Australia Battery Recycling Market | Size, Share and Analysis 2026-2034

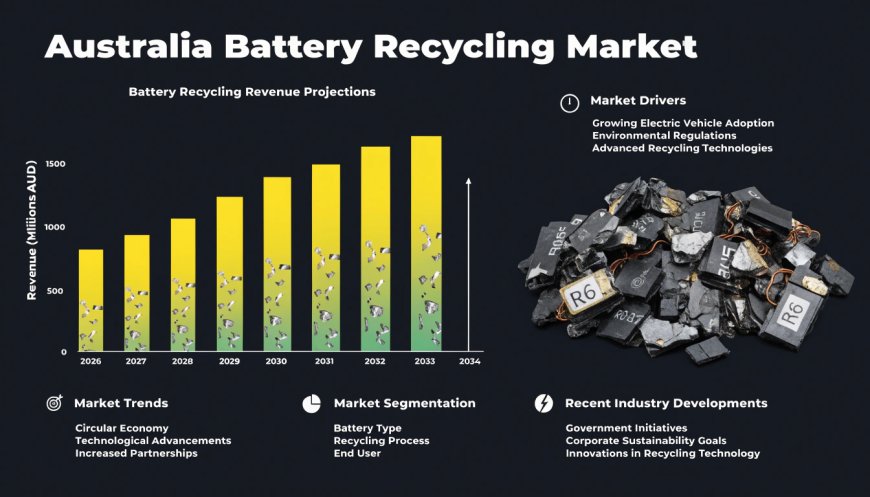

The Australia battery recycling market was valued at approximately USD 312.6 million in 2025 and is projected to reach USD 1.14 billion by 2034

Market Overview

The Australia battery recycling market was valued at approximately USD 312.6 million in 2025 and is projected to reach USD 1.14 billion by 2034, expanding at a compound annual growth rate (CAGR) of around 15.5% during the forecast period 2026–2034. The market is experiencing exceptional growth momentum driven by the rapid proliferation of lithium-ion batteries across electric vehicles, utility-scale and residential energy storage systems, consumer electronics, and industrial applications, combined with the federal and state governments' accelerating policy focus on establishing a sovereign battery materials processing and recycling capability that reduces Australia's dependence on offshore processing of critical minerals recovered from end-of-life battery streams. Australia's unique strategic position as the world's largest producer of lithium and a leading producer of cobalt, nickel, and manganese — the critical materials embedded in modern lithium-ion battery chemistries — creates a powerful industrial logic for developing domestic battery recycling infrastructure that can recover and reintroduce these high-value materials into the domestic battery manufacturing supply chain rather than exporting them as low-value waste to offshore processors. The convergence of rapidly growing end-of-life battery volumes, tightening product stewardship regulation under the federal Battery Stewardship Scheme, surging corporate and government investment in battery recycling infrastructure, and the emergence of a globally significant battery manufacturing ecosystem in Australia that requires domestically sourced recycled materials is creating the conditions for transformational market expansion throughout the forecast period. Australia's battery recycling market is firmly positioned as a critical enabler of the country's broader ambition to become a globally significant battery and clean energy technology manufacturing nation, with the sector attracting increasing attention from international strategic investors, battery manufacturers, and critical minerals processing companies seeking to establish positions in what is widely recognized as one of the most strategically important emerging industrial sectors of the 21st century.

How AI and Advanced Technology Are Reshaping the Future of the Australia Battery Recycling Market

Artificial intelligence, robotics, advanced materials characterization technologies, and digital process optimization platforms are fundamentally transforming the efficiency, safety, economics, and environmental performance of battery recycling operations across Australia, enabling the sector to manage an increasingly complex and diverse incoming battery waste stream while maximizing the recovery value of critical materials. The following analytical insights capture the depth and breadth of this transformation:

-

AI-Powered Battery Sorting and Chemistry Identification: One of the most operationally challenging aspects of battery recycling is the accurate and rapid identification of incoming battery chemistries — lithium iron phosphate, nickel manganese cobalt, nickel cobalt aluminum, and other formulations each require different processing pathways to maximize material recovery value and ensure safe handling. Australian battery recycling operators are deploying AI-powered computer vision systems and X-ray fluorescence spectroscopy platforms combined with machine learning classification algorithms to automatically identify battery chemistry, state of health, and residual charge level within seconds of intake — replacing manual sorting processes that are both slower and exposed to significant safety risks from thermally unstable cells. These AI sorting systems are reported to achieve chemistry classification accuracy rates exceeding 99.2%, dramatically reducing misrouting of batteries into incorrect processing streams that previously resulted in both material recovery losses and thermal incident risks.

-

Robotic Disassembly and Automated Dismantling Systems: The disassembly of electric vehicle battery packs — complex assemblies comprising hundreds of individual cells, thermal management components, battery management system electronics, and structural housing materials — has historically been a highly labor-intensive and hazardous manual process that represents a significant cost and throughput constraint in the recycling value chain. Australian battery technology companies and recycling operators are investing in robotic disassembly platforms that use AI-driven force control, computer vision guidance, and collaborative robot systems to automate the disassembly of battery packs with documented throughput improvements of 3–4 times compared to manual disassembly workflows, while simultaneously reducing worker exposure to high-voltage electrical systems and toxic electrolyte chemicals.

-

Machine Learning for Hydrometallurgical Process Optimization: The hydrometallurgical processing of black mass — the mixed lithium, cobalt, nickel, and manganese material recovered from shredded battery cells — involves complex multi-stage chemical leaching, separation, and precipitation processes whose efficiency is highly sensitive to input material composition variability. Australian recycling companies including Envirostream and Li-Cycle's planned Australian operations are deploying machine learning models trained on thousands of process data points to dynamically optimize reagent dosing, temperature profiles, and residence times in response to real-time incoming feed composition data, achieving reported improvements in critical material recovery rates of 8–15% compared to fixed process parameter operation and significant reductions in reagent consumption costs.

-

Digital Battery Passports and Lifecycle Traceability: The European Union's forthcoming mandatory battery passport regulation — which will require documented lifecycle data for all batteries sold in EU markets — is driving Australian battery recyclers and manufacturers to invest in blockchain-anchored digital traceability platforms that record battery chemistry, provenance, usage history, and end-of-life processing outcomes. Companies including Circular Energy Storage and several Australian battery manufacturers are developing digital battery passport systems that enable recycled material certificates to be issued for recovered lithium, cobalt, and nickel that satisfy both EU regulatory requirements and the growing corporate sustainability due diligence demands of international battery manufacturing customers sourcing recycled content materials from Australian processors.

-

Predictive Safety Monitoring and Thermal Event Prevention: Battery fires — particularly in lithium-ion battery storage facilities handling partially charged end-of-life cells — represent the most significant operational risk in the battery recycling industry, with several high-profile thermal runaway incidents at international recycling facilities highlighting the consequences of inadequate battery state monitoring. Australian recycling operators are deploying AI-powered sensor fusion platforms that continuously monitor temperature, gas emissions, voltage, and impedance across battery storage and processing areas, using anomaly detection algorithms to identify the early signatures of thermal runaway development hours before visible symptoms emerge — enabling preemptive isolation and safe discharge of at-risk cells before catastrophic failure occurs.

-

Demand Forecasting and Collection Network Optimization: The economic viability of battery recycling operations is critically dependent on achieving sufficient incoming volume to justify processing infrastructure investment, making the optimization of collection network design and end-of-life battery demand forecasting a strategically important capability. B-cycle, Australia's national battery stewardship scheme, is deploying AI-powered demand forecasting models that integrate EV fleet registration data, consumer electronics sales volumes, battery warranty expiry profiles, and collection point utilization data to predict regional end-of-life battery volumes with 18–24 month forward visibility — enabling infrastructure investment decisions to be aligned with actual incoming material flows rather than broad market estimates.

-

Advanced Materials Characterization for Recovered Material Certification: Australian battery recyclers targeting premium-priced certified recycled material supply agreements with battery manufacturers require the ability to provide granular chemical composition certification for recovered lithium carbonate, cobalt sulfate, nickel sulfate, and manganese compounds that meets battery-grade purity specifications. AI-assisted spectroscopic analysis platforms are enabling real-time quality certification of recovered materials at production line speed, replacing laboratory batch testing cycles that previously introduced 48–72 hour delays between production and quality certification — a capability that is essential for integrating recycled material streams into just-in-time battery manufacturing supply chains.

Grab a sample PDF of this report: https://www.imarcgroup.com/australia-battery-recycling-market/requestsample

Market Growth Factors

Accelerating Electric Vehicle Adoption and the Emerging End-of-Life Battery Wave Australia's electric vehicle market has entered a phase of exponential growth following years of lagging international adoption rates, with EV sales reaching approximately 98,000 units in 2024 — representing 7.2% of new vehicle sales — and forecast to exceed 250,000 annual units by 2027 as a broader model range across all vehicle segments becomes available at competitive price points. This rapid EV fleet accumulation is creating a correspondingly large and growing pipeline of end-of-life battery packs that will begin reaching end-of-warranty condition from approximately 2028 onward, with industry modeling suggesting that Australia's annual end-of-life EV battery volume will exceed 30,000 tonnes by 2030 and grow exponentially thereafter as the 2024–2026 EV sales cohort reaches its ten-year useful life. The material value embedded in these end-of-life battery packs is extraordinary by the standards of conventional waste streams: a typical 75-kilowatt-hour EV battery pack contains approximately 8–10 kilograms of lithium, 10–15 kilograms of cobalt in NMC chemistry variants, 30–40 kilograms of nickel, and 180–200 kilograms of aluminum and copper structural materials, with combined recovered material values ranging from AUD 800 to AUD 2,400 per pack depending on prevailing critical mineral prices. Beyond passenger vehicles, the accelerating deployment of utility-scale battery energy storage systems — driven by Australia's renewable energy transition program — is creating a separate and equally significant pipeline of large-format battery assets that will require end-of-life processing, with the first generation of utility-scale BESS installations from 2017–2020 approaching their expected operational lifespans. The combination of these converging end-of-life battery streams from multiple application sectors is establishing a raw material supply foundation for the Australian battery recycling industry that will sustain capacity utilization across planned processing infrastructure investments and create the volume certainty required to attract the institutional capital necessary for next-generation hydrometallurgical refinery development.

Federal and State Government Policy Frameworks and Critical Minerals Strategy The Australian government has identified battery recycling and critical minerals processing as foundational pillars of its Future Made in Australia industrial policy agenda, committing substantial financial support and regulatory framework development to accelerate the establishment of a sovereign battery materials recovery and reprocessing capability. The federal government's AUD 1 billion Critical Minerals Facility — administered through Export Finance Australia — provides concessional debt financing to critical minerals processing projects including battery recycling facilities that demonstrate a pathway to producing battery-grade recycled materials for domestic or allied nation supply chains. The National Battery Strategy, published in 2023 and supported by ongoing implementation funding, establishes a comprehensive policy framework targeting the development of an integrated Australian battery value chain from raw material extraction through cell manufacturing to recycling and material recovery — with battery recycling explicitly positioned as the closing loop that enables the circular economy model essential to the long-term competitiveness of domestic battery manufacturing. The Battery Stewardship Scheme — a federal producer responsibility initiative branded B-cycle that mandates battery recycling obligations for importers and manufacturers of portable batteries — has established a national collection and recycling infrastructure network that processed over 1,850 tonnes of batteries in its 2024 operational year, with volume projections indicating a doubling of collection throughput by 2027 as consumer awareness programs and retail collection point density improve. State-level policy initiatives are adding further investment certainty, with Victoria's Battery Recycling Infrastructure Program committing AUD 18 million to co-fund battery recycling facility development, Queensland's Critical Minerals and Battery Technology Roadmap targeting the establishment of an integrated battery recycling hub in the Gladstone industrial precinct, and Western Australia's Battery Industry Development Initiative seeking to leverage the state's critical minerals production base to attract integrated battery recycling and reprocessing investment. The cumulative effect of these overlapping federal and state policy commitments is to create an investment environment with sufficient regulatory certainty, financial support mechanisms, and long-term demand visibility to justify the substantial capital expenditure required to establish world-class battery recycling infrastructure in Australia.

Critical Minerals Supply Chain Security and the Circular Economy Imperative The strategic imperative for Australia to develop domestic battery recycling capability is underpinned by a powerful supply chain security logic that extends well beyond the environmental benefits of diverting battery waste from landfill: as Australia positions itself to become a significant battery cell and battery materials manufacturer through investments including the planned Novonix anode material plant in Queensland, the emerging lithium hydroxide refining industry in Western Australia, and the federal government's support for downstream battery manufacturing through the AUD 1 billion Battery Breakthrough Initiative, the availability of domestically processed recycled battery materials will become a critical competitive input that reduces dependence on primary mining-derived materials and insulates Australian manufacturers from the supply chain disruptions and price volatility that characterize the globally concentrated critical minerals processing industry currently dominated by China. Recycled lithium from end-of-life batteries commands a growing price premium over primary lithium in markets where battery manufacturers are under pressure from automotive OEM customers and government procurement frameworks to achieve minimum recycled content thresholds — a regulatory trend already enacted in the European Union's Battery Regulation and under active consideration in Australia's trading partner markets. The corporate sustainability commitments of major automotive OEMs including Toyota, Volkswagen, and General Motors — all of which have announced minimum recycled content targets for their battery supply chains by 2030 — are creating direct demand for certified Australian recycled battery materials that can be incorporated into global battery supply chains with full chain-of-custody documentation. Australian battery recycling operators that establish processing capabilities and quality certifications aligned with international battery-grade material specifications are well-positioned to capture significant export revenue from these corporate sustainability-driven demand flows, adding an export market dimension to the battery recycling value proposition that substantially improves project economics beyond the domestic material recovery value alone and creates a self-reinforcing investment case for continued capacity expansion throughout the forecast period.

Market Segmentation

Battery Chemistry Type Insights:

-

Lithium-Ion Batteries — The dominant and fastest-growing segment by incoming volume and recovered material value, encompassing EV battery packs, grid-scale energy storage modules, and consumer electronics batteries, with recovery processes targeting lithium, cobalt, nickel, manganese, copper, and aluminum as primary value streams.

-

Lead-Acid Batteries — The historically largest segment by weight processed, with a mature and commercially established recycling infrastructure supported by high lead recovery economics and the continuous replacement cycle of automotive starter batteries across Australia's large vehicle fleet, maintaining relevance despite the growth of lithium-ion as the primary value growth driver.

-

Nickel-Based Batteries — A smaller but significant segment encompassing nickel-metal hydride batteries from hybrid vehicles and industrial applications, with established processing pathways and stable nickel recovery economics supporting continued commercial viability.

-

Other Chemistries — Including zinc-carbon, alkaline, and emerging solid-state battery chemistries, collectively representing a growing processing challenge as battery chemistry diversity expands across consumer and industrial applications.

Application Insights:

-

Electric Vehicle and Automotive Battery Recycling — The highest-growth application segment by capital investment and strategic priority, driven by the accelerating Australian EV fleet accumulation and the high individual unit value of end-of-life EV battery packs relative to other battery waste categories.

-

Consumer Electronics and Portable Battery Recycling — The largest segment by unit volume, encompassing smartphones, laptops, power tools, and e-mobility devices including e-scooters and e-bikes, serviced primarily through the B-cycle national collection network and retail drop-off infrastructure.

-

Industrial and Stationary Storage Battery Recycling — A rapidly growing segment driven by the retirement of first-generation grid-scale BESS installations and industrial uninterruptible power supply systems, offering large individual unit sizes that reduce collection logistics costs and improve processing economics.

Regional Insights:

-

New South Wales — The largest state market by battery waste volume and recycling infrastructure investment, anchored by Sydney's concentration of consumer electronics consumption, EV adoption, and the presence of established battery recycling operators including Envirostream's primary processing facility, with planned capacity expansions targeting the growing EV battery stream.

-

Victoria — A leading market for battery recycling policy development and infrastructure investment, with the state government's Battery Recycling Infrastructure Program actively co-funding facility development and Melbourne's manufacturing and logistics infrastructure supporting efficient battery collection and processing operations.

-

Western Australia and Queensland — High-growth markets driven by the mining and resources sector's significant industrial battery waste streams, large EV fleet growth in Perth and Brisbane metropolitan areas, and the strategic positioning of both states as potential locations for integrated battery recycling and critical minerals reprocessing hubs targeting export market development.

Key Players

-

Envirostream Australia

-

B-cycle (Battery Stewardship Council)

-

Lithium Australia Limited

-

Neometals Ltd

-

Ecobatt

-

Toxco (Retriev Technologies Australian Operations)

-

Battery World Australia

-

CleanPeak Energy (Storage Recycling Division)

-

Reclaim PV Recycling (Battery Division)

-

5B Solar (Battery Recycling Partnerships)

-

Renew Systems

-

Li-Cycle (Planned Australian Operations)

Recent Development & News

March 2025: The Australian federal government announced the approval of a AUD 76 million co-investment under the Critical Minerals Facility for Neometals Ltd's Primobius battery recycling joint venture, supporting the construction of a commercial-scale lithium-ion battery recycling facility in Laverton North, Victoria, designed to process up to 10,000 tonnes of end-of-life lithium-ion batteries annually and produce battery-grade recycled lithium hydroxide, cobalt sulfate, and nickel sulfate for supply to domestic and international battery manufacturers. The facility, developed in partnership with German engineering group SMS Group, employs a proprietary combined mechanical and hydrometallurgical processing technology that Neometals reports achieves recovery rates of over 98% for lithium, cobalt, nickel, and manganese from incoming black mass feed — materially exceeding the 85–90% recovery rates achievable by conventional pyrometallurgical processing approaches. The strategic significance of this investment extends substantially beyond its direct processing capacity: it establishes Australia's first commercial-scale facility capable of producing certified battery-grade recycled materials that meet the purity specifications required by major battery cell manufacturers, creating a domestic proof-of-concept that validates the technical and commercial viability of the Australian battery recycling industry model for subsequent investors and capacity expansions. The market impact is expected to be catalytic, with industry analysts projecting that the Primobius facility's successful commissioning will precipitate at least three additional commercial-scale battery recycling facility announcements within 18 months as competing operators seek to establish positions ahead of the anticipated surge in EV end-of-life battery volumes from 2028 onward.

June 2025: B-cycle, Australia's national battery stewardship scheme, released its 2024–2025 annual impact report revealing that the scheme had collected and processed 2,340 tonnes of portable batteries through its national network of over 4,200 collection points — representing a 26% year-on-year increase in collection volume and a cumulative total of 5,890 tonnes processed since the scheme's launch in 2022. The report additionally announced the expansion of B-cycle's collection network to include 680 new collection points across regional and rural areas of Australia, addressing the significant geographic coverage gap that had previously resulted in substantially lower per-capita collection rates in non-metropolitan areas compared to major capital cities. The strategic importance of this collection network expansion cannot be overstated in the context of the broader battery recycling market's development trajectory: the economic viability of investment in advanced battery processing infrastructure is fundamentally dependent on achieving reliable and geographically distributed incoming material flows, and B-cycle's network expansion directly addresses the collection logistics challenge that has historically constrained the ability of Australian recycling operators to guarantee consistent feed volumes to capital-intensive processing facilities. B-cycle simultaneously announced the launch of a dedicated collection and logistics pathway for small-format lithium-ion batteries from e-mobility devices — e-scooters, e-bikes, and personal mobility aids — a category that has experienced rapid volume growth associated with significant fire safety concerns due to the prevalence of substandard battery chemistries in imported devices, with the dedicated stream enabling safer separate handling of these higher-risk battery types.

September 2025: Lithium Australia Limited announced the successful commissioning and first commercial production run at its upgraded VSPC cathode material plant in Welshpool, Western Australia, which has been reconfigured to incorporate a recycled lithium feedstock processing capability allowing the facility to produce battery-grade lithium iron phosphate cathode material using lithium recovered from end-of-life lithium-ion batteries as a partial feed supplement to primary lithium carbonate. This development represents a globally significant milestone as it establishes Australia's first documented commercial production of battery cathode material incorporating domestically recovered recycled lithium content — closing the battery circular economy loop from end-of-life recovery through to new battery material production within Australian borders for the first time. The strategic implications are profound for Australia's aspiration to develop an integrated domestic battery value chain: by demonstrating that recycled lithium recovered from Australian end-of-life batteries can be successfully reintroduced into cathode material manufacturing at commercial production quality standards, Lithium Australia has validated the technical foundation for a closed-loop battery materials ecosystem that could progressively reduce the Australian battery manufacturing industry's dependence on primary lithium mining as recycled material volumes grow with the maturing EV fleet. The company reported that cathode material produced with recycled lithium feed achieved electrochemical performance characteristics within 2% of equivalent material produced from primary lithium sources, a performance equivalence finding that is expected to accelerate the willingness of battery cell manufacturers to specify recycled content cathode materials in their supply agreements.

November 2025: The Australian Competition and Consumer Commission approved the formation of a Collective Recycling Infrastructure Agreement among five of Australia's leading battery recycling operators — Envirostream, Ecobatt, Retriev Technologies, Reclaim PV Recycling, and CleanPeak Energy — permitting the companies to collectively invest in and jointly operate shared pre-processing infrastructure including battery sorting, safe discharge, and mechanical shredding facilities across three locations in Sydney, Melbourne, and Brisbane. The ACCC's approval, granted under a formal authorization on public benefit grounds, recognized that the shared infrastructure model would enable the participating operators to achieve the processing scale economics necessary to justify investment in advanced hydrometallurgical refining capabilities that none of the individual operators could achieve on a standalone basis given their respective current incoming volume projections. The market impact of this structural development is potentially transformational: by enabling pre-competitive cooperation on capital-intensive shared infrastructure while preserving competition in the higher-value downstream material refining and marketing activities, the agreement creates a viable pathway for the Australian battery recycling industry to achieve the processing scale necessary to attract international battery manufacturer offtake agreements — which typically require minimum annual supply volumes of 500–1,000 tonnes of individual recovered materials — within a commercially realistic investment timeline. Industry analysts estimate that the shared infrastructure model could reduce the capital cost per tonne of processing capacity by 35–45% compared to fully vertically integrated standalone facility development, significantly improving the investment case for all participating operators and creating a template for similar collaborative infrastructure models in other Australian states.

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

Request Customization: https://www.imarcgroup.com/request?type=report&id=37023&flag=E

About Us

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services including market assessment, feasibility studies, regulatory approvals, competitive benchmarking, pricing research, and procurement research.

Contact Us

IMARC Group 134 N 4th St. Brooklyn, NY 11249, USA Email: sales@imarcgroup.com Tel No: (D) +91 120 433 0800 United States: +1-201-971-6302

What's Your Reaction?