Australia Paper Napkins Market: Size, Share, Trends, Analysis, Growth & Forecast to 2026-2034

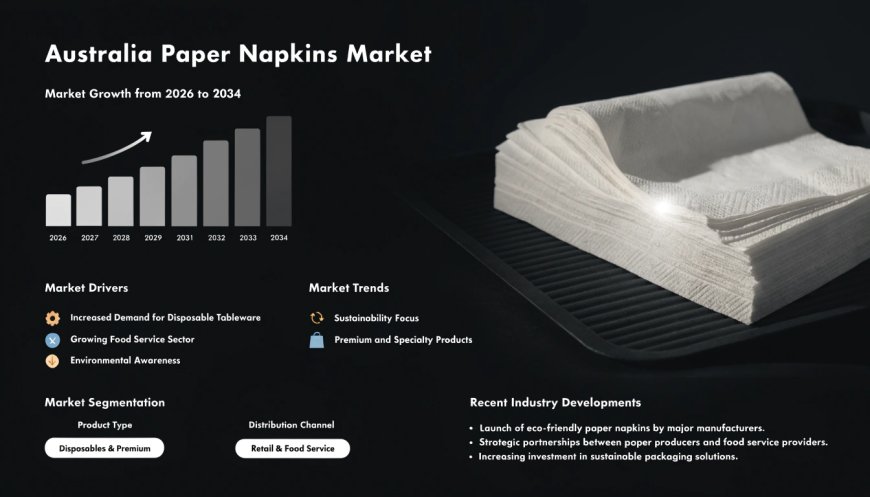

The Australia paper napkins market size reached USD 355.6 Million in 2025. Looking forward, IMARC Group expects the market to reach USD 676.7 Million by 2034, exhibiting a growth rate (CAGR) of 7.19% during 2026-2034

Market Overview

The Australia paper napkins market is expanding at a steady pace, driven by heightened hygiene awareness, a resurgence in dining-out culture, and rising demand for sustainable and biodegradable products. According to IMARC Group, the market size reached USD 355.6 Million in 2025 and is projected to reach USD 676.7 Million by 2034, exhibiting a compound annual growth rate (CAGR) of 7.19% during 2026‑2034. Growth in institutional consumption, particularly from healthcare and education sectors, is further boosting volume, while strong retail distribution and private label penetration continue to shape market share.

The market is strategically important to Australia's economy as it supports the nation's hygiene product manufacturing sector, caters to the growing hospitality and tourism industries, and aligns with the country's environmental goals through the adoption of eco‑friendly and recycled materials. As consumers and businesses increasingly prioritise sustainability, the paper napkins market is poised to benefit from the broader shift toward biodegradable and compostable disposable products.

The Australia paper napkins market is poised for sustained expansion, driven by a projected CAGR of 7.19% through 2034, a thriving tourism and outdoor event sector, and the rise of e‑commerce and subscription‑based hygiene product distribution. With the tourism sector projected to reach $345BN by 2034, and the wider tissue market valued at USD 2.13 billion in 2024, the market presents significant opportunities for manufacturers and retailers focused on sustainable materials, premium offerings, and innovative distribution channels.

Australia Paper Napkins Market Summary

The Australia paper napkins market encompasses a range of products including standard napkins, premium decorative napkins, and napkins for institutional use, available in various sizes, ply counts, and materials. The ecosystem includes international tissue paper conglomerates, domestic manufacturers, distributors, and retailers, serving end‑users across the food service sector (cafés, restaurants, hotels), institutional sector (healthcare, schools, offices), and household consumers.

The broader tissue paper market in Australia was valued at USD 2.13 billion in 2024 and is projected to reach USD 2.90 billion by 2030, registering a CAGR of 5.33%. Facial tissues and paper napkins are essential components aiding this expansion, widely used for personal grooming, hospitality services, and food‑related applications. The demand for high‑quality and attractively packaged napkin products is increasing, especially among premium hospitality venues and event organisers seeking to enhance guest experiences through superior service and presentation.

The market is driven by heightened hygiene awareness following the COVID‑19 pandemic, the strong rebound of Australia's tourism and hospitality sectors, increasing urbanisation, and rising disposable incomes. Consumers and businesses are shifting towards eco‑friendly and biodegradable paper napkins, aligning with broader environmental concerns and government recycling initiatives.

Porter's Five Forces Analysis – Australia Paper Napkins Market

The competitive dynamics of the Australia paper napkins market can be analysed using Porter's Five Forces framework.

Bargaining Power of Suppliers – Moderate

The market relies on a mix of domestic manufacturers and international suppliers for raw materials such as wood pulp and recycled fibres. Key global players like Kimberly-Clark, Essity, and Vinda International have established supply chains that provide them with significant leverage. However, the presence of multiple suppliers and Australia's Recycling Modernisation Fund (RMF) with a USD 0.64 billion commitment to strengthen domestic recycling infrastructure provide alternative sourcing options, helping to balance supplier power.

Bargaining Power of Buyers – High

Buyers include large‑scale hospitality chains, healthcare institutions, and retail consumers. The availability of products from multiple brands and distributors gives buyers extensive choice and strong negotiating power. The rise of e‑commerce and subscription‑based models has increased price transparency and ease of comparison, further strengthening buyer leverage. For premium hospitality venues and event organisers, however, quality and presentation can reduce price sensitivity, allowing suppliers to command premium pricing for value‑added products.

Threat of New Entrants – Moderate

Establishing a manufacturing facility for tissue and napkin products requires significant capital investment in machinery, raw material sourcing, and distribution networks. However, the growing demand for eco‑friendly and specialised napkin products is attracting new entrants focused on sustainable materials, decorative designs, and private label manufacturing. The market also sees opportunities for small and medium‑sized players through e‑commerce and niche product offerings.

Threat of Substitutes – Low

While reusable cloth napkins exist as an alternative, the convenience, hygiene, and disposability of paper napkins make them the preferred choice in food service, hospitality, and institutional settings. The pandemic has reinforced the demand for single‑use products in hygiene‑sensitive environments. For outdoor events and catering, where washing infrastructure is limited, paper napkins have no practical substitute.

Competitive Rivalry – Moderate

The market is moderately competitive, characterised by a mix of international tissue paper conglomerates and domestic manufacturers. In the sanitary paper product manufacturing industry, key players include Kimberly-Clark Pacific Holdings, ABC Tissue, and Essity Holding Australia. Domestic manufacturers are increasingly challenged by competitively priced imports from China, Indonesia, and Malaysia, which benefit from lower production costs. Competition centres on product quality, sustainability credentials, pricing, distribution reach, and branding, with premiumisation and product innovation being key differentiating strategies.

Request for Sample Report: https://www.imarcgroup.com/australia-paper-napkins-market/requestsample

Market Growth Drivers

Tourism Revival and Outdoor Event Catering

Australia's tourism and events sector has rebounded significantly, resulting in heightened demand for paper napkins in outdoor catering, festivals, and hospitality services. In 2024, Australia's tourism sector reached a record $265.5 billion, accounting for 10% of the national economy, while supporting 1.42 million jobs, a rise of nearly 10% from 2023. Domestic visitor spending is projected to climb to $148 billion, while international visitor spending, which jumped 195% to $31.6 billion in 2023, is forecast to reach $35 billion in 2024 and $52.5 billion by 2034. Looking ahead to 2034, the sector could surpass $345 billion in value and back 2 million jobs, representing 12% of total employment.

Disposable napkins are essential for hygiene and ease of service at temporary or large‑scale events where washing infrastructure is limited. With rising inbound tourism and domestic travel, cafes, food trucks, and pop‑up venues have expanded, all requiring high‑volume napkin supply. Manufacturers are introducing water‑resistant and durable napkin varieties tailored for outdoor use. This trend contributes materially to market growth by broadening seasonal and event‑based consumption cycles and introducing new avenues for product innovation and marketing.

E‑Commerce and Subscription‑Based Distribution

The digital transformation of retail in Australia has facilitated new sales channels for paper napkins through e‑commerce and subscription‑based models. Consumers now prefer direct‑to‑doorstep delivery of hygiene essentials, including tissue and napkin products. Subscription services offer convenience and ensure stock consistency for households and small businesses. In addition, online platforms provide wider product comparisons, eco‑label visibility, and customer reviews, enabling more informed and value‑driven purchasing decisions.

Australia's toilet, towel, and tissue paper market is projected to reach 767,000 tons and $1.6 billion by 2035, growing at a CAGR of 1.5% in volume and 2.5% in value from 2024. In 2024, consumption was 651,000 tons, a 5.6% increase from 2023, with a market value of $1.2 billion, up 9.5% year‑over‑year. E‑commerce is enabling brands to reach consumers directly, bypassing traditional retail channels and offering customised product bundles, subscription plans, and loyalty programmes that build recurring revenue streams and customer retention.

Rising Demand for Sustainable and Biodegradable Products

Increasing environmental awareness among Australian consumers is driving a shift toward eco‑friendly and biodegradable paper napkins. The government's Recycling Modernisation Fund (RMF), with a USD 0.64 billion commitment, aims to strengthen domestic recycling infrastructure, reduce waste exports, and support the use of recycled inputs in tissue production. In response, manufacturers are adopting green production methods, including alternative fibres and reduced resource consumption.

The shift toward eco‑friendly products, such as bamboo‑based and recycled tissues, is influencing purchasing behaviour. Consumers are increasingly choosing napkins made from recycled fibres or sustainably sourced pulp. Product innovations in embossing techniques, sheet size customisation, and improved roll length are helping enhance product efficiency and minimise waste, appealing to consumers who value functionality, sustainability, and cost‑effectiveness in their everyday purchases.

Premiumisation and Product Innovation

The tissue paper market in Australia is seeing strong consumer interest in premium products that offer improved comfort, strength, and skin compatibility. Innovations such as quilted textures, hypoallergenic tissues, and multi‑ply napkins have become increasingly common. In addition, consumers are seeking advanced product features, leading to the popularity of scented variants and designer prints. These enhancements not only address specific consumer needs but also support value‑based differentiation in a highly commoditised category.

The demand for high‑quality and attractively packaged napkin products is increasing, especially among premium hospitality venues and event organisers seeking to enhance guest experiences through superior service and presentation. Manufacturers are capitalising on these trends to command premium prices and strengthen brand positioning, contributing to overall market growth.

Market Growth Drivers

Institutional Consumption from Healthcare and Education Sectors

Healthcare and education sectors represent significant and stable demand channels for paper napkins. Hospitals, clinics, aged care facilities, schools, and universities require high‑volume supplies of disposable hygiene products to maintain cleanliness and prevent infection spread. These institutions rely on bulk purchasing and long‑term contracts with suppliers, creating stable demand for standardised, high‑capacity tissue products. The healthcare sector, in particular, relies on soft and sanitary tissues for patient care, while educational institutions continue to invest in touch‑free dispensing systems and premium tissue solutions to promote hygiene and well‑being.

Government Support for Domestic Manufacturing

The Australian government has demonstrated commitment to strengthening domestic manufacturing capabilities in the tissue and hygiene products sector. The Recycling Modernisation Fund (RMF) supports the use of recycled inputs, while initiatives promoting local production and reducing reliance on imports create favourable conditions for domestic manufacturers. However, domestic producers face challenges from competitively priced imports from lower‑cost countries, highlighting the need for continued policy support and innovation to maintain competitiveness.

Urbanisation and Rising Disposable Incomes

Australia's population growth, urbanisation, and rising disposable incomes are contributing to increased demand for convenient, disposable hygiene products. As consumers spend more time away from home—whether at restaurants, cafes, or events—the use of paper napkins in commercial settings continues to rise. Urban households also increasingly prefer disposable paper products for their convenience and hygiene benefits, supporting steady growth in the residential segment.

Australia Paper Napkins Market Segmentation

Segmentation analysis provides a detailed view of the Australia paper napkins market by category:

-

Product Type Insights: Standard Napkins, Premium Decorative Napkins, Institutional Napkins

-

Material Type Insights: Virgin Pulp, Recycled Fibre, Bamboo‑based

-

Application Insights: Food Service (Cafés, Restaurants, Hotels), Institutional (Healthcare, Education, Offices), Household

-

Distribution Channel Insights: Supermarkets and Hypermarkets, Convenience Stores, Online Stores, Food Service Distributors, Others

-

Regional Insights: Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia

Competitive Landscape

The competitive landscape of the Australia paper napkins market is characterised by a mix of international tissue paper conglomerates and domestic manufacturers. Key players compete on product quality, sustainability credentials, pricing, distribution reach, and branding. The market is also seeing increased activity in private label production, with retailers offering their own branded napkin products at competitive price points.

Key Companies Operating in the Market:

-

ABC Tissue Products Pty Ltd – The leading tissue paper product supplier in Australia, operating manufacturing facilities in Queensland and New South Wales with more than 600 employees. The company offers a comprehensive range of toilet tissues, facial tissues, kitchen towels, and napkins, serving both retail and commercial markets.

-

Kimberly-Clark Pacific Holdings – A major international player in the sanitary paper product manufacturing industry, with well‑known brands and extensive distribution networks across Australia.

-

Essity Holding Australia – A global hygiene and health company with significant market presence in Australia, offering a range of tissue products including napkins for both consumer and professional use.

-

Solaris Paper (Livi Paper) – An Australian operated and managed affiliate of APP, distributing high quality toilet and tissue paper products throughout the Australasia region. Livi offers a complete range of tissue finished products including napkins, with major Away From Home brands and private label capabilities.

-

Vinda International Holdings Limited – An international tissue paper manufacturer with a presence in the Australian market, offering premium tissue products.

-

Hospeco – A supplier of bulk paper products including napkins, hand towels, and toilet rolls, deliverable throughout Australia.

-

LX Enterprise Rolls – A Sydney‑based, Australian‑owned manufacturer of premium paper hygiene products using 100% virgin pulp, catering to commercial customers.

These companies compete on product quality, sustainability credentials, pricing, distribution reach, and branding. Manufacturers are increasingly adopting green production methods, including alternative fibres and reduced resource consumption, to meet the growing demand for eco‑friendly products. Private label penetration is also shaping the competitive landscape, as retailers offer their own branded napkin products at competitive price points.

Regional Analysis

Regional dynamics within the Australia paper napkins market are shaped by the concentration of economic activity, tourism, retail infrastructure, and population density across states and territories.

-

Australia Capital Territory & New South Wales is the largest market region, driven by Sydney's high concentration of hospitality venues, corporate offices, and tourism activity. The region benefits from extensive distribution networks and strong retail presence, serving both commercial and household consumers.

-

Victoria & Tasmania represents a significant market, with Melbourne's vibrant café culture, strong hospitality sector, and major events calendar driving demand for paper napkins. The region's growing tourism industry and active outdoor event scene further contribute to market growth.

-

Queensland is a growing market, supported by its thriving tourism industry, coastal events, and expanding population. The state's warm climate encourages outdoor dining, food trucks, and festivals, all of which require high‑volume napkin supply.

-

Western Australia sees steady demand, with Perth's growing hospitality sector and resource‑related corporate activity supporting the commercial segment. The region's isolation encourages local distribution networks and strong retail presence.

-

Northern Territory & Southern Australia are smaller markets but experience growth driven by tourism events and institutional demand from healthcare and education sectors. Seasonal peaks during tourist seasons create specific demand patterns for disposable napkin products.

Recent Industry Developments

-

May 2026: The Australian government announced additional funding for the Recycling Modernisation Fund (RMF) to strengthen domestic recycling infrastructure and support the use of recycled inputs in tissue production, directly benefiting the paper napkins market.

-

2025: The broader tissue paper market in Australia was valued at USD 2.13 billion, with napkins identified as a key growth segment due to rising demand from premium hospitality venues and event organisers.

-

2025: Major manufacturers, including ABC Tissue Products, expanded their product portfolios to include napkins made from recycled fibres and sustainably sourced pulp, responding to growing consumer demand for eco‑friendly options.

-

2025: E‑commerce platforms reported increased sales of paper napkins through subscription‑based models, with consumers opting for automatic delivery of household essentials, including napkins, to ensure stock consistency and convenience.

-

2025: The Australian tourism sector was projected to reach $265.5 billion in 2024, supporting 1.42 million jobs, with domestic visitor spending expected to climb to $148 billion, driving demand for napkins in outdoor catering, festivals, and hospitality services.

-

2025: Key industry players continued to invest in product innovation, including water‑resistant napkins for outdoor use and premium decorative napkins for events, broadening the range of applications and customer segments.

Browse Full Report with TOC & List of Figures for In‑Depth Market Insights: https://www.imarcgroup.com/australia-paper-napkins-market

Note: If you need any specific information that is not covered currently within the scope of the report, we will provide the same as a part of customisation.

About Us

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us

IMARC Group

134 N 4th St., Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No.: (D) +91 120 433 0800

United States: +1-201-971-6302

What's Your Reaction?