasses staples and cooking essentials (25.8% share), vegetables and fruits, dairy products, snacks, meat and seafood, and others. Staples and cooking essentials lead with the highest repeat transaction frequency, while fresh categories including vegetables, fruits, meat, and seafood are growing rapidly as AI-enabled produce grading and chilled-chain automation address quality concerns.

• Breakup by Business Model: The market includes hybrid marketplace (47.2% share), pure marketplace, and others. Hybrid marketplace models dominate as Woolworths and Coles leverage their physical store networks alongside dedicated customer fulfilment centres, while pure marketplace models are gaining traction through Amazon’s platform connecting consumers with specialty retailers like Harris Farm Markets.

• Breakup by Platform: The market is divided into app-based (62.4% share) and web-based platforms. App-based platforms dominate driven by Australia’s 95%+ smartphone penetration, with mobile apps enabling push notifications, real-time order tracking, barcode scanning, and personalised promotional offers that drive higher engagement and repeat purchase rates.

• Breakup by Purchase Type: The market encompasses one-time purchases (65.7% share) and subscription models. One-time purchases dominate reflecting the early-stage adoption of online grocery by many consumers, while subscription models present significant growth potential as express delivery capabilities and AI-powered automated replenishment reduce planning friction.

• Breakup by Region: The market is segmented across Australian Capital Territory & New South Wales (34.5% share), Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia. ACT & NSW leads driven by Sydney’s dense population, advanced delivery infrastructure, and the concentration of fulfilment centre investment including Woolworths’ Moorebank CFC and Amazon Fresh’s expanding suburban coverage.

Australia Online Grocery Market Competitive Landscape

The Australia online grocery market features a competitive landscape dominated by established supermarket chains expanding their digital capabilities alongside global e-commerce platforms and specialty grocery retailers. Key players operating in the market include Woolworths Group Limited, Coles Group Limited, Amazon Australia Pty Ltd, ALDI Australia, Metcash Limited (IGA, Foodland, Drakes), and Harris Farm Markets, among others. These companies compete through fulfilment centre automation, delivery speed and coverage, product range and freshness, pricing competitiveness, loyalty program engagement, app experience quality, and sustainability credentials to capture share in Australia’s rapidly expanding online grocery market.

Latest News & Development in the Australia Online Grocery Market

• May 2025: Woolworths announced the development of its Heathwood Customer Fulfilment Centre in Brisbane using Witron automation technology, expanding its network of automated CFCs, while having earlier opened a AUD 60 million fulfilment hub in Adelaide joining its network of seven CFCs across Australia.

• March 2025: Woolworths implemented an AI-enabled produce grading system at its Sydney fulfilment facility to support automated quality verification for home delivery orders, while Amazon’s Melbourne sort centre received zero-carbon certification, advancing sustainability in online grocery logistics.

• February 2025: Coles launched a Perth express delivery pilot targeting 60-minute delivery windows, demonstrating the shift toward sub-hour grocery fulfilment as the retailer continues to expand its online service capabilities across Australian cities.

• December 2024: Amazon Fresh extended to 47 additional Sydney suburbs, while Coles commissioned its Witron-powered automated facility in Truganina, Victoria, in October 2024, unlocking capacity for tens of thousands of automated daily order picks at substantially reduced operational cost.

• 2024-2025: Amazon partnered with Harris Farm Markets to offer fresh local products through its platform, with Harris Farm fulfilling orders from stores and Amazon Flex handling last-mile delivery, while Coles partnered with Uber Eats (December 2025) to expand 50%+ of Coles items for on-demand delivery.

Note: If you require any specific information not currently covered within the scope of the report, IMARC Group will provide it as part of customization.

Speak to an analyst:

https://www.imarcgroup.com/request?type=report&id=22049&flag=E

What's Your Reaction?