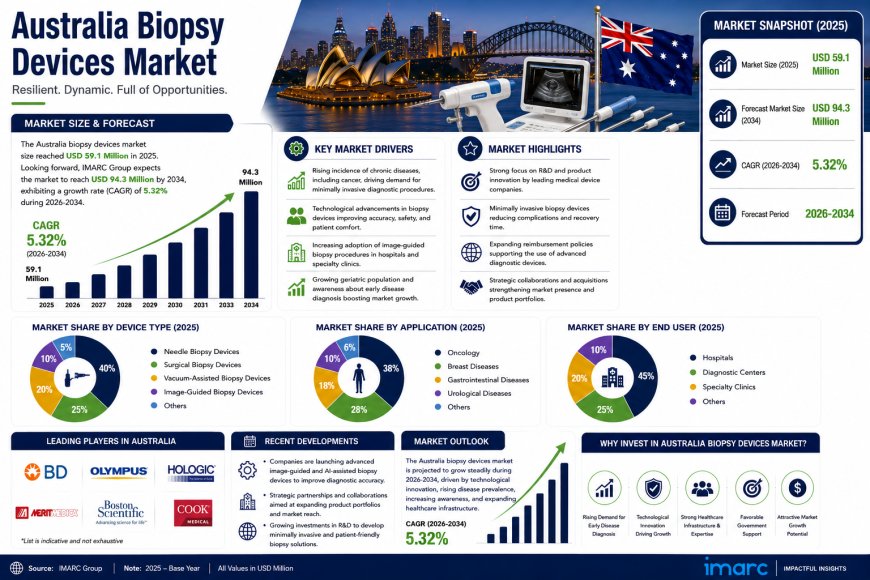

Australia Biopsy Devices Market Size, Share, Trends & Forecast 2026-2034

The market size was valued at USD 59.1 Million in 2025 and is projected to reach USD 94.3 Million by 2034, exhibiting a compound annual growth rate (CAGR) of 5.32% during 2026-2034.

Market Overview

The Australia biopsy devices market is witnessing robust growth propelled by rising cancer incidence rates; the successful launch of the National Lung Cancer Screening Program (NLCSP); ongoing expansion of national breast, bowel, and cervical cancer screening programs; and continuous technological advancements in minimally invasive and image-guided biopsy procedures. The market size was valued at USD 59.1 Million in 2025 and is projected to reach USD 94.3 Million by 2034, exhibiting a compound annual growth rate (CAGR) of 5.32% during 2026-2034. This growth is being supported by nearly 170,000 new cancer cases diagnosed in Australia in 2025, representing an approximately 93% increase over 25 years, according to the Australian Institute of Health and Welfare (AIHW).

Request for a Sample Report:

https://www.imarcgroup.com/australia-biopsy-devices-market/requestsample

Porter's Five Forces Analysis — Australia Biopsy Devices Market

The Australia biopsy devices market, valued at USD 59.1 Million in 2025 and projected to reach USD 94.3 Million by 2034 at a CAGR of 5.32%, reflects a structurally sound and technologically advanced industry environment with strong growth fundamentals driven by increasing cancer prevalence and the adoption of precision diagnostic techniques.

Bargaining Power of Suppliers — Moderate

- The global biopsy devices market features established multinational medical device manufacturers including Becton Dickinson and Co., Boston Scientific, Hologic, Medtronic, Olympus, and Cook Medical, creating a concentrated but competitively balanced upstream supply for biopsy device manufacturing.

- Key raw materials including medical-grade plastics, stainless steel, precision components, and advanced imaging sensors are sourced globally, with major suppliers maintaining diversified supply chains that moderate individual product dependency.

- The Australian market benefits from direct presence of leading manufacturers such as Hologic Australia offering comprehensive breast biopsy solutions including the Brevera and Eviva systems, Boston Scientific providing pulmonary and gastrointestinal biopsy devices, and BD offering advanced vacuum-assisted breast biopsy platforms.

Bargaining Power of Buyers — Moderate to High

- The Australian healthcare system, dominated by public hospitals and diagnostic networks, represents a concentrated buyer segment with significant purchasing volume. Public hospital networks across New South Wales, Victoria, Queensland, and Western Australia collectively negotiate procurement contracts that provide substantial leverage over device pricing.

- Private hospital groups, diagnostic imaging centres, and pathology laboratories increasingly demand premium biopsy devices with integrated image-guidance and automation capabilities, driving market differentiation and quality competition.

- The Medical Services Advisory Committee (MSAC) and Medicare Benefits Schedule (MBS) reimbursement framework influences adoption patterns, with government-funded screening programs including BreastScreen Australia and the National Bowel Cancer Screening Program creating structured demand that enhances buyer coordination.

Threat of New Entrants — Low to Moderate

- The biopsy devices market requires significant regulatory expertise to navigate the Therapeutic Goods Administration (TGA) approval process, clinical validation, and quality management systems, creating meaningful barriers for new market entrants.

- Established players benefit from decades of clinical evidence, physician training programs, and entrenched hospital procurement relationships. For example, Hologic's Affirm Prone Breast Biopsy System remains the world's first dedicated prone biopsy system capable of both stereotactic and tomosynthesis-guided procedures, representing significant technological and market positioning advantages.

- However, emerging Australian medtech companies are demonstrating innovative entry pathways. Diag-Nose.io received ARTG registration for its ABEL Microsampler nasal liquid biopsy device in March 2025, while Optiscan Imaging unveiled its real-time digital pathology device.

Threat of Substitutes — Low

- Tissue biopsy remains the gold standard for definitive cancer diagnosis, with no equivalent substitute capable of providing the same histological and molecular information required for treatment planning. The global liquid biopsy market is growing at a CAGR of 13.9% in Australia as a complementary tool for early detection and monitoring rather than a replacement for tissue biopsy.

- Emerging non-invasive diagnostic technologies, including circulating tumor DNA (ctDNA) assays and multi-cancer early detection blood tests, are expanding the diagnostic landscape. The Australia Multi-cancer Early Detection Market is expected to grow at a CAGR of 16.9% from 2025 to 2030, but these technologies serve as screening adjuncts rather than direct substitutes for confirmatory tissue biopsy.

- The superiority of core needle biopsy and vacuum-assisted biopsy for obtaining diagnostic-quality tissue samples, particularly in breast, lung, and prostate cancer diagnosis, ensures continued demand for traditional and advanced biopsy devices.

Competitive Rivalry — Moderate

- The Australia biopsy devices market features a competitive landscape dominated by leading global medical device manufacturers. Key players include Becton Dickinson and Co. (market leader in biopsy devices), Boston Scientific Corporation (pulmonary and gastrointestinal biopsy systems), Hologic, Inc. (comprehensive breast biopsy solutions), Medtronic plc (bronchial and bone biopsy devices), Olympus Corporation (gastrointestinal biopsy forceps and fine needle biopsy devices), Cook Medical (prostate and renal biopsy devices), and Argon Medical Devices, among others.

- Competitive intensity is intensifying through technological innovation in robotic bronchoscopy, AI-driven imaging guidance, and vacuum-assisted biopsy platforms. Companies compete on biopsy accuracy, sample quality, procedure time, patient comfort, and integration with imaging modalities.

- The Australian market also features strategic partnerships and distribution agreements, with ParagonCare serving as the exclusive distribution partner for Body Vision Medical's LungVision AI-driven advanced imaging system in Australia.

Market Trends

National Lung Cancer Screening Program Driving Biopsy Volumes

The launch of the National Lung Cancer Screening Program (NLCSP) on 1 July 2025 represents a transformative trend driving biopsy device demand in Australia. The program, a free government initiative designed to detect lung cancer in people most at risk before symptoms appear, has demonstrated exceptional early uptake. As of World Cancer Day in February 2026, more than 60,000 people had enrolled in the National Cancer Screening Register, with over 56,500 scans completed and more than 700 people referred immediately for further assessment. This landmark screening initiative is creating substantial downstream demand for bronchoscopic and percutaneous biopsy procedures, particularly for lung nodules detected through low-dose CT screening. The program's expansion to include remote and underserved regions, with Heart of Australia delivering first lung cancer screening clinics in the Kimberley in late 2025 and planned expansion to the Northern Territory and Queensland in 2026, further broadens the addressable market for biopsy devices across geographically diverse healthcare settings.

Robotic Bronchoscopy and AI-Driven Biopsy Technologies

The rapid adoption of robotic bronchoscopy systems is revolutionising lung cancer diagnosis in Australia. The Ion robotic bronchoscope, built in Brisbane, has been deployed at Epworth Eastern Hospital in Victoria — the first private hospital in Australia to adopt this next-generation technology. The system's built-in navigation technology allows respiratory specialists to access nodules that are often inaccessible using conventional approaches, enabling biopsy of peripheral lung lesions that were previously unreachable. Concurrently, Sir Charles Gairdner Hospital in Western Australia achieved a 100-patient milestone with its robotic bronchoscope, a multimillion-dollar system that helps clinicians diagnose and remove small cancerous nodules in the peripheral lung where conventional biopsy tools face limitations. Beyond robotics, Body Vision Medical received TGA regulatory approval for its LungVision AI-driven advanced imaging system in Australia in early 2025, with ParagonCare serving as the exclusive distribution partner. LungVision provides real-time navigation and enhanced visualisation to help physicians perform bronchoscopic biopsies with greater precision, improving early lung cancer diagnosis.

Market Summary

- The Australia biopsy devices market is projected to grow from USD 59.1 Million in 2025 to USD 94.3 Million by 2034 at a 5.32% CAGR, driven by rising cancer incidence, national screening program expansion, and technological advancements in biopsy devices.

- Nearly 170,000 new cancer cases were diagnosed in Australia in 2025, representing an increase of around 93% over 25 years, according to AIHW, creating sustained demand for tissue biopsy for diagnostic confirmation and treatment planning.

- The National Lung Cancer Screening Program launched on 1 July 2025 has enrolled over 60,000 people and completed more than 56,500 scans within its first seven months, generating substantial downstream biopsy procedure volumes.

- Robotic bronchoscopy adoption is accelerating, with the Ion robotic bronchoscope deployed at Epworth Eastern Hospital (first private hospital in Australia) and Sir Charles Gairdner Hospital achieving a 100-patient milestone with its robotic bronchoscopy program.

- TGA regulatory approvals are expanding the market, including Body Vision Medical's LungVision AI-driven imaging system, Cirdan's CoreLite breast biopsy imaging system, and Diag-Nose.io's ABEL Microsampler nasal liquid biopsy device.

Market Growth Drivers

Rising Cancer Incidence and National Screening Program Expansion

Australia's escalating cancer burden is a primary growth driver for the biopsy devices market. According to AIHW, nearly 1 million Australians had been diagnosed with cancer within the last 10 years as of 2025, including 518,000 males and 452,000 females. The total number of new cancer cases diagnosed in Australia in 2025 was estimated at nearly 170,000, representing an increase of approximately 93% over 25 years, with the majority of the increase due to population growth and an ageing population. This rising incidence is directly correlated with increased demand for biopsy procedures for diagnostic confirmation, molecular profiling, and treatment guidance.

Australia's national cancer screening framework provides structured demand for biopsy devices across four key programs: BreastScreen Australia (free breast cancer screening for women aged 50-74), National Bowel Cancer Screening Program (free home testing kits for eligible Australians aged 45-74, extended from 1 July 2024 to include people aged 45-49), National Cervical Screening Program (free screening every five years for women aged 25-74), and the newly launched National Lung Cancer Screening Program (free low-dose CT screening for at-risk individuals launched July 2025). Each of these programs generates positive screening results requiring confirmatory biopsy, creating substantial and sustained demand for core needle biopsy, vacuum-assisted biopsy, fine needle aspiration, and image-guided biopsy devices across public and private healthcare settings.

Technological Advancements in Minimally Invasive and Precision Biopsy

Continuous technological innovation is expanding the addressable market for biopsy devices by enabling safer, more accurate, and less invasive diagnostic procedures. Robotic bronchoscopy systems, including the Ion robotic bronchoscope deployed in Australian hospitals, are enabling biopsy of peripheral lung nodules previously considered unreachable with conventional techniques. AI-driven imaging guidance systems, such as Body Vision Medical's LungVision receiving TGA approval in Australia, provide real-time navigation and enhanced visualisation to improve biopsy accuracy and reduce procedure time. Vacuum-assisted breast biopsy systems, including Hologic's ATEC Sapphire console and Eviva system, enable minimally invasive breast biopsy across multiple modalities including ultrasound, MRI, stereotactic 2D, and 3D image guidance, offering patients less invasive alternatives to surgical biopsy. Advanced biopsy forceps and fine needle biopsy devices, including Olympus's SecureFlex single-use fine needle biopsy device launched in October 2025 for endoscopic ultrasound-guided fine needle biopsy (EUS-FNB) of gastrointestinal lesions, enhance diagnostic yield for pancreatic and gastrointestinal cancers.

Market Segments

By Product Type

- Biopsy Needles (Core Needle Biopsy, Fine Needle Aspiration, Vacuum-Assisted Biopsy)

- Biopsy Guns

- Biopsy Forceps

- Biopsy Guidance Systems (Ultrasound-Guided, MRI-Guided, CT-Guided, Stereotactic)

- Biopsy Site Markers

- Others

By Imaging Modality

- Ultrasound-Guided Biopsy

- MRI-Guided Biopsy

- CT-Guided Biopsy

- Stereotactic-Guided Biopsy

- Others

By Procedure Type

- Needle-Based Biopsy (Core Needle Biopsy, Fine Needle Aspiration)

- Vacuum-Assisted Biopsy

- Surgical Biopsy (Incisional, Excisional)

- Others

By Application

- Breast Cancer Biopsy

- Lung Cancer Biopsy

- Prostate Cancer Biopsy

- Gastrointestinal Cancer Biopsy

- Gynecological Cancer Biopsy

- Others (Liver, Kidney, Pancreatic, Bone Biopsy)

By End User

- Hospitals and Diagnostic Imaging Centres

- Ambulatory Surgical Centres

- Pathology and Research Laboratories

- Academic and Research Institutes

By Region

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Competitive Landscape

The Australia biopsy devices market features a competitive landscape dominated by multinational medical device manufacturers with strong local distribution networks, regulatory expertise, and clinical training capabilities. Key players operating in the market include:

- Becton Dickinson and Company (BD): Market leader in Australia biopsy devices, offering comprehensive biopsy platforms including the EnCor EnCompass next-generation multi-modality vacuum-assisted breast biopsy console compatible with stereotactic, MRI, and ultrasound imaging.

- Boston Scientific Corporation: Leading provider of pulmonary and gastrointestinal biopsy devices, including the Radial Jaw 4 Pulmonary Biopsy Forceps, iNod Ultrasound Guidance System, and SpyGlass DS System for ERCP-guided biopsies.

- Hologic, Inc.: Dominant player in breast biopsy solutions, offering the Brevera Breast Biopsy System with real-time imaging and automated post-biopsy specimen handling, Affirm Prone and Upright Breast Biopsy Systems, Eviva Breast Biopsy System, and ATEC Sapphire vacuum-assisted biopsy console.

- Medtronic plc: Provider of advanced biopsy technologies including the Stealth Autoguide for robotically assisted biopsy alignment, SharkCore FNB biopsy system for fine-needle biopsy procedures, and ILLUMISITE solution for safer lung biopsy.

- Olympus Corporation: Leading provider of gastrointestinal biopsy devices, including SecureFlex single-use fine needle biopsy device for EUS-FNB, comprehensive biopsy forceps range, and AI-assisted diagnostic technologies for bowel cancer detection.

- Cook Medical: Provider of reusable biopsy systems including the Cook Bx Biopsy Device for prostate and renal histological core biopsies.

- Other Key Players: Argon Medical Devices, Merit Medical Systems, Cardinal Health, Conmed Corporation, Integra LifeSciences, Teleflex, and emerging Australian medtech companies including Diag-Nose.io (nasal liquid biopsy) and Optiscan Imaging (real-time digital pathology).

Latest Recent News & Development

April 2026: The NSW Minns Labor Government announced $7.5 million in research grants under the five-year Translational Program Grants to reduce toxic side effects of radiotherapy and invasive biopsies, including a world-first AI-powered cancer research project and a project to replace invasive tissue biopsies with a simple blood test.

January 2026: Paragon Care Limited (ASX:PGC) acquired Fisher Biotec Pty Ltd for AUD 3.2 million on January 30, 2026, strengthening its position in the Australian medical device distribution landscape including biopsy and diagnostic equipment.

October 2025: Olympus launched SecureFlex, a single-use fine needle biopsy device designed for endoscopic ultrasound-guided fine needle biopsy (EUS-FNB) of submucosal and extramural lesions within the gastrointestinal tract, enhancing diagnostic accuracy for gastrointestinal and pancreatic diseases.

September 2025: Epworth Eastern Hospital became the first private hospital in Victoria, and the first private hospital in Australia, to introduce the Ion robotic bronchoscope, coinciding with the national rollout of the National Lung Cancer Screening Program. The system uses built-in navigation technology to reach previously inaccessible peripheral lung nodules.

July 2025: The Australian Government launched the National Lung Cancer Screening Program (NLCSP) on 1 July 2025, a free initiative to detect lung cancer in people most at risk before symptoms appear, representing Australia's fourth national cancer screening program.

August 2025: Cirdan received TGA approval for its CoreLite and Solas OR x-ray imaging systems for breast core biopsy procedures, reinforcing the company's growing presence in the Australian healthcare market.

Browse Full Report with TOC & List of Figures:

https://www.imarcgroup.com/australia-biopsy-devices-market/toc

About Us

IMARC Group is a global management consulting firm that helps companies in making business strategies. We have been serving the market research industry for over a decade, and have a strong client base of over 5,000+ companies across various industries. Our market research reports cover over 3,000+ markets, and we offer a wide range of services, including market research, competitive intelligence, and business strategy consulting. Our reports are based on a combination of primary and secondary research, and we use various data analysis tools and techniques to provide accurate and relevant insights.

Contact Us

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 433 0800

United States: +1-631-791-1145

What's Your Reaction?