India Solar Panel Market 2026-2034: 22.94% CAGR Industry Expansion, Key Dynamics & Strategic Forecasts

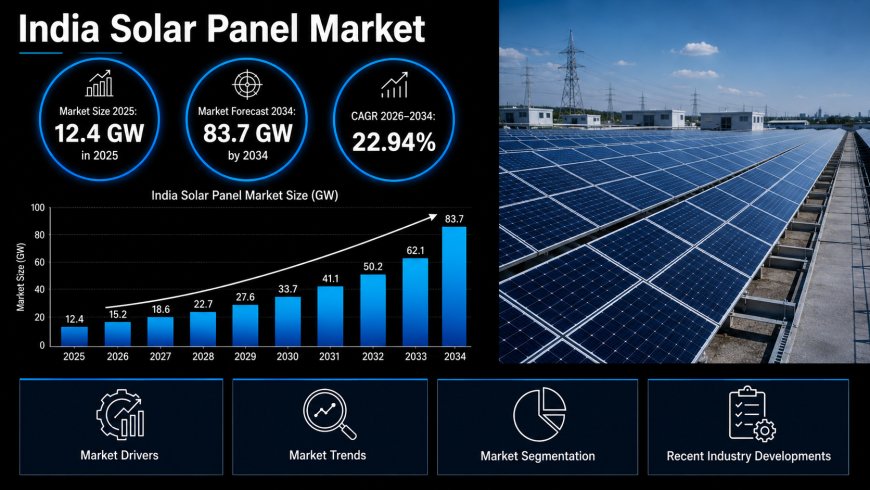

The India solar panel market size reached 12.4 GW in 2025. Looking forward, IMARC Group expects the market to reach 83.7 GW by 2034, exhibiting a growth rate (CAGR) of 22.94% during 2026-2034.

According to IMARC Group’s report titled “India Solar Panel Market Size, Share, Trends and Forecast by Type, End Use, and Region, 2026-2034“, The report offers a comprehensive analysis of the industry, including India solar panel market share, forecast, growth and regional insights.

The India solar panel market size reached 12.4 GW in 2025. Looking forward, IMARC Group expects the market to reach 83.7 GW by 2034, exhibiting a growth rate (CAGR) of 22.94% during 2026-2034.

India is executing a massive, policy-driven structural shift in its power architecture, transitioning rapidly from fossil-fuel dependence to a decentralized, utility-scale renewable energy grid.

- Technological Dominance: Monocrystalline technology now commands the market with approximately 48.9% market share in 2025, driven by superior conversion efficiencies.

- Utility-Scale Dependency: Large-scale utility projects account for nearly 87% of the total installed capacity, serving as the foundational volume driver for domestic panel procurement.

The CXO Blindspot: How the Solar Panel Market is Reshaping the Energy & Mining Sector in India

A critical vulnerability within India's renewable energy infrastructure is the massive discrepancy between domestic module assembly capacity and upstream cell/wafer manufacturing capabilities. Leaders frequently overlook this structural deficit, assuming final-stage assembly equates to supply chain autonomy.Ignoring the critical supply chain vulnerabilities associated with domestic solar cell and wafer manufacturing creates a severe ripple effect across India’s Energy & Mining sector. It forces developers into heavy reliance on imported components, exposing high-capacity utility-scale projects to extreme geopolitical price volatility and currency fluctuations. Consequently, these supply chain disruptions delay the commissioning of gigawatt-scale solar parks, inflate the levelized cost of electricity (LCOE), and compress the operating margins of independent power producers nationwide.

➤ Access Key Market Statistics and Actionable Insights - Request Sample Report: https://www.imarcgroup.com/india-solar-panel-market/requestsample

India's Strategic Vision for the Solar Panel Market

- National Decarbonization Targets: The macroeconomic vision is anchored in the commitment to achieve 500 GW of non-fossil fuel capacity by 2030, with solar power functioning as the primary pillar of this energy transition.

- Domestic Self-Reliance (Atmanirbhar Bharat): The government aims to establish a vertically integrated domestic manufacturing ecosystem, structurally eliminating the reliance on imported photovoltaic cells, wafers, and polysilicon from global competitors.

- Distributed Energy Expansion: A core objective is to democratize energy generation by scaling rooftop solar installations across residential and commercial sectors, reducing the transmission load on central power grids.

Why Invest in the India Solar Panel Market: Key Growth Drivers & ROI

- Massive Consumption Base: India's rapidly industrializing economy and expanding middle class are generating exponential electricity demand. Investing in utility-scale and commercial rooftop solar captures this structural growth, offering corporate investors highly predictable, long-term revenue streams backed by sovereign and state-level power purchase agreements.

- Policy Support and Subsidies: Aggressive federal incentives, specifically the massive Production Linked Incentive (PLI) scheme for high-efficiency modules, drastically lower manufacturing capital expenditure. These proactive financial frameworks systematically insulate domestic manufacturers from initial setup risks, accelerating the break-even timeline for new facility investments.

- Premiumization via Tech Upgrades: The market is swiftly upgrading from standard polycrystalline units to advanced monocrystalline and bifacial technologies. This technological premiumization maximizes energy yield per square meter, enabling independent power producers to command higher internal rates of return on space-constrained solar park installations.

- Supply Chain Efficiencies: Establishing localized manufacturing ecosystems reduces extreme dependency on imported solar cells and wafers. By vertically integrating domestic supply chains, manufacturers achieve unparalleled operational efficiency, minimizing logistical delays, and directly protecting profit margins against volatile international freight and tariff fluctuations.

India Solar Panel Market Trends & Future Outlook

- Bifacial Module Adoption: The utility-scale sector is rapidly adopting bifacial solar panels, which capture albedo radiation from the rear side, systematically increasing total energy generation by 10-20% without expanding the physical footprint.

- Solar-Plus-Storage Integration: As grid penetration deepens, the long-term trajectory mandates pairing high-capacity panels with lithium-ion Battery Energy Storage Systems (BESS) to solve intermittency issues and provide round-the-clock (RTC) power.

- AI-Driven Plant Optimization: Large-scale solar parks are aggressively deploying artificial intelligence and IoT sensor networks to execute predictive maintenance on solar arrays, minimizing downtime and optimizing module-level cleaning schedules.

- Agrivoltaics Expansion: There is an emerging shift toward agrivoltaics—co-locating solar panels with agricultural crops—maximizing land-use efficiency and providing dual revenue streams for rural infrastructure developers.

CXO Executive Brief: Regulatory & Policy Catalysts in India

- Production Linked Incentive (PLI): According to the Ministry of New and Renewable Energy (MNRE), the National Programme on High Efficiency Solar PV Modules (PLI Scheme) actively disperses multi-crore subsidies to legally incentivize the domestic manufacturing of fully integrated solar supply chains.

- PM Surya Ghar Muft Bijli Yojana: As launched by the Government of India, this massive policy framework provides direct capital subsidies to install rooftop solar systems across one crore households, actively catalyzing immediate decentralized demand for domestic modules.

- Approved List of Models and Manufacturers (ALMM): Administered strictly by the MNRE, the ALMM mandate dictates that all government-backed and subsidized solar projects must exclusively procure panels from certified domestic manufacturers, legally securing the domestic market share.

- Basic Customs Duty (BCD): According to the Ministry of Finance, the imposition of a 40% Basic Customs Duty on imported solar modules and 25% on solar cells acts as a vital structural barrier to protect local manufacturers from price dumping.

- 100% FDI Allowance: According to Invest India, 100% Foreign Direct Investment is permitted under the automatic route for renewable energy projects, heavily facilitating the influx of global institutional capital into greenfield solar park developments.

➤ Explore the Exact Chapters and Data Scope - Get Full Brochure: https://www.imarcgroup.com/request?type=report&id=21647&flag=A

India Solar Panel Market Segmentation:

The market report offers a comprehensive analysis of the segments, highlighting those with the largest India solar panel market share. It includes forecasts for the period 2026-2034 and historical data from 2020-2025 for the following segments.

Breakup by Type:

- Crystal Silicon

- Monocrystalline Silicon

- Polycrystalline Silicon

- Thin Film

- Others

Breakup by End Use:

- Commercial

- Residential

- Industrial

Breakup by Region:

- North India

- West and Central India

- South India

- East and Northeast India

By the IMARC Group, the Top Competitive Landscape & their Positioning:

Covering an in-depth analysis of the competitive landscape, market structure, key player positioning, competitive dashboards, top winning strategies, and detailed profiles of all major industry participants you will gain access to all these exclusive insights within the full research report.

Note: If you need specific information that is not currently within the scope of the report, we can provide it to you as a part of the customization.

➤ Shape the Data to Answer Your Specific Questions - Request Customization: https://www.imarcgroup.com/request?type=report&id=21647&flag=E

Frequently Asked Questions (FAQs)

1. What is the current value and projected growth of the India Solar Panel Market?

According to IMARC Group, the market reached 12.4 GW in 2025 and is projected to reach 83.7 GW by 2034, growing at a CAGR of 22.94% (2026–2034).

2. What is driving the growth of the market?

Growth is driven by strong government initiatives, favorable renewable energy policies, declining solar technology costs, and rising demand for clean energy solutions.

3. What are the key trends in the India solar panel market?

Key trends include adoption of advanced technologies like bifacial panels, increasing domestic manufacturing, and large-scale solar installations.

4. Why is solar energy gaining importance in India?

Solar energy is gaining importance due to its role in reducing carbon emissions, ensuring energy security, and supporting India’s renewable energy targets.

5. Which segments are driving demand in this market?

Major demand comes from utility-scale solar projects, rooftop installations, and commercial & industrial applications.

Strategic Insight & Verdict

Having analyzed the trajectory of India’s solar panel market, we observe a decisive shift toward vertically integrated domestic manufacturing and high-efficiency technologies driven by policy incentives and energy security goals. Demand is increasingly centered on performance, cost optimization, and supply chain resilience. Companies that invest in advanced cell technologies, backward integration, and scale efficiencies will secure long-term advantage as India accelerates its clean energy transition.

Gaurav, Digital Market Research Strategist at IMARC Group: https://www.linkedin.com/in/gourav-shah-005425345

Verified Data Source: IMARC Group

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1-202071-6302

What's Your Reaction?