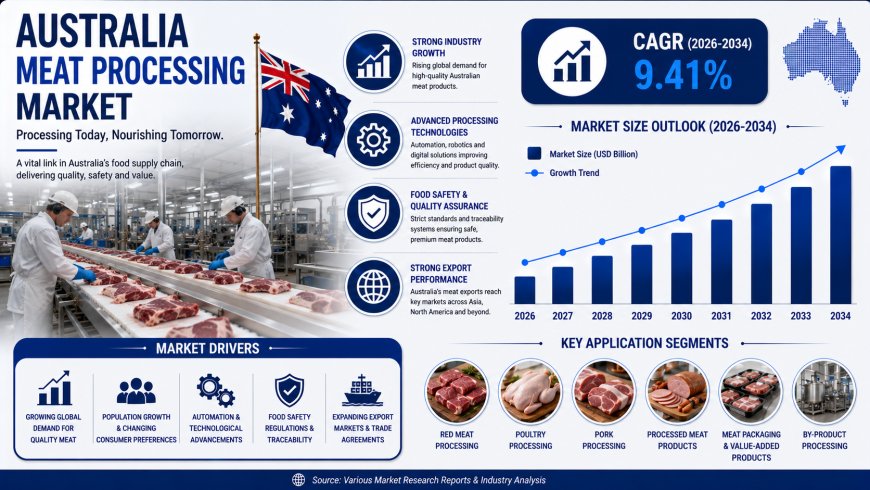

Australia Meat Processing Market Trends, Growth and Analysis Report 2026-2034

The Australia meat processing market size was valued at USD 500.18 Million in 2025 and is projected to reach USD 1,269.41 Million by 2034, growing at a compound annual growth rate of 9.41% from 2026-2034.

Market Overview

The Australia meat processing market is experiencing sustained growth, as domestic protein consumption increases and export demand strengthens across key international destinations. Rapid adoption of automation, technological innovations in processing equipment, and expanding cold chain infrastructure are enhancing operational efficiency and product quality across the supply chain. The market size reached USD 500.18 Million in 2025 and is projected to reach USD 1,269.41 Million by 2034, growing at a compound annual growth rate (CAGR) of 9.41% from 2026 to 2034.

Growing consumer preferences for convenient, minimally processed, and premium meat products are accelerating product diversification. The market is strategically important to Australia's economy as it supports a robust agricultural foundation, a resilient export ecosystem, and contributes significantly to rural and regional employment.

Request a Sample Report for In-Depth Market Insights: https://www.imarcgroup.com/australia-meat-processing-market/requestsample

Australia Meat Processing Market Summary

- The Australia meat processing market encompasses a system where meat products (raw cooked meat, precooked meat, fresh processed meat, raw fermented sausages, dried meat, and others) are processed using equipment (grinding, tenderizing, cutting, slicing, smoking, and others) for beef, pork, mutton, and other meats, across manual, semi-automatic, and automatic modes of operation.

- These meat processing products and services are valued for their role in providing convenient, minimally processed, and premium meat products to domestic and international consumers, enabling value-added product diversification and export growth.

- The ecosystem includes meat processors, equipment manufacturers, livestock producers, cold chain logistics providers, government agencies (food safety, trade), export partners, and consumers across Australian regions.

- Major segments identified in the market include product (fresh processed meat at 38.5%, raw cooked meat, precooked meat, raw fermented sausages, dried meat, others), equipment (cutting equipment at 32.5%, grinding, tenderizing, slicing, smoking, others), meat (beef at 42.5%, pork, mutton, others), mode of operation (automatic at 58.5%, manual, semi-automatic), and region (Australia Capital Territory & New South Wales at 32.5%, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia).

- The market is benefiting from rising domestic protein demand and shifting consumer preferences (high-protein diets, convenience-oriented purchasing), strong export demand and expanding global market access (2.24 million tons of red meat shipped to 104 nations in 2024), technological advancements and modernization of processing infrastructure (automation, robotics, AI-guided quality control), accelerating adoption of automation and robotics, and expansion of premium and value-added meat products (grass-fed, grain-fed, Wagyu, halal-certified, organic).

- According to the United States Department of Agriculture Foreign Agricultural Service, Australian beef production increased by 14% from 2023 levels in 2024, reaching near-record volumes.

PORTER'S FIVE FORCES ANALYSIS—AUSTRALIA MEAT PROCESSING MARKET

Bargaining Power of Suppliers—Moderate

- Meat processing suppliers include livestock producers, equipment manufacturers, and packaging material suppliers. Australia's vast cattle herd and diverse processing capacity provide consistent livestock supply. Feedlot capacity across Queensland and New South Wales supports consistent year-round supply.

- Cutting equipment leads at 32.5% market share, with advanced robotics and computer vision-guided cutting systems enabling high-throughput operations. Suppliers of specialized automation equipment have moderate bargaining power.

- However, the presence of multiple equipment manufacturers across different categories gives processors options, reducing dependency on any single supplier.

Bargaining Power of Buyers—Moderate to High

- Buyers include domestic retail chains, foodservice operators (QSRs, full-service dining), meal delivery platforms, and international export partners. The foodservice sector generates sustained wholesale demand for precisely portioned, hygienically processed meat inputs.

- In 2024, Australia shipped 2.24 million tons of red meat to 104 nations, indicating strong export buyer presence. Large international buyers have significant bargaining power due to volume purchasing.

- Processors are investing in halal-certified processing lines and blockchain-enabled traceability platforms to address nuanced preferences of export markets across Asia and the Middle East, responding to buyer requirements.

Threat of New Entrants—Moderate

- The meat processing market has moderate barriers to entry. Capital investment in processing facilities, automation equipment, and cold chain infrastructure is substantial. The Australian government has demonstrated sustained commitment to supporting food processing innovation.

- The extensive network of bilateral and multilateral free trade agreements covering key export destinations creates opportunities for new entrants with export capabilities.

- However, established processors have existing relationships with livestock producers, export partners, and retail customers, as well as scale advantages, creating barriers for unestablished entrants.

Threat of Substitutes—Moderate

- Plant-based protein alternatives are substitutes for meat products. The Australia health and wellness market is set to attain USD 205.8 Billion by 2034, indicating growing interest in alternative protein sources.

- However, Australia's global reputation for producing safe, high-quality, sustainably raised red meat gives processors a competitive premium reinforced by comprehensive food safety accreditation systems.

- The growing appetite for premium beef varieties (grass-fed, grain-fed, Wagyu) reflects a premiumization trend that plant-based substitutes cannot easily replicate.

Competitive Rivalry—Moderate to High

- The Australia meat processing market exhibits moderate-to-high concentration, with a small number of large, vertically integrated processors operating extensive multi-site facilities, alongside a broader base of regional and specialty processors.

- Competitive differentiation is increasingly driven by product quality, export accreditation, sustainability credentials, automation investment, and breadth of branded product portfolios.

- Leading processors are channeling profits from record export performance back into facility expansions, renewable energy integration, and workforce development programs.

MARKET GROWTH DRIVERS

Rising Domestic Protein Demand and Shifting Consumer Preferences

The sustained growth in domestic protein consumption constitutes a foundational driver of the Australia meat processing market. Australian consumers are increasingly adopting high-protein dietary frameworks driven by broader health, fitness, and wellness trends, which are elevating demand across a diverse spectrum of processed, minimally processed, and value-added meat products throughout retail, foodservice, and digital commerce channels.

The shift towards convenience-oriented purchasing is particularly significant, as the rapid growth of dual-income households, urbanization, and time-poor lifestyles accelerates demand for pre-seasoned, marinated, and ready-to-cook formats that deliver premium quality with minimal preparation burden. In 2024, in New South Wales, for couple families with dual incomes, the median income for families with children was USD 3,282, while for those without children, it was USD 2,954. Processors are responding by investing in flexible, multi-product lines capable of addressing the increasingly segmented consumer market.

Strong Export Demand and Expanding Global Market Access

The Australia meat processing sector is significantly propelled by robust and growing international demand, particularly from high-value markets in Asia, the Middle East, and North America. Australia's well-established global reputation for producing safe, high-quality, sustainably raised red meat gives its processors a competitive premium reinforced by comprehensive food safety accreditation systems and animal welfare standards recognized by importing nations.

In 2024, Australia shipped 2.24 Million Tons of red meat to 104 nations, marking the highest quantity of red meat exported to date. The extensive network of bilateral and multilateral free trade agreements covering key export destinations continues to reduce tariff barriers and streamline market access, enabling Australian processors to compete effectively against other major exporting nations.

Technological Advancements and Modernization of Processing Infrastructure

Technological innovations and infrastructure modernization represent a powerful structural growth driver for the Australia meat processing market. The accelerating deployment of automated processing systems, robotics, AI-guided quality control, and advanced packaging technologies is enabling processing facilities to achieve significant improvements in throughput efficiency, product consistency, and operational cost management.

These investments are particularly critical in an environment of rising labor costs and persistent workforce challenges in regional processing locations, where automation offers a sustainable pathway to maintaining and expanding production capacity. The Australian government has demonstrated sustained commitment to supporting food processing innovation, with approvals granted for major new facilities incorporating renewable energy systems and advanced processing technologies.

Accelerating Adoption of Automation and Robotics

The integration of automated robotics, artificial intelligence (AI), and machine vision systems across the Australia meat processing sector is reshaping facility operations and production capabilities. Processors are deploying robotic cutting, deboning, and packaging lines to address persistent labor shortages in regional areas, improve throughput consistency, and reduce reliance on physically demanding manual tasks.

These technologies enable precise, repeatable processing outcomes while enhancing hygiene compliance and food safety standards, contributing to Australia meat processing market growth in alignment with the increasing demands of export-oriented production. Automated cutting machines using machine learning (ML) algorithms and three-dimensional scanning capabilities can adjust to changes in animal size and carcass structure, greatly increasing production and accuracy.

Expansion of Premium and Value-Added Meat Products

Consumer demand for premium, specialty, and value-added meat products is intensifying across both domestic retail and export channels, creating new product development opportunities for Australian processors. The growing appetite for grass-fed, grain-fed, Wagyu, halal-certified, and organic varieties reflects a broader premiumization trend driven by health and wellness awareness, ethical sourcing preferences, and rising disposable incomes.

Processors are investing in advanced grading systems, blockchain-enabled traceability platforms, and halal-certified processing lines to address the nuanced preferences of export markets across Asia and the Middle East. Strong feedlot capacity across Queensland and New South Wales continues to support consistent year-round supply of high-quality grain-fed beef.

AUSTRALIA MEAT PROCESSING MARKET SEGMENTATION

- Product Insights:

- Fresh Processed Meat (38.5% share in 2025)

- Raw Cooked Meat

- Precooked Meat

- Raw Fermented Sausages

- Dried Meat

- Others

- Equipment Insights:

- Cutting Equipment (32.5% share in 2025)

- Grinding Equipment/Mincer

- Tenderizing Equipment

- Slicing Equipment

- Smoking Equipment

- Others

- Meat Insights:

- Beef (42.5% share in 2025)

- Pork

- Mutton

- Others

- Mode of Operation Insights:

- Automatic (58.5% share in 2025)

- Semi-Automatic

- Manual

- Regional Insights:

- Australia Capital Territory & New South Wales (32.5% share in 2025)

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

COMPETITIVE LANDSCAPE

The Australia meat processing market exhibits moderate-to-high concentration, with a small number of large, vertically integrated processors operating extensive multi-site facilities, alongside a broader base of regional and specialty processors. Competitive differentiation is increasingly driven by product quality, export accreditation, sustainability credentials, automation investment, and the breadth of branded product portfolios. Leading processors are channeling profits from record export performance back into facility expansions, renewable energy integration, and workforce development programs.

Strategic partnerships with international retail and foodservice buyers are strengthening long-term supply relationships, while investments in digital traceability and food safety systems are reinforcing export market credentials across premium destinations globally.

Key players mentioned in the report include major Australian meat processing companies. Notable industry data includes:

- 2024 Export Data: Australia shipped 2.24 Million Tons of red meat to 104 nations, marking the highest quantity of red meat exported to date.

- 2024 Production Data (USDA): Australian beef production increased by 14% from 2023 levels in 2024, reaching near-record volumes.

- 2024 Income Data (NSW): For couple families with dual incomes, the median income for families with children was USD 3,282, while for those without children, it was USD 2,954.

REGIONAL ANALYSIS

- Australia Capital Territory & New South Wales (32.5% share): This region constitutes the single largest regional market in Australia's meat processing industry, anchored by a concentration of major processing facilities, extensive logistics infrastructure, and proximity to Australia's largest domestic consumer markets. Sydney and surrounding metropolitan areas serve as critical distribution hubs for both domestic supply chains and export-oriented cold chain operations. Beef and sheep processing operations are particularly prominent. The Australian Capital Territory's proximity to key regulatory bodies provides favorable access to compliance support and export accreditation services.

- Victoria & Tasmania: Victoria is a significant meat processing region with strong processing infrastructure and access to export logistics. The region's agricultural hinterland supports consistent livestock supply. Tasmania's isolation and disease-free status provide advantages for certain export markets, supporting specialty and premium product processing.

- Queensland: Queensland is a major beef processing state with extensive feedlot capacity supporting consistent year-round supply of high-quality grain-fed beef. The state's processing facilities collectively handle significant daily throughput volumes across multiple product categories. Proximity to Asian export markets provides logistics advantages for international shipments.

- Northern Territory & Southern Australia: The Northern Territory supports live export and processing operations for Asian markets. South Australia has established meat processing facilities serving both domestic and export channels. The region's livestock production zones support processing operations across beef, lamb, and mutton categories.

- Western Australia: Western Australia's meat processing industry benefits from proximity to key Asian export markets. The state's livestock production zones (beef, sheep) support processing operations. Perth serves as a distribution hub for both domestic supply chains and export-oriented cold chain operations.

RECENT INDUSTRY DEVELOPMENTS

May 2026: Hewitt Group, Australia's largest certified organic producer, announced the acquisition of Nolan Meats, one of the country's leading beef processors. Nolan Meats employs more than 600 people and processes approximately 700 cattle per day, making the deal one of the most significant developments in the Australian meat processing industry this year.

May 2026: Premium beef producer King River expanded its global footprint, supplying Wagyu beef to 45 countries through 25 international distributors. The company reported annual production of approximately 3.2 million kilograms of beef, highlighting growing export opportunities for Australia's meat processing sector.

May 2026: Industry leaders warned that Australia is facing a shortage of accessible abattoirs, with more than two-thirds of small and medium livestock producers reportedly unable to access service-kill facilities. The issue threatens between A$564 million and A$742 million in annual farm revenue and has intensified calls for government support.

February 2026: A new industry report highlighted growing pressure on Australia's meat processing infrastructure, particularly in regional areas where producers face longer transport distances and reduced processing capacity following years of abattoir consolidation.

January 2026: JBS Australia confirmed the indefinite closure of its Seven Point Pork processing facility in South Australia, affecting approximately 270 jobs. The decision was linked to reduced customer orders and livestock supply constraints, underscoring ongoing challenges in the meat processing sector.

Note: If you need any specific information that is not covered currently within the scope of the report, we will provide the same as a part of customization.

Speak to an analyst: https://www.imarcgroup.com/request?type=report&id=36468&flag=C

About Us

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us

IMARC Group

134 N 4th St., Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 433 0800

United States: +1-201-971-6302

What's Your Reaction?