Australia Generic Drug Market Projected to Reach USD 19.1 Billion by 2033

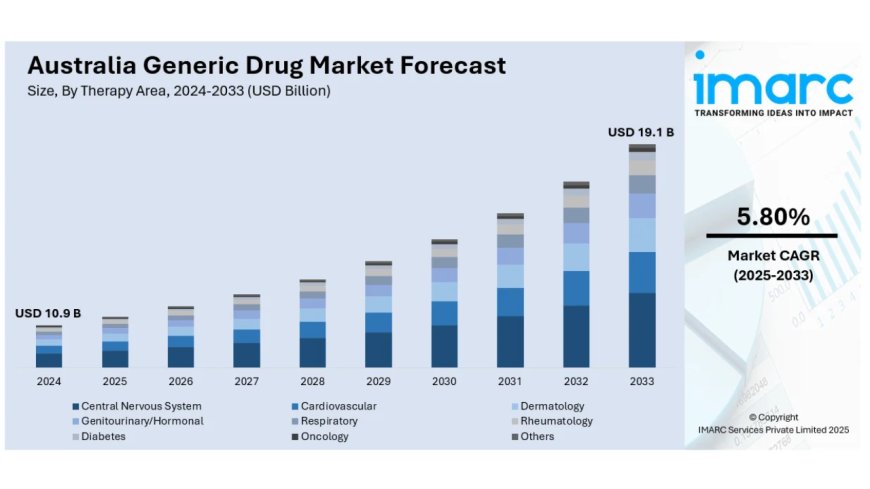

Australia generic drug market size reached USD 10.9 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 19.1 Billion by 2033, exhibiting a CAGR of 5.80% during 2025-2033

The latest report by IMARC Group, titled "Australia Generic Drug Market Report by Therapy Area (Central Nervous System, Cardiovascular, Dermatology, Genitourinary/Hormonal, Respiratory, Rheumatology, Diabetes, Oncology, Others), Drug Delivery (Oral, Injectables, Dermal/Topical, Inhalers), Distribution Channel (Retail Pharmacies, Hospital Pharmacies), and Region 2025-2033," offers comprehensive analysis of the Australia generic drug market growth. The report includes competitor and regional analysis, along with detailed breakdown of the market segmentation. The Australia generic drug market size reached USD 10.9 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 19.1 Billion by 2033, exhibiting a CAGR of 5.80% during 2025-2033.

Base Year: 2024

Forecast Years: 2025-2033

Historical Years: 2019-2024

Market Size in 2024: USD 10.9 Billion

Market Forecast in 2033: USD 19.1 Billion

Market Growth Rate (2025-2033): 5.80%

Australia Generic Drug Market Overview

The Australian generic drug market is witnessing robust growth, driven by rising healthcare costs and the growing demand for affordable treatment alternatives that deliver clinically equivalent outcomes at substantially lower prices. Strong government support through the Pharmaceutical Benefits Scheme (PBS)—which subsidizes around 80% of prescription medicines with annual funding exceeding $5.1 billion—continues to underpin market expansion. The increasing acceptance of biosimilars as cost-effective options for cancer and autoimmune disease treatments, coupled with the rising prevalence of chronic conditions such as cardiovascular disease, diabetes, and respiratory disorders requiring long-term therapy, further fuels demand. Additionally, investments in local manufacturing are enhancing supply stability and reducing dependence on imports.

Market growth is further supported by the patent expiry of high-volume branded drugs, creating opportunities for generic entry in lucrative therapeutic areas. Pharmacists’ expanded role in generic substitution, aligned with PBS guidelines, encourages broader adoption. Regulatory and policy support from the Therapeutic Goods Administration (TGA), which enforces stringent quality standards, along with public awareness initiatives addressing misconceptions about generic drug safety and efficacy, have also strengthened market confidence. Community pharmacies play a vital role through funding, training, and professional development programs that promote generic usage.

Australia’s generic drug sector shows strong performance across multiple therapeutic categories, including cardiovascular drugs targeting hypertension and heart disease, diabetes treatments addressing a growing patient base, oncology generics and biosimilars reducing cancer care costs, central nervous system (CNS) drugs for mental health and neurological disorders, and respiratory medications for asthma and chronic obstructive pulmonary disease (COPD).

Dominated by oral delivery systems, the market is also seeing rising biosimilar adoption for biologics, improved retail pharmacy distribution ensuring broad accessibility, and growth in personalized generics and niche formulations for pediatric and geriatric populations. Digital transformation, including e-prescription systems, is further facilitating generic substitution and patient convenience.

Regionally, the Australian Capital Territory (ACT) and New South Wales (NSW) lead market growth, supported by dense healthcare infrastructure and higher population concentrations. Australia’s emphasis on healthcare cost containment, PBS price structures promoting generic uptake, and prescriber guidelines advocating active ingredient prescribing continue to strengthen its position as a dynamic market for affordable medicines and pharmaceutical industry advancement. However, challenges persist, including pricing pressures, lingering perception barriers, and supply chain vulnerabilities.

Request For Sample Report:

https://www.imarcgroup.com/australia-generic-drug-market/requestsample

Australia Generic Drug Market Trends

• Biosimilar adoption growth: Rising popularity of biosimilars providing cost-saving alternatives to original biologics for treating cancer and autoimmune disorders, with healthcare providers gaining confidence in prescribing biosimilars due to favorable clinical experiences and government programs ensuring safety and accessibility.

• Local manufacturing expansion: Movement towards developing domestic pharmaceutical production base reducing import dependence, with companies investing in local facilities for stable supply following global disruptions, lowering costs, enhancing turnaround times, and providing employment opportunities.

• Digital health integration: E-prescription expansion enabling pharmacists to access real-time prescription data and suggest generic alternatives efficiently, with telehealth integration increasing opportunities for generic promotion, patient apps expanding access, and digital platforms improving medication tracking.

• Patent cliff opportunities: Steady boost from blockbuster branded drug patent expirations creating generic entry opportunities in cardiovascular, oncology, and diabetes care segments, driving competition, improving patient access, and causing sharp price reductions accelerating market growth.

• Pharmacist empowerment: Increasing pharmacist influence on patient medication choices through PBS generic substitution guidelines, with continuing education initiatives equipping pharmacists to educate patients on generic safety and effectiveness enhancing uptake at dispensing level.

• Personalized formulation development: Pharmaceutical technology advancements creating opportunities for specialized generics tailored to pediatric and geriatric patients requiring modified dosages or delivery forms including dissolvable tablets and liquid suspensions filling treatment gaps.

Market Drivers

• Healthcare cost pressures: Rising healthcare expenditures placing financial pressure on public systems and consumers with generic drugs offering clinically equivalent alternatives at significantly lower costs, helping control pharmaceutical spending while maximizing treatment accessibility and managing budgets.

• PBS reimbursement framework: Pharmaceutical Benefits Scheme providing substantial government support subsidizing around 80% of prescriptions with annual funding exceeding $5.1 billion, using price disclosure mechanisms and reference pricing encouraging generic substitution through reduced reimbursement costs.

• Chronic disease prevalence: Growing patient population managing cardiovascular diseases, diabetes, asthma, and hypertension requiring long-term medication management creating sustained demand for affordable generic treatments particularly under PBS coverage ensuring accessibility.

• Aging population demographics: Increasing elderly population with higher medication needs and polypharmacy requirements driving demand for cost-effective generic alternatives, particularly for chronic conditions requiring multiple prescriptions and extended treatment duration.

• Regulatory quality standards: Therapeutic Goods Administration enforcing strict safety and quality standards for generics motivating replacement of branded drugs, with clear labeling standards reinforcing clinical equivalence and building healthcare provider and patient confidence.

• Export market potential: Australia's stringent pharmaceutical standards and quality reputation positioning manufacturers as trusted exporters to Asia-Pacific region, with free trade agreements and regulatory harmonization enhancing cross-border drug approval ease and regional market access.

Challenges and Opportunities

Challenges:

- Market consolidation and pricing pressure with large pharmacy chains exerting strong bargaining power negotiating steep price reductions, PBS price disclosure policies forcing thin profit margins, limiting innovation investment and potentially impacting competition and drug availability

- Limited public awareness and perception gaps with significant population portions lacking trust in generic quality and efficacy particularly among older patients, with misinformation, brand loyalty, and fear of reduced effectiveness contributing to low conversion rates

- Supply chain disruptions and import dependence with heavy reliance on imported APIs and finished generics from India and China making supply vulnerable to global disruptions, pandemics, geopolitical tensions, and shipping delays causing shortages

- Regulatory compliance costs with maintaining TGA standards requiring substantial investment in quality control, testing, documentation, and manufacturing processes creating financial burden particularly for smaller generic manufacturers competing on thin margins

Opportunities:

- Personalized generics and niche formulations developing specialized products for underserved pediatric and geriatric segments requiring modified dosages or delivery forms, with pharmacogenomics innovations enabling individualized therapies using generic APIs building competitive differentiation

- Asia-Pacific export expansion leveraging Australia's quality reputation and stringent standards to supply affordable healthcare solutions to neighboring countries experiencing rising demand, with free trade agreements and regional proximity enhancing market penetration capabilities

- Digital transformation and e-prescriptions utilizing expanding digital health infrastructure for improved generic promotion through real-time prescription data access, telehealth integration, patient education apps, and e-pharmacy services increasing awareness and accessibility

- PBS listing expansion securing more generic products under Pharmaceutical Benefits Scheme ensuring widespread access particularly for chronic and high-volume conditions, with tiered pricing models favoring early adopters and structured reimbursement enhancing value proposition

- Biosimilar market growth capitalizing on increasing acceptance of biosimilars for high-cost biologic treatments with healthcare system budget management driving adoption, physician confidence building, and government programs supporting safety and accessibility initiatives

Australia Generic Drug Market Segmentation

By Therapy Area:

- Central Nervous System

- Cardiovascular

- Dermatology

- Genitourinary/Hormonal

- Respiratory

- Rheumatology

- Diabetes

- Oncology

- Others

By Drug Delivery:

- Oral

- Injectables

- Dermal/Topical

- Inhalers

By Distribution Channel:

- Retail Pharmacies

- Hospital Pharmacies

By Region:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Browse Full Report:

https://www.imarcgroup.com/australia-generic-drug-market

Australia Generic Drug Market News (2024-2025)

• 2024: Pharmaceutical Benefits Scheme maintained annual funding exceeding $5.1 billion subsidizing around 80% of prescription drugs reinforcing government commitment to making generic medications widely accessible and affordable across Australian healthcare system.

• 2024: Biosimilar adoption accelerated with healthcare providers increasingly confident in prescribing cost-saving alternatives for cancer and autoimmune disorders, supported by government programs ensuring safety, quality, and accessibility standards.

• 2024: Local manufacturing initiatives expanded with pharmaceutical companies investing in domestic production facilities to strengthen supply chain resilience following global disruptions, reducing import dependence and customizing production for local requirements.

• 2024: Digital health infrastructure advancement facilitated generic promotion with e-prescription expansion enabling pharmacists to access real-time data and suggest cost-effective alternatives efficiently improving substitution rates.

• 2024: Community Pharmacy Agreement programs continued incentivizing pharmacists to promote cost-effective treatments through medication management services, patient consultations, and education on generic use particularly for chronic diseases.

• 2024: Therapeutic Goods Administration reinforced labeling standards distinguishing generics while emphasizing clinical equivalence to branded medications, supporting public awareness campaigns dispelling misconceptions about generic safety and quality.

• 2024: Patent expirations for multiple blockbuster branded drugs created generic entry opportunities in cardiovascular, oncology, and diabetes therapeutic areas driving competition and improving patient access through price reductions.

• 2024: Prescriber guidelines promoted active ingredient name prescribing enabling pharmacists to substitute with available generic products, with general practitioner education initiatives building confidence in generic equivalence and cost-effectiveness.

Key Highlights of the Report

- Market Performance (2019-2024)

- Market Outlook (2025-2033)

- Industry Catalysts and Challenges

- Segment-wise historical and future forecasts

- Competitive Landscape and Key Player Analysis

- Therapy Area, Drug Delivery, Distribution Channel, and Regional Analysis

Ask analyst for your customized sample:

http://imarcgroup.com/request?type=report&id=33092&flag=F

Competitive Landscape

The Australia generic drug market features a mix of multinational pharmaceutical companies and domestic manufacturers competing across multiple therapeutic areas. Major international players leverage global R&D capabilities, extensive product portfolios, and established distribution networks to maintain market positions. Local manufacturers focus on specialized formulations, regional partnerships, and government contract opportunities. Competition intensifies around PBS listings, with companies pursuing price competitiveness while maintaining quality standards. Biosimilar segments attract strategic investments as patent cliffs create opportunities. Market consolidation pressures manufacturers to optimize costs while regulatory compliance requirements demand quality investments. Strategic partnerships between manufacturers, pharmacy chains, and healthcare providers shape distribution dynamics.

Major Companies Operating in the Market:

- AstraZeneca

- Cipla Ltd

- Dr. Reddy's Laboratories Ltd

- Generic Health

- Noumed Pharmaceuticals Pty Ltd

- Sandoz AG

- Sun Pharmaceutical Industries Ltd

- Teva Pharma Australia Pty Ltd

- Viatris Inc.

Q&A Section

Q1: What drives growth in the Australia generic drug market?

A1: Market growth is driven by rising healthcare costs pushing affordable alternative demand, PBS support subsidizing 80% of prescriptions with $5.1 billion+ annual funding, growing biosimilar acceptance for cancer and autoimmune treatments, increasing chronic disease prevalence requiring long-term management, patent expirations creating generic entry opportunities, and local manufacturing investments ensuring supply stability and reducing import dependence.

Q2: What are the latest trends in this market?

A2: Key trends include biosimilar adoption growth for cost-effective biologic alternatives, local manufacturing expansion reducing import reliance, digital health integration with e-prescriptions facilitating substitution, patent cliff opportunities in cardiovascular and diabetes segments, pharmacist empowerment through PBS guidelines, and personalized formulation development for pediatric and geriatric patients.

Q3: What challenges do companies face?

A3: Major challenges include market consolidation and pricing pressure with pharmacy chains negotiating steep reductions and PBS policies forcing thin margins, limited public awareness with trust gaps particularly among older patients, supply chain disruptions from import dependence on India and China, and regulatory compliance costs maintaining TGA standards creating financial burdens.

Q4: What opportunities are emerging?

A4: Emerging opportunities include personalized generics development for underserved demographics, Asia-Pacific export expansion leveraging quality reputation, digital transformation utilizing e-prescriptions and telehealth platforms, PBS listing expansion ensuring widespread access, and biosimilar market growth capitalizing on healthcare budget management needs and increasing physician confidence.

Q5: What is the market forecast for Australia generic drugs?

A5: The Australia generic drug market was valued at USD 10.9 Billion in 2024 and is projected to reach USD 19.1 Billion by 2033, exhibiting a CAGR of 5.80% during 2025-2033, driven by healthcare cost containment, government support, chronic disease prevalence, and pharmaceutical innovation.

Q6: What role does the PBS play in market growth?

A6: The Pharmaceutical Benefits Scheme is critical, subsidizing around 80% of prescriptions with annual funding exceeding $5.1 billion, using price disclosure mechanisms and reference pricing to encourage generic substitution through reduced reimbursement costs, ensuring widespread access particularly for chronic conditions, and supporting tiered pricing models favoring early adopters.

Q7: Which therapeutic areas dominate the market?

A7: Key therapeutic areas include cardiovascular medications addressing hypertension and heart disease prevalence, diabetes treatments managing growing patient populations, oncology generics and biosimilars reducing cancer treatment costs, central nervous system medications for mental health conditions, and respiratory drugs treating asthma and COPD with oral delivery dominating prescription volumes.

About Us

IMARC Group is a leading market research company that offers management strategy and market research worldwide. We partner with clients in all sectors and regions to identify their highest-value opportunities, address their most critical challenges, and transform their businesses. IMARC's information products include major market, scientific, economic and technological developments for business leaders in pharmaceutical, industrial, and high technology organizations. Market forecasts and industry analysis for biotechnology, advanced materials, pharmaceuticals, food and beverage, travel and tourism, nanotechnology and novel processing methods are at the top of the company's expertise.

Contact Us

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91-120-433-0800

United States: +1-201-971-6302

What's Your Reaction?