Australia Travel Insurance Market Growth and Analysis Report 2026–2034

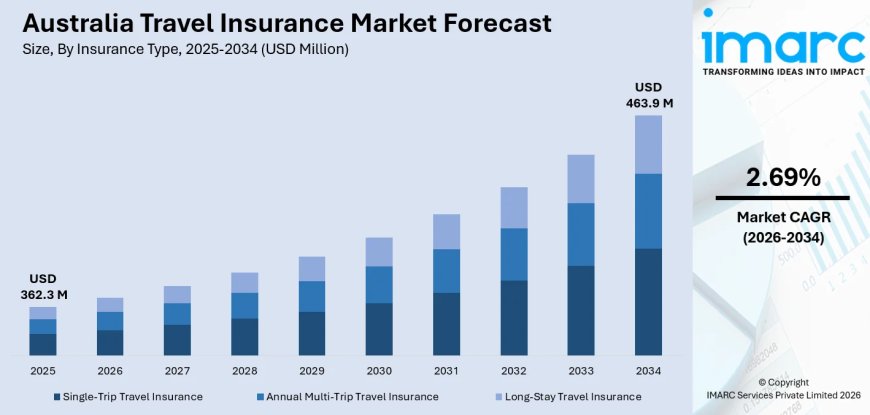

Australia travel insurance market size reached USD 362.3 Million in 2025 and is projected to reach USD 463.9 Million by 2034, growing at a compound annual growth rate of 2.69% from 2026–2034.

Market Overview

The Australia travel insurance market size reached USD 362.3 Million in 2025 and is projected to reach USD 463.9 Million by 2034, growing at a compound annual growth rate of 2.69% from 2026–2034. The market is expanding driven by surging outbound travel activity firmly surpassing pre-pandemic levels, rising consumer awareness of travel-related financial risks, and rapid adoption of digital and AI-powered insurance platforms transforming the policy and claims lifecycle. The Australian Bureau of Statistics' confirmation of 11.5 million overseas trips completed by Australians in 2024, Fast Cover's June 2025 deployment of an AI-driven claims management platform developed with Five Sigma, and Allianz Partners Australia's May 2025 launch of a cruise-specific embedded travel insurance product in partnership with Norwegian Cruise Line are collectively reinforcing the market's sustained growth trajectory throughout the forecast period.

Market Trends

Rising Risk Awareness and Post-Pandemic Behavioural Shifts

Australia's post-pandemic travel environment has fundamentally and durably altered consumer perceptions of travel insurance, elevating the product from an optional expense to an expected component of trip planning across leisure and business traveller segments. Comprehensive, all-inclusive policies accounted for 86% of all travel insurance sales in Australia in 2025, demonstrating the market's decisive preference for breadth of coverage over basic, minimum-premium protection. This behavioural shift is most evident in purchasing patterns across family and senior traveller cohorts, where the financial consequences of uninsured cancellations, medical emergencies, and trip disruptions have driven consistent demand for premium, fully comprehensive policy tiers across domestic and international travel itineraries.

Digital Transformation and AI-Driven Insurance Platforms

Technology is comprehensively transforming the Australian travel insurance value chain, from digital policy distribution and instant underwriting through to AI-accelerated claims processing and real-time customer service. In June 2025, leading digital-first insurer Fast Cover partnered with claims technology company Five Sigma to deploy an AI-driven claims management platform that materially reduced claim turnaround times and accelerated the entire process from first notice of loss to payment settlement. This adoption of AI-powered underwriting, real-time policy management, and embedded digital distribution across online aggregators, insurer direct platforms, and travel booking ecosystems is progressively redefining competitive standards and consumer experience expectations across all product tiers in the Australian market.

Cruise and Niche Travel Segment Expansion

Specialty insurance segments are expanding rapidly as Australian travellers diversify their travel habits toward cruise, adventure, snow, and long-haul destination itineraries that carry distinct risk profiles unserved by standard policy structures. In May 2025, Allianz Partners Australia launched a cruise-specific travel insurance package in partnership with Norwegian Cruise Line, offering embedded coverage for shipboard medical care, emergency evacuation, and cabin confinement at the point of booking — directly integrating protection into the traveller's purchase moment. This embedded distribution model, combining specialised product design with seamless point-of-sale integration through travel partner platforms, reflects the broader strategic direction that is redefining growth in the Australian travel insurance market across the forecast period.

Request for Sample Report: https://www.imarcgroup.com/australia-travel-insurance-market/requestsample

Market Growth Drivers

Surging Outbound and Inbound Travel Activity

Australian travel volumes have firmly returned to a rising structural trend following the post-pandemic recovery, creating a direct and expanding demand base for travel insurance policy uptake across all product segments. The Australian Bureau of Statistics recorded 8,402,400 tourist arrivals in the 2024–2025 fiscal year, representing a 5.5% increase over the prior year, while resident returns reached 1,544,890 journeys in January 2025 alone — a 10.9% year-on-year increase. Each incremental outbound departure represents a potential insurance purchase event, making sustained travel volume growth the most structurally reliable demand driver for the Australian travel insurance market across the entire 2026–2034 forecast horizon.

Rising Overseas Medical Costs Heightening Protection Needs

Medical expense coverage — commanding a 42% share of the coverage segment in 2025 — remains the undisputed anchor product and primary purchase motivation driving Australian travellers toward comprehensive travel insurance policies. Growing consumer awareness of the severe and unpredictable financial consequences of overseas medical treatment, emergency hospitalisation, and repatriation assistance is compelling travellers to prioritise medical protection when planning international itineraries. Destinations with elevated healthcare costs, particularly long-haul markets in North America, Europe, and Japan that Australians commonly visit, are intensifying the perceived necessity of adequate medical coverage and sustaining premium policy demand across leisure, family, and senior traveller segments throughout the forecast period.

Favourable Demographics and Growing Senior Traveller Base

Australia's ageing population is providing structural and sustained support for premium, comprehensive travel insurance product demand, as mature travellers and early retirees consistently select all-inclusive policies with elevated coverage limits and added-value assistance services. Industry data from 2025 confirms that mature travellers and early retirees represent the top buyer demographic in the Australian travel insurance market, regularly investing in comprehensive coverage for peace of mind across both leisure and family travel itineraries. This demographic's demand for all-inclusive plans with superior medical coverage limits, trip cancellation protection, and specialist senior traveller products maintains premium revenue growth and positions the ageing traveller cohort as a structurally significant and commercially valuable long-term market segment.

Porter's Five Forces Analysis of the Australia Travel Insurance Market

1. Threat of New Entrants — Low to Moderate

The Australia travel insurance market presents significant structural and regulatory barriers that constrain new market participation:

- APRA and ASIC regulatory oversight requirements for licensed insurance product issuers impose substantial compliance, capital adequacy, and product disclosure obligations that represent meaningful entry barriers for new domestic and international participants seeking to offer standalone travel insurance products in the Australian market

- Allianz Australia and Zurich's Cover-More collectively commanding approximately 49% of the domestic market — with Allianz holding approximately 25% and Cover-More approximately 24% individually — creates a strongly entrenched competitive concentration that new entrants must invest significantly to compete against across brand trust, distribution relationships, and claims capability

- Digital-native insurers and InsurTech platforms face lower capital barriers in building online distribution and policy management capability, but must still partner with licensed underwriters or obtain their own APRA authorisation before issuing policies, maintaining a meaningful regulatory gatekeeping function

- Allianz's October 2025 acquisition bid for NIB Holdings' travel insurance unit including World Nomads and Travel Insurance Direct signals ongoing market consolidation that progressively narrows the competitive space available to new entrants and reinforces the incumbent advantage of established full-service providers

2. Bargaining Power of Suppliers — Low

Reinsurance providers and technology vendors hold limited but context-specific leverage over travel insurance market participants:

- Global reinsurance providers supplying catastrophe risk capacity and excess-of-loss protection to Australian travel insurers hold moderate leverage during periods of elevated global claims activity — including pandemic disruptions, geopolitical events, and natural disasters — that tighten reinsurance capacity and push up treaty pricing across the market

- Claims technology suppliers including Five Sigma, whose AI-driven platform Fast Cover deployed in June 2025, command growing influence as operational transformation becomes a competitive imperative, though the availability of multiple competing InsurTech vendors constrains any single provider's pricing leverage over insurers

- Distribution platform suppliers including online aggregators and embedded booking platform partners — airlines, cruise operators, and travel agencies — hold meaningful negotiating leverage over insurers seeking featured placement and embedded point-of-sale access, particularly as digital channels grow in strategic importance

- The commoditised nature of standard travel insurance underwriting components — medical expense reimbursement, trip cancellation, and baggage loss — limits individual supplier leverage by enabling insurers to access equivalent risk capacity and reinsurance coverage from multiple competing providers

3. Bargaining Power of Buyers — Moderate

Individual travellers, corporate accounts, and affinity group buyers exercise varied but collectively significant purchasing influence:

- Online insurance aggregators providing instant side-by-side policy comparison across multiple competing providers significantly elevate individual consumer bargaining power, enabling price-sensitive buyers to identify the lowest-cost compliant product across the market and intensifying competitive pricing pressure across standard single-trip and annual multi-trip policy tiers

- Corporate travel managers and large employer groups procuring business travel insurance on behalf of employee populations command substantial volume leverage, negotiating preferential premium rates, customised policy wordings, and dedicated claims service arrangements that smaller individual buyers cannot access

- Family travellers — representing the largest end-user segment at 35% — exhibit relatively lower price sensitivity given the high perceived value of comprehensive protection for multi-person, high-cost international itineraries, reducing their effective bargaining leverage and sustaining premium product demand within this commercially significant buyer cohort

- Senior and mature travellers demonstrating strong willingness to pay for comprehensive, high-limit policies represent a structurally low-leverage buyer segment from a price sensitivity perspective, though their demand for specialised pre-existing condition coverage creates product design pressure on insurers to expand policy accessibility

4. Threat of Substitutes — Low

Australian travel insurance faces minimal credible substitution pressure given the breadth of risk coverage the product provides:

- Credit card embedded travel insurance offered by premium card issuers including American Express — which bundles travel protection within Platinum card membership tiers — represents the most commercially significant substitute, though coverage limits, activation conditions, and exclusion breadth typically fall materially short of standalone comprehensive policy protection

- Government reciprocal healthcare agreements with select countries including the United Kingdom and New Zealand provide limited emergency medical coverage for Australian travellers, but exclude trip cancellation, baggage loss, property damage, and evacuation coverage, leaving substantial uninsured risk exposure that standalone policies address

- Self-insurance through personal savings and emergency funds represents a theoretical substitute for premium-sensitive younger travellers, but the catastrophic and unpredictable cost profile of overseas medical emergencies — which can reach hundreds of thousands of dollars — makes pure self-insurance practically untenable for most Australian traveller profiles

- The breadth of simultaneous risk coverage — medical expenses, trip cancellation, baggage, liability, and emergency assistance bundled in a single policy — creates a comprehensive protection value proposition that no individual substitute product can replicate, fundamentally limiting substitution risk across the market's core buyer segments

5. Competitive Rivalry — High

The Australia travel insurance market is characterised by intense multi-dimensional competition across established multinationals, domestic specialists, and digital-native challengers:

- Allianz Australia and Zurich's Cover-More together control approximately 49% of the domestic market, but compete aggressively against each other and against a competitive field including NIB Travel Services, AIG Australia, 1Cover, Australia Post, and digital-first providers across pricing, product innovation, distribution partnership, and claims service quality dimensions

- Fast Cover's June 2025 AI-driven claims platform deployment signals a technology investment arms race in which operational efficiency, claims speed, and digital customer experience are becoming primary competitive differentiators alongside traditional product breadth and premium pricing

- Allianz's October 2025 acquisition bid for NIB Holdings' travel insurance unit — including the World Nomads and Travel Insurance Direct brands — reflects the strategic conviction among leading players that market consolidation through M&A is a necessary response to intensifying price competition and digital distribution disruption

- The expansion of embedded insurance distribution through airline booking platforms, cruise operators, and online travel agencies is creating new competitive fronts beyond the traditional aggregator and direct insurer channel battlegrounds, compelling all major market participants to invest in partnership distribution capabilities and contextual product design to maintain competitive channel coverage

Market Segments

By Insurance Type:

- Single-Trip Travel Insurance

- Annual Multi-Trip Travel Insurance

- Long-Stay Travel Insurance

By Coverage:

- Medical Expenses

- Trip Cancellation

- Trip Delay

- Property Damage

- Others

By Distribution Channel:

- Insurance Companies

- Insurance Intermediaries

- Banks

- Insurance Aggregators

- Insurance Brokers

- Others

By End User:

- Family Travelers

- Senior Citizens

- Education Travelers

- Business Travelers

- Others

By Region:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Competitive Landscape

The market research report has provided a comprehensive analysis of the competitive landscape in the Australia travel insurance market. Competitive analysis covering market structure, key player positioning, top winning strategies, competitive dashboard, and a company evaluation quadrant with detailed profiles of all major companies has been included in the report. Key participants including Allianz Australia Limited, Zurich Financial Services Australia, NIB Travel Services, Fast Cover, AIG Australia, 1Cover, Australia Post Group, and American Express Company compete across product innovation, digital platform investment, embedded distribution partnerships, and M&A-driven consolidation strategies across all coverage, end-user, and regional segments throughout the Australian market.

Latest News and Developments

2025: In June 2025, Fast Cover deployed an AI-driven claims management platform developed in partnership with Five Sigma, significantly reducing claim turnaround times and accelerating the complete process from first notice of loss to settlement payment. This implementation positioned Fast Cover as a technology leader in Australian travel insurance claims service and signalled the broader industry shift toward AI-powered operational transformation. In October 2025, Allianz Australia advanced an acquisition bid for NIB Holdings' travel insurance division — encompassing the World Nomads and Travel Insurance Direct brands — in a consolidation move that, if completed, would further concentrate the Australian market's competitive landscape among a smaller number of dominant full-service providers.

2025: In May 2025, Allianz Partners Australia launched a cruise-specific travel insurance package embedded within Norwegian Cruise Line's booking platform, offering integrated coverage for shipboard medical treatment, emergency evacuation, and cabin confinement at the point of purchase. The product launch demonstrated the commercial viability of embedded specialty insurance distribution through travel partner platforms and reinforced the growing strategic importance of point-of-sale integration as a competitive growth channel for Australian travel insurers seeking to capture travellers at their highest purchase-intent moment across the expanding cruise segment.

2024: The Australian Bureau of Statistics confirmed that Australians completed 11.5 million overseas trips in 2024, surpassing pre-pandemic outbound travel volumes for the first time and establishing a new baseline demand level for travel insurance policy uptake across all product tiers. Resident international returns recorded a 10.9% year-on-year increase in January 2025 to 1,544,890 journeys, providing quantified evidence of the structural recovery in outbound travel activity that is directly expanding the addressable insurance market across leisure, family, business, and senior traveller segments nationwide.

2024: Comprehensive, all-inclusive travel insurance policies accounted for 86% of all travel insurance sales in Australia, reflecting the durable post-pandemic behavioural shift among Australian travellers toward prioritising breadth of coverage over minimum-cost basic protection. This premium product preference concentration reinforced the commercial positioning of full-service insurers offering comprehensive policy structures and supported sustained average premium revenue growth across the market. Insurers responded by expanding modular add-on offerings including adventure packs, cruise packs, and snow packs, enabling policy customisation while maintaining comprehensive base coverage as the structural market standard.

2023: Telemedicine service integration within travel insurance policies gained commercial momentum across the Australian market as leading insurers incorporated real-time overseas medical consultation access into policy assistance services, enabling travellers to obtain professional medical guidance for minor health issues and prevent unnecessary escalation into full repatriation events. This capability enhancement improved both claims cost management outcomes for insurers and traveller confidence in overseas health protection, contributing to growing consumer willingness to invest in comprehensive policies with higher premium price points across leisure and family traveller segments.

2022: Annual multi-trip travel insurance policy adoption accelerated among frequent business and leisure travellers as Australian outbound travel activity recovered strongly through 2022, with cost-conscious frequent flyers and corporate travellers recognising the per-trip premium efficiency advantages of annual multi-trip plans over sequential single-trip policy purchases. Insurers expanded and competitively repriced annual policy offerings in response to growing demand, while corporate travel managers increasingly standardised annual multi-trip coverage as the default insurance arrangement for employees travelling internationally more than twice per year, generating predictable recurring premium revenue within the business traveller segment.

2021: The Australian travel insurance market demonstrated adaptive resilience through the staged international travel reopening process, with leading insurers including Allianz Australia and Cover-More introducing enhanced pandemic-related coverage provisions and quarantine cost benefits into their policy structures to address the novel risk concerns that had deterred travel insurance purchasing during the peak pandemic disruption period. This product adaptation — incorporating COVID-19 medical expense coverage, cancellation protection for border closure events, and mandatory quarantine accommodation benefits — re-established consumer confidence in travel insurance relevance and value, laying the commercial foundation for the market's strong post-pandemic demand recovery through 2022–2025.

Note

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customisation.

Speak to an Analyst for a Customised Sample Report: https://www.imarcgroup.com/request?type=report&id=21979&flag=C

About Us

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us

Email: sales@imarcgroup.com

Tel No.: (D) +91 120 433 0800

United States: +1-201-971-6302

What's Your Reaction?