Australia Renewable Energy Market Size, Share, Report 2026-2034

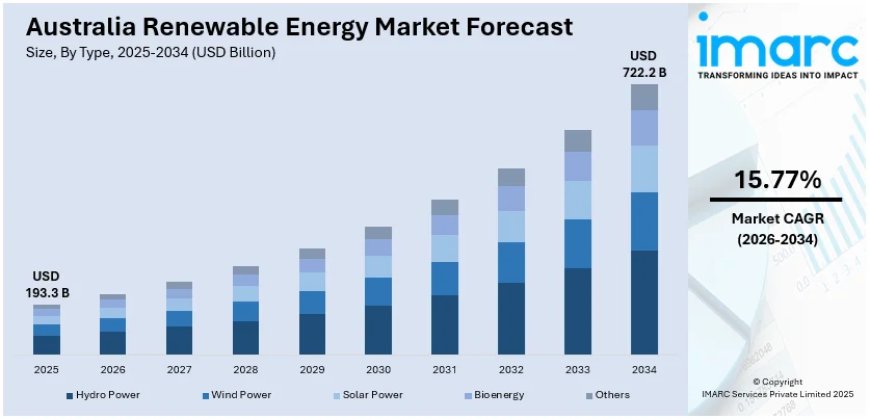

Australia renewable energy market size reached USD 193.3 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 722.2 Billion by 2034, exhibiting a growth rate (CAGR) of 15.77% during 2026-2034.

Australia Renewable Energy Market Overview

The Australia renewable energy market size reached USD 193.3 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 722.2 Billion by 2034, exhibiting a growth rate (CAGR) of 15.77% during 2026-2034. Australia's renewable energy sector is undergoing an unprecedented transformation, driven by ambitious government decarbonization targets, massive private investment inflows, and the rapid deployment of solar, wind, and battery storage infrastructure at scale. The country reached a landmark milestone in 2025, with renewables contributing over 50% of electricity generation on the national grid for the first time, underscoring the accelerating pace of Australia's energy transition.

The market is being further propelled by the emergence of green hydrogen as a transformative export opportunity, the explosive growth of battery energy storage systems, and surging corporate demand for renewable power purchase agreements (PPAs). Government policy frameworks—including the Renewable Energy Target, the Capacity Investment Scheme (CIS), and the Clean Energy Finance Corporation—provide the regulatory certainty and financial de-risking that underpin long-term private investment. With approximately 7 GW of new renewable capacity added in 2025 alone and over 12 GW in the construction or financial commitment pipeline, Australia is firmly on track toward its target of 82% renewable electricity by 2030.

How AI is Reshaping the Future of the Australia Renewable Energy Market

Artificial intelligence is rapidly becoming a cornerstone of Australia's renewable energy ecosystem, transforming how energy is generated, distributed, stored, and consumed. From predictive analytics for solar and wind output to autonomous grid management, AI is enabling the efficient integration of variable renewable sources at an unprecedented scale.

• AI-Enabled Smart Grid Optimization: AI-powered smart grid systems across Australian cities are using machine learning algorithms to monitor and optimize the real-time distribution of renewable energy. Queensland has achieved a 15% reduction in energy wastage through AI-enabled smart grids that automatically route excess solar and wind generation to battery storage during peak production and draw from stored energy during peak consumption, significantly improving grid reliability and efficiency.

• Predictive Maintenance and Asset Performance: AI-driven predictive maintenance platforms are being deployed across wind farms and large-scale solar installations to anticipate equipment failures, optimize maintenance schedules, and extend asset lifecycles. These systems analyze real-time sensor data, weather patterns, and historical performance metrics to reduce unplanned downtime by up to 30%, lowering operational costs and maximizing energy yield from renewable assets.

• AI-Powered Energy Forecasting: Advanced AI forecasting models are improving the accuracy of solar irradiance and wind speed predictions, enabling grid operators and energy traders to better anticipate renewable output fluctuations. These models integrate satellite imagery, atmospheric data, and machine learning to deliver forecasts with significantly reduced error margins, which is critical for balancing supply and demand in a grid increasingly dominated by intermittent renewable sources.

• Data Centre Renewable Integration: The Australian Government released its expectations for data centres and AI infrastructure developers in March 2026, mandating that AI data centres contribute to the energy transition by offsetting their energy requirements using renewable sources. Major technology firms are responding—Amazon's AUD 20 billion data centre investment includes over 170 MW of renewable capacity through power purchase agreements with utility-scale solar projects in Victoria and Queensland, creating a powerful demand-side pull for new renewable generation.

• AI-Driven Energy-as-a-Service Platforms: Smart energy technologies and AI-driven analytics are increasingly being integrated into Energy-as-a-Service (EaaS) platforms, offering enterprises real-time energy monitoring, predictive maintenance, and automated energy optimization solutions. Large enterprises and property developers are partnering with energy service providers to implement renewable-powered microgrids and AI-based energy efficiency platforms, driving the EaaS market toward USD 5.1 billion by 2034.

Request a Business Sample Report for Procurement & Investment Evaluation:

https://www.imarcgroup.com/australia-renewable-energy-market/requestsample

Australia Renewable Energy Market Trends

Explosive Growth in Battery Energy Storage Systems

Battery energy storage has emerged as one of the most dynamic segments of Australia's renewable energy market, with installations in 2025 reaching 1.9 GW and 4.9 GWh—exceeding the combined capacity deployed over the previous eight years. The national energy storage capacity reached 4.72 GW in 2025 and is projected to expand to 19.81 GW by 2034, growing at a CAGR of 17.28%. This surge is driven by the critical need to address the intermittency of solar and wind generation, provide grid stability services, and support the closure of aging coal-fired power stations. Large-scale battery projects—including community-scale batteries and utility-grade installations—are being deployed across New South Wales, Victoria, Queensland, and South Australia, supported by government incentives under the Capacity Investment Scheme and state-level energy storage targets. The declining cost trajectory of lithium-ion batteries, coupled with growing interest in alternative chemistries such as iron-air and vanadium flow batteries, is further accelerating deployment and improving the economic viability of renewable energy projects.

Green Hydrogen Emerging as a Transformative Export Opportunity

Green hydrogen is rapidly positioning itself as the most transformative long-term growth opportunity within Australia's renewable energy market, leveraging the country's world-class solar and wind resources to produce a storable, exportable clean fuel. Australia's National Hydrogen Strategy, supported by dedicated hydrogen hubs in regions such as the Pilbara, Gladstone, and the Hunter Valley, is attracting significant domestic and international investment in electrolyzer capacity and hydrogen export infrastructure. The strategic value of green hydrogen extends beyond domestic decarbonization—it positions Australia as a potential global clean energy superpower, with export agreements being developed with key trading partners including Japan, South Korea, and Germany. The convergence of falling electrolyzer costs, abundant renewable resources, and strong policy support is expected to make green hydrogen a commercially viable fuel source at scale during the forecast period, driving substantial incremental demand for solar and wind generation capacity.

Australia Renewable Energy Market Summary

The Australia renewable energy market is characterized by accelerating deployment, transformative policy support, and technological innovation across multiple energy sources and applications:

• The market was valued at USD 193.3 Billion in 2025 and is projected to reach USD 722.2 Billion by 2034, growing at a CAGR of 15.77% during 2026-2034.

• Approximately 7 GW of new renewable capacity was added in 2025, with over 12 GW in the construction or financial commitment pipeline, keeping Australia on track toward its 82% renewable electricity target by 2030.

• Battery energy storage installations surged to 1.9 GW and 4.9 GWh in 2025—exceeding the combined capacity of the previous eight years—with the storage market projected to reach 19.81 GW by 2034 at a CAGR of 17.28%.

• Green hydrogen is emerging as a transformative export opportunity, with Australia's world-class solar and wind resources, dedicated hydrogen hubs, and international export agreements positioning the country as a potential global clean energy superpower.

• AI-powered smart grids, predictive maintenance platforms, and energy forecasting models are driving operational efficiency gains, with Queensland achieving a 15% reduction in energy wastage through AI-enabled grid optimization systems.

Australia Renewable Energy Market Growth Drivers

Government Policy Frameworks and Investment Incentives

Australia's renewable energy market expansion is fundamentally underpinned by a comprehensive suite of government policies designed to accelerate the energy transition and de-risk private investment. The Capacity Investment Scheme (CIS) provides revenue underwriting for new dispatchable generation and storage projects, ensuring bankable returns for investors in wind, solar, and battery assets. The Clean Energy Finance Corporation (CEFC) continues to deploy concessional capital across renewable projects, while the Australian Renewable Energy Agency (ARENA) funds pre-commercial innovation in areas such as offshore wind, green hydrogen electrolysis, and next-generation battery technologies. State-level policies are equally aggressive—Victoria's legislated 95% renewable electricity target by 2035, New South Wales's Renewable Energy Zone (REZ) framework, and Queensland's 80% renewables target by 2035 are generating coordinated investment pipelines across the national electricity market. The scheduled closure of coal-fired power stations—with the majority expected to retire by the early 2030s—creates an urgent structural demand for replacement renewable capacity, providing long-term visibility for project developers and financiers.

Surging Corporate PPA Demand and Data Centre Renewable Requirements

Corporate demand for renewable energy through power purchase agreements (PPAs) has become a major growth driver, with organizations across sectors including technology, financial services, mining, and manufacturing securing long-term renewable electricity contracts to meet sustainability targets and hedge against volatile wholesale energy prices. This trend has been dramatically amplified by the data centre boom—Australia's emergence as a major hyperscale data centre market is creating enormous incremental demand for renewable generation. Amazon's AUD 20 billion data centre investment in 2025, which includes over 170 MW of solar PPA capacity across Victoria and Queensland, exemplifies this dynamic. The Australian Government's March 2026 policy expectations for data centres and AI infrastructure explicitly require these facilities to offset their energy requirements using renewables, with states agreeing that data centres should fully offset their consumption through solar, wind, and energy storage. This regulatory mandate, combined with voluntary corporate net-zero commitments, is creating a powerful and growing demand-side pull that will sustain renewable energy project development well through the forecast period.

Australia Renewable Energy Market Segmentation

The Australia renewable energy market report offers a comprehensive analysis across the following segments, providing detailed insights into market dynamics and growth trajectories:

Breakup by Energy Source: Solar Energy, Wind Energy, Hydropower, Bioenergy, Others

Solar energy dominates the market, reflecting Australia's exceptional solar irradiance levels and the rapid cost declines in photovoltaic technology. The country has one of the highest rooftop solar penetration rates globally, while utility-scale solar farms are expanding rapidly across Queensland, New South Wales, and Victoria. Wind energy represents the second-largest segment, with both onshore and emerging offshore wind projects contributing to the generation mix. Hydropower provides critical baseload and pumped storage capacity, with projects such as Snowy 2.0 expected to add significant dispatchable renewable generation.

Breakup by End Use: Residential, Commercial and Industrial, Utility-Scale

The utility-scale segment accounts for the largest market share, driven by large solar and wind farm developments supported by government capacity schemes and corporate PPAs. The residential segment maintains strong growth momentum, fueled by Australia's high rooftop solar adoption rate, declining battery costs, and expanding home energy management systems. The commercial and industrial segment is experiencing accelerating demand, as businesses pursue renewable energy procurement to meet corporate sustainability targets, reduce energy costs, and comply with emerging ESG reporting requirements.

Breakup by Technology: Photovoltaic (PV), Concentrated Solar Power (CSP), Onshore Wind, Offshore Wind, Others

Photovoltaic technology commands the dominant share, encompassing both rooftop and utility-scale installations. Onshore wind represents a mature and rapidly expanding segment, while offshore wind is emerging as a significant growth frontier following the passage of Australia's Offshore Electricity Infrastructure Act and the designation of priority development zones. Concentrated solar power retains a niche presence, primarily in research and demonstration contexts.

Breakup by Region: New South Wales, Victoria, Queensland, South Australia, Western Australia, Others (including ACT, Tasmania, Northern Territory)

Queensland leads the regional market, benefiting from exceptional solar resources, large-scale wind development, and the state's 80% renewable electricity target by 2035. New South Wales follows closely, anchored by its Renewable Energy Zone (REZ) framework and major infrastructure projects including the Snowy 2.0 pumped hydro scheme. Victoria's aggressive 95% renewables target by 2035 is driving significant offshore wind and battery storage investment. South Australia remains a global leader in variable renewable penetration, regularly achieving periods of 100% renewable generation, and serves as a testbed for advanced grid management and storage technologies.

Australia Renewable Energy Market Competitive Landscape

The Australia renewable energy market features a diverse competitive landscape comprising major utilities, independent power producers, global renewable energy developers, and emerging technology providers. Key players operating in the market include Origin Energy, AGL Energy, Goldwind Australia, Vestas, Canadian Solar, Trina Solar, Neoen, Acciona Energía, Iberdrola (Infigen Energy), ENGIE Australia, and Tesla Energy. These companies are competing across solar, wind, battery storage, and green hydrogen value chains, with strategies focused on securing long-term government contracts, expanding corporate PPA portfolios, investing in next-generation battery technologies, and developing integrated renewable energy hubs. The competitive landscape is further evolving as global hyperscale technology companies enter the market as major off-takers, driving demand for utility-scale renewable projects through large-scale power purchase agreements.

Australia Renewable Energy Market: Latest News and Developments

Recent developments shaping the Australia renewable energy market include:

• March 2026: The Australian Government released its formal expectations for data centres and AI infrastructure developers, requiring these facilities to contribute to the energy transition by fully offsetting energy requirements using renewable sources such as solar, wind, and energy storage, with the Australian Energy Market Commission asked to advise on implementation by July 2026.

• Late 2025: Australia set new records as nine wind and solar projects, along with 1 GW and 2.3 GWh of battery storage, were connected to the national grid in the final quarter of 2025, bringing total new renewable capacity for the year to approximately 7 GW and keeping the country on track for its 82% renewable electricity target by 2030.

• June 2025: Amazon announced an AUD 20 billion data centre investment in Australia, including the procurement of over 170 MW of renewable capacity through power purchase agreements with European Energy across three new utility-scale solar projects in Victoria and Queensland.

• 2025: Battery energy storage installations in Australia reached a record 1.9 GW and 4.9 GWh in 2025, surpassing the combined capacity deployed over the previous eight years, with total committed battery capacity in the pipeline reaching 13 GW and 34.7 GWh by year-end.

• 2025: Australia achieved a historic milestone as renewable energy sources contributed over 50% of total electricity generation on the national grid for the first time, driven by record rooftop solar installations, the commissioning of multiple large-scale wind and solar farms, and expanding battery storage capacity.

Note: If you require any specific information not currently covered within the scope of the report, IMARC Group will provide it as part of customization.

Speak to an analyst:

What's Your Reaction?