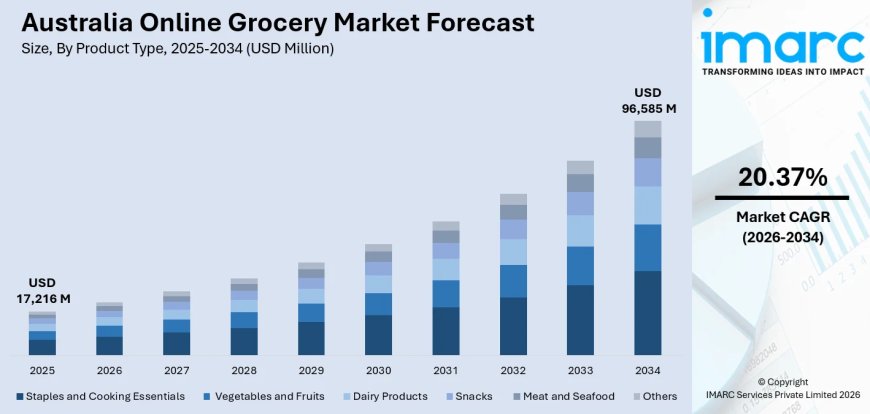

Australia Online Grocery Market 2026 | Worth USD 96,585 Million by 2034

Australia online grocery market size stood at USD 17,216 Million in 2025 and is projected to hit USD 96,585 Million by 2034, advancing at a CAGR of 20.37% through 2026-2034.

Market Overview

The Australia online grocery market is witnessing explosive growth driven by a predominantly mobile‑oriented consumer base, continued capital deployment into automated fulfilment infrastructure, and the broad‑based adoption of application‑driven grocery procurement. The market size stood at USD 17,216 Million in 2025 and is projected to reach USD 96,585 Million by 2034, advancing at a compound annual growth rate (CAGR) of 20.37% through 2026‑2034.

This market is strategically important to Australia’s retail and logistics economy, transforming the way Australian households manage their essential purchasing. Woolworths Group’s online food sales exceeded AU$ 9.1 billion in FY2025 alone, reflecting not merely the scale of digital channel growth, but the velocity at which consumer engagement is transitioning from physical retail environments to digital platforms. Mobile‑first grocery procurement has transitioned from an emerging trend to the established behavioural norm, with Australian consumers now holding clear expectations that their preferred supermarket application will retain their purchasing preferences.

The Australia online grocery market is poised for sustained expansion, driven by mobile‑first shopping behaviour, automated fulfilment investment, and hybrid marketplace models. With a projected CAGR of 20.37% through 2034, the market presents significant opportunities for retailers focusing on app integration, dark store expansion, and personalised promotional strategies.

AUSTRALIA ONLINE GROCERY MARKET SUMMARY

-

The Australia online grocery market encompasses the digital retail of food and grocery products through web‑based platforms and mobile applications, including pantry staples, fresh produce, dairy, meat, and household essentials.

-

The ecosystem spans supermarket chains (Woolworths, Coles), pure‑play online retailers, hybrid marketplace platforms, automated fulfilment centres, and last‑mile delivery networks.

-

Staples and cooking essentials account for 25.8% by product type in 2025, representing the category’s most enduring structural position within the channel, grounded in habitual replenishment behaviour.

-

Hybrid marketplace controls 47.2% of the business model in 2025, wherein first‑party inventory and third‑party seller listings coexist within a unified platform environment.

-

App‑based platforms own 62.4% of the platform segment in 2025, reflecting the depth of mobile integration within Australian consumer behaviour.

-

One‑time purchases account for 65.7% of purchase type in 2025, indicating most online grocery shoppers prefer independent, one‑off transactions rather than recurring subscription services.

-

Australia Capital Territory & New South Wales leads regionally at 34.5% in 2025, reflecting the compounding advantages conferred by Sydney’s population density and the concentration of automated fulfilment infrastructure.

PORTER'S FIVE FORCES ANALYSIS – AUSTRALIA ONLINE GROCERY MARKET

The competitive dynamics of the Australia online grocery market can be analysed using Porter's Five Forces framework.

Bargaining Power of Suppliers – Moderate

-

Online grocery platforms rely on suppliers of fresh produce, packaged goods, and household essentials. Major supermarket chains Woolworths and Coles maintain extensive supplier networks and negotiate volume‑based contracts, moderating supplier leverage. The rise of third‑party seller listings on hybrid marketplaces provides alternative sourcing channels.

Bargaining Power of Buyers – High

-

Australian consumers benefit from extensive choice across app‑based platforms, web‑based grocery sites, and hybrid marketplaces. The ability to compare prices, access personalised promotional content, and switch between platforms easily strengthens buyer negotiating power. With more than nine in ten Australians carrying smartphones, the accessibility of mobile grocery applications further empowers consumers.

Threat of New Entrants – Moderate

-

Significant capital requirements for automated fulfilment centres, delivery networks, and customer acquisition create barriers. However, the hybrid marketplace model, wherein first‑party and third‑party inventory coexist, has lowered entry barriers for niche grocery suppliers and online‑only retailers.

Threat of Substitutes – Low

-

Traditional brick‑and‑mortar grocery shopping represents a partial substitute, but the convenience, time savings, and personalised experience of online grocery procurement continue to drive channel shift. The prevalence of one‑time purchases underscores the importance of flexibility and convenience in the market.

Competitive Rivalry – High (Healthy)

-

The market features intense competition between Woolworths Group, Coles Group, and emerging online‑only players. Woolworths Group’s online food sales exceeded AU$ 9.1 billion in FY2025, reflecting the scale of digital channel growth. Competition is driven by delivery speed, app user experience, product range, and personalised promotional strategies.

Request for Sample Report: https://www.imarcgroup.com/australia-online-grocery-market/requestsample

MARKET GROWTH DRIVERS

Mobile‑First Grocery Procurement as the Established Norm

Mobile‑first grocery procurement has transitioned from an emerging trend to the established behavioural norm in Australia. What originally emerged as a pandemic‑era convenience measure has since crystallised into a permanent behavioural pattern. Australian consumers now hold clear expectations that their preferred supermarket application will retain their purchasing preferences, offer seamless reordering functionality, and provide personalised promotional content. App‑based platforms own 62.4% of the platform segment in 2025, reflecting the depth of mobile integration within Australian consumer behaviour.

Investment in Automated Fulfilment Infrastructure

Continued capital deployment into automated fulfilment infrastructure across Sydney and Melbourne is transforming the online grocery landscape. Woolworths now operates multiple Customer Fulfilment Centres across the country, while Coles has strengthened its online fulfilment capacity through partnership with Ocado. The margin relative to Victoria is progressively narrowing as Melbourne’s dark store network and Customer Fulfilment Centre development continues to advance. New South Wales maintains a structural lead, reflecting the compounding advantages conferred by Sydney’s population density and the concentration of automated fulfilment infrastructure within this region.

Hybrid Marketplace Model Driving Margin Diversification

Hybrid marketplace controls 47.2% of the business model in 2025, wherein first‑party inventory and third‑party seller listings coexist within a unified platform environment. This configuration affords consumers access to a broader product range, while enabling platform operators to achieve meaningful margin diversification – a structural advantage that pure‑play online models have consistently struggled to replicate at comparable scale. The hybrid model is particularly well‑suited to the Australian market, where consumer expectations for both convenience and product variety continue to rise.

AUSTRALIA ONLINE GROCERY MARKET SEGMENTATION

Segmentation analysis provides a detailed view of the Australia online grocery market by category:

-

Product Type Insights: Staples and Cooking Essentials (25.8% share in 2025), Fresh Produce, Dairy and Eggs, Meat and Seafood, Beverages, Household Essentials, Others.

-

Business Model Insights: Hybrid Marketplace (47.2% share), Pure‑Play Online, Supermarket‑Led.

-

Platform Insights: App‑Based (62.4% share), Web‑Based.

-

Purchase Type Insights: One‑Time (65.7% share), Subscription, Recurring.

-

Regional Insights: Australia Capital Territory & New South Wales (34.5% share), Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia.

COMPETITIVE LANDSCAPE

The competitive landscape of the Australia online grocery market is dominated by Woolworths Group and Coles Group, alongside emerging online‑only players and hybrid marketplace platforms. Woolworths Group’s online food sales exceeded AU$ 9.1 billion in FY2025 alone, reflecting the scale of digital channel growth. Coles has strengthened its online fulfilment capacity through partnership with Ocado, with central fulfilment centre catchments in Melbourne and Sydney now fully functional. The market research report provides a comprehensive analysis of the competitive landscape, including market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant, with detailed profiles of all major companies provided in the full report.

REGIONAL ANALYSIS

-

Australia Capital Territory & New South Wales leads regionally at 34.5% in 2025, reflecting the compounding advantages conferred by Sydney’s population density and the concentration of automated fulfilment infrastructure within this region.

-

Victoria & Tasmania is progressively narrowing the margin relative to New South Wales as Melbourne’s dark store network and Customer Fulfilment Centre development continues to advance.

-

Queensland sees growing online grocery demand driven by Brisbane’s expanding population and increasing mobile‑first shopping behaviour.

-

Western Australia experiences steady growth supported by Perth’s improving delivery infrastructure and rising consumer adoption of app‑based grocery platforms.

-

Northern Territory & Southern Australia, though smaller in market share, are benefiting from improved digital connectivity and the expansion of online grocery delivery networks.

RECENT INDUSTRY DEVELOPMENTS

-

2025 Activity: Woolworths Group’s online food sales exceeded AU$ 9.1 billion in FY2025, reflecting the scale of digital channel growth.

-

2025 Activity: Coles’ customer fulfilment centre partnership with Ocado continued to ramp up capacity, with Melbourne and Sydney CFC catchments expanded and same‑day CFC fulfilled delivery launched.

-

2025 Activity: App‑based grocery procurement continued to gain share, with more than nine in ten Australians carrying smartphones and supermarket applications offering personalised promotional content alongside streamlined reordering functionality.

Note: If you need any specific information that is not covered currently within the scope of the report, we will provide the same as a part of customization.

https://www.imarcgroup.com/request?type=report&id=22049&flag=C

ABOUT US

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

CONTACT US

IMARC Group

134 N 4th St., Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 433 0800

United States: +1 201 971 6302

What's Your Reaction?