Australia Legal Services Market Size, Share, Report 2026-2034

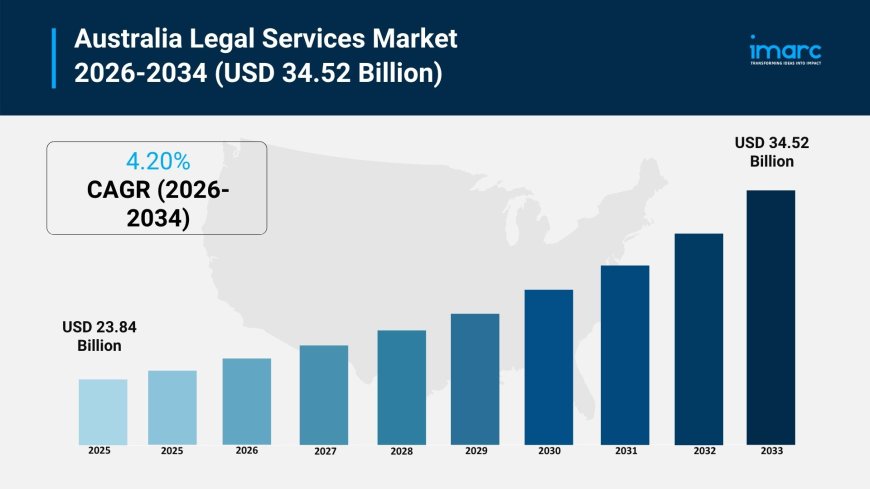

Australia legal services market was valued at USD 23.84 Billion in 2025 and is projected to reach USD 34.52 Billion by 2034, expanding at a CAGR of 4.20% during the forecast period (2026-2034).

Australia Legal Services Market Overview

The Australia legal services market is experiencing steady growth driven by increasing regulatory complexity, a rising volume of corporate transactions, growing demand for litigation and dispute resolution services, and the accelerating integration of technology across legal practice areas. According to IMARC Group, the Australia legal services market was valued at USD 23.84 Billion in 2025 and is projected to reach USD 34.52 Billion by 2034, expanding at a CAGR of 4.20% during the forecast period (2026-2034). The country's unique federal-state regulatory framework creates persistent demand for specialized legal counsel across multiple jurisdictions, while the growth of industries including clean energy, technology startups, and advanced agriculture is generating sophisticated commercial and regulatory challenges that require expert legal guidance.

The Australian legal landscape is undergoing a transformative period characterized by the rapid adoption of generative AI technologies, evolving client expectations around pricing and service delivery, and the emergence of new practice areas driven by ESG compliance, cybersecurity regulation, and digital economy expansion. A recent Thomson Reuters survey revealed that 65% of law firms have implemented either an AI strategy or responsible use policy, while in-house legal teams are even further ahead at 79%, signaling the industry's accelerating digital transformation. The market is experiencing a competitive dynamic between the prestigious Big 8 law firms, which have traditionally leveraged legacy brand strength and premium rate positioning, and rapidly rising large law firms that are beginning to outpace established players through innovation and operational agility. Meanwhile, the growing demand for cross-border legal services driven by Australia's trade relationships with Asia-Pacific economies, combined with expanding infrastructure investment, renewable energy development, and the increasing complexity of Indigenous heritage and land rights legislation, is creating a broad-based, multi-segment demand environment that supports sustained long-term growth across the legal services ecosystem.

How AI is Reshaping the Future of the Australia Legal Services Market

Artificial intelligence is fundamentally transforming the Australia legal services market, reshaping how law firms deliver services, manage operations, and engage with clients. Australian legal firms are at the forefront of global AI adoption, with 65% of law firms having implemented either an AI strategy or responsible use policy. Generative AI is now widely being used for research, drafting, and document review, tasks historically performed by junior and mid-level associates, signaling a structural shift in the traditional legal leverage model and driving a rethinking of service delivery, pricing, and professional development across the industry.

• AI-Powered Legal Research and Document Analysis: Advanced natural language processing and machine learning systems are transforming legal research by rapidly analyzing vast databases of case law, legislation, regulatory guidance, and legal commentary to identify relevant precedents, statutory interpretations, and risk factors. These AI platforms enable Australian lawyers to complete in hours what previously required days of manual research, dramatically improving throughput while enhancing the comprehensiveness and accuracy of legal analysis across litigation, corporate advisory, and regulatory compliance practice areas.

• Automated Contract Drafting and Review: AI-driven contract lifecycle management platforms are automating the drafting, review, and negotiation of legal agreements by identifying non-standard clauses, flagging risk provisions, and suggesting alternative language based on best-practice templates and historical deal data. These systems are accelerating transaction timelines for corporate, real estate, and commercial law practitioners while reducing the risk of human error in high-volume contract workflows, enabling law firms to handle increasing deal volumes without proportional increases in associate headcount.

• Predictive Litigation Analytics and Case Strategy: Machine learning algorithms are analyzing historical litigation outcomes, judicial decision patterns, and case characteristics to provide data-driven predictions on the likely success of legal arguments, estimated case duration, and probable settlement ranges. These predictive analytics tools are enabling Australian litigators to develop more informed case strategies, advise clients on risk-adjusted decision-making, and optimize resource allocation across complex dispute resolution matters involving commercial, employment, and regulatory disputes.

• AI-Enhanced Due Diligence and Compliance Monitoring: AI systems are revolutionizing due diligence processes in mergers and acquisitions, real estate transactions, and regulatory compliance by rapidly scanning and analyzing thousands of documents to identify material risks, regulatory breaches, and contractual obligations. These platforms significantly compress due diligence timelines while improving the thoroughness of risk identification, enabling corporate law teams to support the growing volume of M&A activity and cross-border transactions with greater speed and accuracy.

• Value-Based Pricing and Client Service Transformation: AI is catalyzing a fundamental shift in legal service pricing models, with 58% of in-house professionals surveyed believing that generative AI should be factored into law firm pricing. This is driving the transition from traditional billable-hour models toward value-based, fixed-fee, and subscription-based service delivery structures. AI-powered project management and matter analytics tools are enabling firms to price services more transparently, demonstrate measurable value to clients, and differentiate their offerings in an increasingly competitive market where technology-driven efficiency is becoming a baseline client expectation.

Request a Business Sample Report for Procurement & Investment Evaluation:

https://www.imarcgroup.com/australia-legal-services-market/requestsample

Australia Legal Services Market Trends

Rising Demand for ESG, Environmental, and Sustainability-Related Legal Advisory

One of the most significant trends reshaping the Australia legal services market is the rapidly growing demand for Environmental, Social, and Governance (ESG) advisory services. Australia's unique environmental challenges, combined with intensifying corporate accountability expectations and evolving regulatory frameworks, are driving law firms to develop specialized capabilities in climate transition planning, carbon offset structuring, environmental compliance, modern slavery reporting, and sustainability-linked financing. Companies undertaking development activities in ecologically sensitive regions such as the Murray-Darling Basin and mineral-rich areas of Western Australia face stringent environmental assessment requirements, necessitating expert legal guidance on sustainable planning, Indigenous land rights, and ecological impact assessments. The governance dimension is equally important, with increasing scrutiny of directors' fiduciary duties in relation to sustainability risks generating new advisory functions for legal professionals. As green investment, sustainability-linked bonds, and ESG-compliant corporate structures become mainstream, law firms with deep expertise in environmental regulation, social compliance, and governance frameworks are positioning themselves for sustained growth across corporate, infrastructure, and resource sector client bases.

Digital Economy Growth and Cybersecurity Regulation Creating New Practice Areas

The rapid expansion of Australia's digital economy is emerging as a transformative trend in the legal services market, creating entirely new practice areas and service demand across technology law, data privacy, fintech regulation, and cybersecurity compliance. With a thriving tech startup ecosystem fueled by government stimulus and venture capital, particularly within innovation precincts like Sydney's Tech Central and Melbourne's Cremorne Digital Hub, legal expertise in startup equity structuring, intellectual property protection, software-as-a-service agreements, and digital commerce regulation is in growing demand. Emerging privacy regulations and cybersecurity requirements specific to critical infrastructure, digital identity verification, and consumer data handling are creating rich opportunities for legal firms specializing in regulatory compliance and risk management. As Australia strengthens its national focus on digital resilience through enhanced cyber incident response planning, data breach notification requirements, and cross-border data transfer regulations, law firms with specialized capabilities in technology law and cybersecurity advisory are becoming essential partners for businesses navigating the increasingly complex digital regulatory landscape. The convergence of traditional legal expertise with technology-specific knowledge is creating a new generation of hybrid legal-tech professionals who serve both private and public sector clients across the country's expanding digital economy.

Australia Legal Services Market Summary

• The Australia legal services market was valued at USD 23.84 Billion in 2025 and is projected to reach USD 34.52 Billion by 2034, expanding at a CAGR of 4.20% during 2026-2034, driven by increasing regulatory complexity, rising corporate transaction volumes, growing ESG advisory demand, and the accelerating integration of AI and legal technology.

• The market is segmented by service into taxation, real estate, litigation, bankruptcy, labor/employment, and corporate categories, by firm size into large, medium, and small firms, and by provider into private practicing attorneys, legal business firms, government departments, and others, reflecting the diverse legal service requirements across Australia's economy.

• AI adoption is accelerating across the industry, with 65% of law firms having implemented an AI strategy or responsible use policy, while 58% of in-house professionals believe generative AI should be factored into law firm pricing, signaling a fundamental shift toward value-based service delivery models.

• Australia's trade relationships with Asia-Pacific economies, combined with CPTPP membership and growing cross-border investment activity, are generating strong demand for international law, trade policy, and multicultural client representation services, particularly in Sydney, Melbourne, and Brisbane.

• The competitive landscape features a dynamic between the prestigious Big 8 law firms leveraging legacy brand strength and premium rate positioning, and rapidly rising large law firms that are outpacing established players through innovation, technology integration, and operational agility.

Australia Legal Services Market Growth Drivers

Increasing Regulatory Complexity and Multi-Jurisdictional Compliance Demands

Australia's unique federal-state legal framework is serving as a foundational growth driver for the legal services market, creating persistent and expanding demand for specialized legal counsel across multiple jurisdictions. Companies operating in multiple states face varying licensing regulations, environmental permits, workplace health and safety laws, and consumer protection requirements, while federal regimes administered by bodies such as the Australian Competition and Consumer Commission, the Australian Prudential Regulation Authority, and national privacy regulators add additional compliance layers. Industry-specific legislation within mining, agriculture, finance, and telecommunications poses further area-specific challenges, with mining businesses in Western Australia navigating state land access laws, environmental impact approvals, and Native Title requirements, while employment arrangements across states must conform to Fair Work Commission standards. The emergence of new regulatory domains around data protection, digital economy governance, and critical infrastructure cybersecurity is compelling businesses to seek specialized legal guidance on cross-border data transfers, privacy impact assessments, and cyber incident response protocols. As regulatory enforcement intensifies and the penalties for non-compliance grow more severe, law firms are being engaged for proactive auditing, policy formulation, internal investigations, and dispute resolution across an increasingly complex compliance landscape.

Economic Diversification, Infrastructure Investment, and Cross-Border Transactions

Australia's ongoing economic diversification and massive infrastructure investment pipeline are serving as powerful catalysts for legal services demand across corporate, transactional, and advisory practice areas. New industries including clean energy, technology startups, and advanced agriculture are creating sophisticated commercial and regulatory challenges that require expert legal counsel on corporate structuring, joint ventures, mergers and acquisitions, intellectual property protection, and investment arrangements. In New South Wales and Victoria, the financial centers of Sydney and Melbourne are developing tech incubators and innovation precincts that generate demand for specialized legal advice on corporate governance, startup equity, and fintech regulation. Concurrently, increased infrastructure and renewable energy development across states like Queensland and South Australia requires expert legal guidance on environmental regulation compliance, project finance structuring, and procurement tendering. Australia's strong trade relationships with Asia-Pacific economies create additional demand for cross-border transaction expertise, with law firms helping multinational corporations navigate bilateral agreements, CPTPP provisions, and Foreign Investment Review Board procedures. As Chinese, Japanese, and Singaporean investment flows into Australian sectors including education, property, agriculture, and technology, legal advice on structuring transactions and ensuring regulatory compliance is becoming increasingly essential for business growth.

Australia Legal Services Market Segments

The Australia legal services market is segmented based on service, firm size, provider, and region, encompassing a comprehensive range of categories that reflect the diverse legal requirements across the national economy. Understanding these segments is essential for identifying growth opportunities, assessing competitive dynamics, and developing targeted strategies for market participants.

Breakup by Service:

• Taxation

• Real Estate

• Litigation

• Bankruptcy

• Labor/Employment

• Corporate

Corporate legal services are experiencing strong growth driven by the rising volume of mergers and acquisitions, cross-border transactions, and corporate restructuring activity, particularly in technology, healthcare, and financial services sectors. Litigation and dispute resolution services maintain consistent demand as commercial disputes, employment issues, and contract breaches drive an uptick in cases requiring expert legal representation or alternative dispute resolution strategies such as arbitration and mediation. Taxation services are expanding as evolving tax legislation and international tax compliance requirements create complexity for businesses operating across multiple jurisdictions. Real estate legal services benefit from Australia's active property development and conveyancing market. Labor and employment law is growing in importance due to evolving Fair Work Commission requirements and workplace health and safety regulations. Bankruptcy services serve a critical function during economic transitions and corporate restructuring cycles.

Breakup by Firm Size:

• Large Firms

• Medium Firms

• Small Firms

Large firms dominate high-value corporate, M&A, and cross-border transaction work, leveraging established litigation teams, multi-practice capabilities, and international network affiliations to serve major corporate clients, government entities, and institutional investors. The Big 8 law firms maintain premium positioning through legacy brand strength and deep expertise in complex regulatory matters. Medium firms are capturing growth through specialization in niche practice areas, regional expertise, and competitive pricing that appeals to mid-market corporate clients and growing enterprises. Small firms and sole practitioners serve essential roles in personal legal services including family law, estate planning, conveyancing, and migration assistance, with technology enabling broader geographic reach through virtual consultations and online service delivery.

Breakup by Provider:

• Private Practicing Attorneys

• Legal Business Firms

• Government Departments

• Others

Legal business firms represent the largest provider segment, encompassing full-service law firms that deliver comprehensive legal solutions across corporate, litigation, real estate, taxation, and regulatory compliance practice areas. Private practicing attorneys serve diverse client bases across personal, commercial, and specialized legal domains, with growing adoption of technology platforms enabling independent practitioners to compete effectively with larger firms. Government departments maintain substantial in-house legal capabilities for policy development, regulatory enforcement, and public sector legal advisory, with in-house teams at 79% AI strategy adoption leading the profession in technology integration. Other providers include community legal centers, non-profit legal aid organizations, and alternative legal service providers that are expanding access to justice for underserved populations across metropolitan and regional communities.

Breakup by Region:

• Australia Capital Territory & New South Wales

• Victoria & Tasmania

• Queensland

• Northern Territory & Southern Australia

• Western Australia

Australia Capital Territory & New South Wales leads the regional market, anchored by Sydney's position as Australia's premier financial and commercial center with the highest concentration of large law firms, corporate clients, and international legal service providers. Sydney's Tech Central innovation precinct generates growing demand for technology law, IP protection, and startup advisory services. Victoria & Tasmania benefit from Melbourne's Cremorne Digital Hub, extensive M&A activity, and strong demand for litigation and dispute resolution services. Queensland's legal market is supported by Brisbane and Perth's growing roles as multicultural professional services hubs, resource sector activity, and infrastructure development. Northern Territory & Southern Australia present specialized demand for mining, Indigenous heritage, and land rights legal services, with community legal centers providing essential access to justice in remote areas. Western Australia's legal market is driven by the mining and resources sector, requiring expertise in environmental compliance, Native Title, and project finance across the state's mineral-rich regions.

Competitive Landscape

The Australia legal services market features a dynamic competitive landscape characterized by the interplay between prestigious Big 8 law firms, rapidly rising large law firms, specialized boutique practices, and an emerging cohort of legal technology disruptors. The Big 8 firms, including firms such as King & Wood Mallesons, Allens, Herbert Smith Freehills, Clayton Utz, Ashurst, MinterEllison, and Corrs Chambers Westgarth, have traditionally dominated through legacy brand strength, premium rate positioning, and deep expertise in complex corporate and regulatory matters. However, rapidly rising large law firms are beginning to outpace established players through innovation, technology integration, and operational agility, creating a competitive bifurcation that is reshaping market dynamics. International law firms are expanding their Australian presence, attracted by the country's strong economic fundamentals and position as a gateway to Asia-Pacific markets. Legal technology companies such as Clio, which announced Australian expansion plans in January 2024, are introducing cloud-based practice management, AI-powered research, and automated workflow solutions that are transforming how firms of all sizes operate. Competitive differentiation increasingly centers on technology capabilities, ESG advisory expertise, cross-border transaction experience, and the ability to deliver transparent, value-based pricing models that meet evolving client expectations.

Latest News and Development

• In 2025, the Thomson Reuters Australia State of the Legal Market Report revealed a growing competitive split between the Big 8 law firms and rapidly rising large firms, with the latter outpacing established players through innovation and operational agility. The report highlighted that generative AI is reshaping the traditional leverage model as AI handles research, drafting, and document review tasks previously performed by junior associates.

• In 2025, a survey found that 58% of in-house legal professionals in Australia believe generative AI should be factored into law firm pricing, signaling an industry-wide transition toward value-based service delivery models. This shift is compelling law firms to rethink traditional billable-hour pricing and develop transparent, technology-enhanced service offerings.

• In 2024, a Thomson Reuters Tech, AI and the Law report found that 65% of Australian law firms have implemented an AI strategy or responsible use policy, while 79% of in-house legal teams have adopted AI governance frameworks, positioning Australia's legal sector among the global leaders in legal technology integration.

• In January 2024, Clio, a leading global legal technology company and developer of the world's first comprehensive legal operating system, announced plans to expand its footprint in Australia. The company is rapidly expanding its Australian team to enhance product development, sales, partnerships, and customer success, adapting its cloud-based practice management offerings to the unique needs of the Australian legal market.

• In 2024, Australian law firms continued to invest in innovation precincts and technology partnerships, with Sydney's Tech Central and Melbourne's Cremorne Digital Hub serving as focal points for legal-tech collaboration. Law firms increasingly embedded AI-powered research platforms, automated contract review tools, and predictive litigation analytics into their service delivery workflows, reflecting the sector's commitment to technology-driven transformation.

Note: If you require any specific information not currently covered within the scope of the report, IMARC Group will provide it as part of customization.

Speak to an analyst:

https://www.imarcgroup.com/request?type=report&id=24769&flag=E

What's Your Reaction?