Australia Energy Storage Market Size, Share, Growth & Forecast 2026-2034

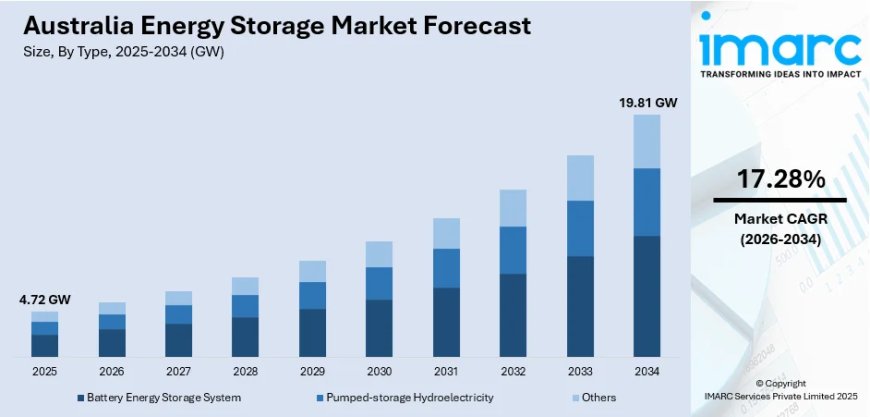

Australia energy storage market size reached 4.72 GW in 2025 and is projected to reach 19.81 GW by 2034, growing at a compound annual growth rate of 17.28% from 2026-2034.

Market Overview

The Australia energy storage market is undergoing a transformative expansion, driven by accelerating renewable energy integration, declining battery technology costs, supportive government incentives, and the critical need for grid stability as coal-fired generation retires across the National Electricity Market. According to IMARC Group, the market reached 4.72 GW in 2025 and is projected to reach 19.81 GW by 2034, exhibiting a CAGR of 17.28% during 2026-2034. Australia has emerged as the world's third-largest market for utility-scale battery energy storage by capacity, with 14 GW/37 GWh of battery storage at or nearing financial close and a development pipeline that surged 45 GW in twelve months to reach 154 GW, reflecting the extraordinary pace of investment and project commitment across the sector.

Key Market Summary

• Historical Market Size (2025): 4.72 GW

• Forecast Market Size (2034): 19.81 GW

• CAGR (2026-2034): 17.28%

• Largest Type Segment: Battery Energy Storage System (BESS) — 70.08%

• Largest End User Segment: Utility Scale — 50.12%

• Leading Region: Australian Capital Territory & New South Wales — 26%

• Segmentation Coverage: Type, End User, and Region

Key Sectors Driving Market Trends

Australia's energy storage market is being propelled by the urgent requirement to integrate record volumes of wind and solar generation into the national grid while maintaining system reliability as coal-fired power stations retire. Battery energy storage systems (BESS) account for 70.08% of the market, driven by rapid cost declines in lithium-ion battery technology, the codification of grid-forming inverter standards by AEMO, and the scaling of utility-scale projects from 2-hour to 4-hour and 8-hour duration configurations. The utility-scale segment holds 50.12% market share, with projects such as the 500 MW/1 GWh Liddell BESS and the AUD 1 billion Waratah Super Battery (850 MW/1.6 GWh) anchoring the pipeline.

The residential segment is experiencing equally dramatic growth, with household battery installations surging past 145,000 by end-2025, supported by the Australian Government's Cheaper Home Batteries Program launched on 1 July 2025. The Clean Energy Regulator forecasts up to 12 GWh of residential storage from 350,000 to 520,000 installations in 2026. Commercial and industrial storage is also gaining traction as businesses seek to optimise behind-the-meter solar self-consumption, manage demand charges, and participate in virtual power plant aggregation schemes.

Environmental Impact and Sustainability

Energy storage is playing a foundational role in Australia's clean energy transition, enabling the displacement of fossil fuel generation and reducing greenhouse gas emissions across the National Electricity Market. Grid-scale battery storage systems have offset 30 petajoules of gas use since deployment began, with 8.1 petajoules reduced in just four months leading up to early 2026. Battery storage projects now claim 46% of Australia's record 64 GW energy development investment pipeline, reflecting the central position of storage in the decarbonisation pathway.

The sustainability profile of the energy storage sector is further strengthened by the growth of pumped-storage hydroelectricity, with AEMO's Draft 2026 Integrated System Plan projecting 12 GW of pumped storage as essential long-duration storage infrastructure alongside 32 GW of grid-scale batteries. Community battery programs are also expanding, with 244 community battery systems now connected across Australia, supporting localised renewable energy sharing and reducing grid congestion at the distribution level.

Regulatory Framework

The Australia energy storage market operates within a comprehensive regulatory framework administered by the Australian Energy Market Operator (AEMO), the Australian Energy Market Commission (AEMC), and the Australian Energy Regulator (AER). AEMO's Draft 2026 Integrated System Plan (ISP) projects grid-scale BESS reaching 24 GW by 2030, an increase of approximately 9 GW over previous forecasts, and codifies grid-forming inverter technology as a cornerstone of system strength, with 10 grid-forming BESS sites currently operational in the NEM and a pipeline of 94 projects.

The Cheaper Home Batteries Program, launched on 1 July 2025, is transitioning to a tiered rebate structure from May 2026, with incentives calibrated by battery capacity to balance adoption acceleration with fiscal sustainability. The Clean Energy Regulator (CER) administers the Renewable Energy Target and related certificate schemes, while state-level programs in Victoria, New South Wales, Queensland, and South Australia provide additional rebates and feed-in tariffs that support residential and commercial storage deployment.

Request a Business Sample Report for Procurement & Investment Evaluation:

https://www.imarcgroup.com/australia-energy-storage-market/requestsample

Market Segments

Breakup by Type:

• Battery Energy Storage System (BESS) — 70.08% market share (largest)

• Pumped-Storage Hydroelectricity (PSH)

• Others

Breakup by End User:

• Utility Scale — 50.12% market share (largest)

• Commercial and Industrial

• Residential

Breakup by Region:

• Australian Capital Territory and New South Wales — 26% market share (largest)

• Victoria and Tasmania

• Queensland

• Northern Territory and South Australia

• Western Australia

Economic Costs and Benefits

The energy storage market is generating substantial economic contribution across Australia, with over AUD 2.4 billion invested in large-scale BESS projects in a single quarter in early 2025, the second-highest quarterly investment on record. These investments are creating employment across battery manufacturing, electrical engineering, construction, commissioning, and grid operations, while catalysing demand for local supply chains in switchgear, power electronics, thermal management systems, and civil infrastructure.

On the cost side, high initial capital investment, grid connection complexity and lead times, supply chain constraints for lithium-ion cells and critical minerals, and the regulatory burden of AEMO registration and compliance represent material challenges. However, declining battery cell prices, improving round-trip efficiencies, and the growing revenue stack available from wholesale energy arbitrage, frequency control ancillary services (FCAS), and capacity mechanisms are strengthening the investment case and delivering increasingly attractive returns across utility, commercial, and residential segments.

Competitive Landscape

The Australia energy storage market features a dynamic mix of international technology providers and domestic energy infrastructure developers. Neoen energised its 270 MW/540 MWh Western Downs BESS Stage 2 project six weeks ahead of schedule in September 2025, reinforcing its position as a leading clean energy developer. Akaysha Energy is constructing a 4 GWh portfolio of BESS in Australia, including the AUD 1 billion Waratah Super Battery (850 MW/1.6 GWh), with a further 13 GWh in its development pipeline. AGL Energy commissioned the 500 MW/1 GWh Liddell BESS in Q4 2025. The Melbourne Renewable Energy Hub (600 MW/1.6 GWh) progressed through commissioning across its A1, A2, and A3 stages. Quinbrook Infrastructure Partners advanced the 260 MW/620 MWh Supernode in Queensland. Recurrent Energy secured AEMO approval for its 600 MWh Sundown Energy Park solar-plus-BESS hybrid. Key technology suppliers including Tesla, Wartsila, and Fluence are competing actively to supply grid-scale battery systems across the NEM and WEM.

Real-World Applications

• Grid-Scale Renewable Firming: Utility-scale BESS projects are storing excess solar and wind generation during peak production hours and discharging during evening demand peaks, enabling higher renewable penetration without compromising grid reliability.

• Frequency Control and System Strength: Grid-forming battery systems are providing essential frequency control ancillary services (FCAS), synthetic inertia, and voltage support as synchronous coal generators retire across the NEM.

• Residential Solar Self-Consumption: Household battery systems are enabling homeowners to store rooftop solar generation for evening use, reducing grid dependence and lowering electricity bills under time-of-use tariff structures.

• Community Battery Programs: 244 community battery systems are now connected across Australia, enabling localised renewable energy sharing, reducing distribution network congestion, and providing shared storage benefits to apartment dwellers and renters.

• Long-Duration Storage: Australia's first 8-hour battery storage system has been registered with AEMO, alongside pumped hydro projects targeting multi-day storage to manage extended periods of low wind and solar output.

Latest News and Developments

• Q4 2025: A total 1,060 MW/2,520 MWh of new grid-scale battery capacity came online, including the 500 MW/1 GWh Liddell BESS in NSW and the 260 MW/620 MWh Supernode in Queensland, marking a landmark period for energy storage deployment.

• September 2025: Neoen energised its 270 MW/540 MWh Western Downs BESS Stage 2 project six weeks ahead of schedule in Queensland.

• October 2025: Australia became the world's third-largest utility battery market by capacity, with 14 GW/37 GWh at or nearing financial close and a development pipeline reaching 154 GW.

• 2026: AEMO released its Draft 2026 Integrated System Plan, projecting grid-scale BESS reaching 24 GW by 2030 and confirming 12 GW of pumped storage as essential long-duration infrastructure.

• April 2026: The Australian Government's expanded battery subsidies under the Cheaper Home Batteries Program are driving a surge in residential storage demand, with the Clean Energy Regulator forecasting up to 12 GWh from 350,000-520,000 installations in 2026.

Future Opportunities

Looking ahead, the Australia energy storage market is expected to benefit from the continued scaling of grid-scale BESS to 24 GW by 2030, the maturation of long-duration energy storage technologies including iron-air and flow batteries, the completion of major pumped hydro projects such as Snowy 2.0, and the deepening integration of virtual power plant platforms that aggregate residential and commercial batteries into grid-dispatchable resources. The codification of grid-forming inverter standards, the expansion of community battery programs, and the growing revenue diversification across energy arbitrage, FCAS, and capacity mechanisms are anticipated to accelerate investment and deployment through the 2026-2034 forecast horizon.

Note: If you require any specific information not currently covered within the scope of the report, IMARC Group will provide it as part of customization.

Speak to an analyst:

https://www.imarcgroup.com/request?type=report&id=24686&flag=E

About Us

IMARC Group is a leading market research company that offers management strategy and market research worldwide. We partner with clients in all sectors and regions to identify their highest-value opportunities, address their most critical challenges, and transform their businesses.

IMARC's information products include major market, scientific, economic and technological developments for business leaders in pharmaceutical, industrial, and high technology organizations. Market forecasts and industry analysis for biotechnology, advanced materials, pharmaceuticals, food and beverage, travel and tourism, nanotechnology and novel processing methods are at the top of the company's expertise.

Contact Us

IMARC Group

134 N 4th St., Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 433 0800

United States: +1-201971-6302

What's Your Reaction?